Advertisement

- Japan

- /

- Infrastructure

- /

- TSE:9351

There May Be Underlying Issues With The Quality Of Toyo Wharf & Warehouse's (TSE:9351) Earnings

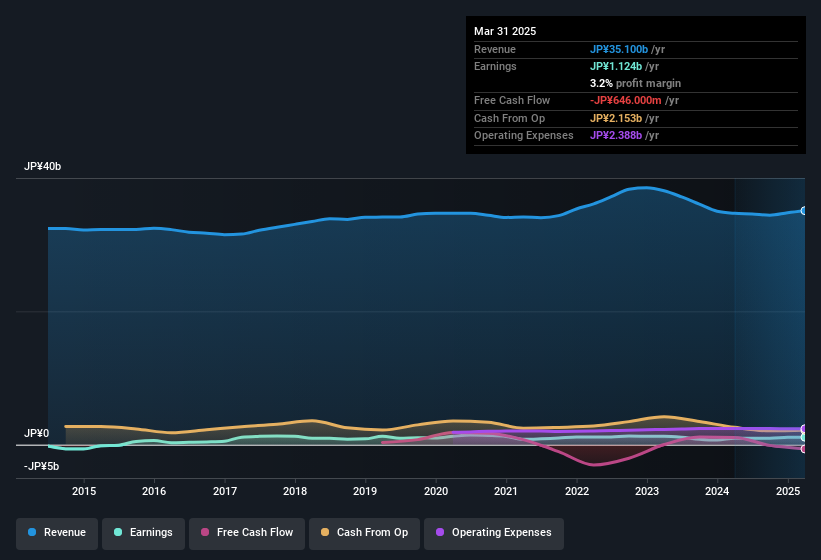

Despite posting some strong earnings, the market for Toyo Wharf & Warehouse Co., Ltd.'s (TSE:9351) stock hasn't moved much. Our analysis suggests that this might be because shareholders have noticed some concerning underlying factors.

The Impact Of Unusual Items On Profit

To properly understand Toyo Wharf & Warehouse's profit results, we need to consider the JP¥285m gain attributed to unusual items. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. Which is hardly surprising, given the name. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Toyo Wharf & Warehouse.

Our Take On Toyo Wharf & Warehouse's Profit Performance

We'd posit that Toyo Wharf & Warehouse's statutory earnings aren't a clean read on ongoing productivity, due to the large unusual item. Because of this, we think that it may be that Toyo Wharf & Warehouse's statutory profits are better than its underlying earnings power. But at least holders can take some solace from the 15% EPS growth in the last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. To that end, you should learn about the 5 warning signs we've spotted with Toyo Wharf & Warehouse (including 2 which are significant).

Today we've zoomed in on a single data point to better understand the nature of Toyo Wharf & Warehouse's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Toyo Wharf & Warehouse might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9351

Moderate risk average dividend payer.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor