If you have been watching Murata Manufacturing (TSE:6981) recently, you might be wondering what’s driving attention to the stock this week. Unlike periods where companies are in the headlines for flashy breakthroughs or big M&A moves, Murata’s latest price shift hasn’t been sparked by an obvious external event. Sometimes, though, a quiet stretch can be just as intriguing for long-term investors and can raise new questions about where the company’s value truly lies in the current market.

Zooming out, Murata Manufacturing’s stock has given investors a mixed ride this year, with longer-term returns painting a very different picture than the recent drift. Its shares have slipped around 7% over the past year, despite a roughly 14% rise in the past three months and some bounce during the past month. In the bigger scheme, the five-year return sits above 21%, suggesting periods of both sharp optimism and investor caution. Notably, Murata has continued to grow both revenue and net profit year over year, which adds another layer to the valuation debate.

With all this back and forth, the question for investors is as timely as ever: is the current price an opportunity to buy into future growth, or has the market already balanced the upside in?

Advertisement

Price-to-Earnings of 20.8x: Is it justified?

On a price-to-earnings (P/E) basis, Murata Manufacturing trades above the Japanese electronic industry average. This signals the market views it as relatively expensive compared to domestic sector peers.

The P/E ratio reflects what investors are willing to pay for one unit of current or projected earnings. For manufacturing firms, especially in tech, it is a key gauge of whether the market expects future growth, improved profitability, or just stability compared to competitors.

Murata’s elevated P/E could mean there is confidence in its earnings resilience and innovation pipeline. It may also suggest investors are already paying up for expected progress, which adds pressure to deliver on those expectations.

However, slowing revenue growth or falling short of earnings expectations could quickly shift market sentiment and pose risks to Murata’s current valuation.

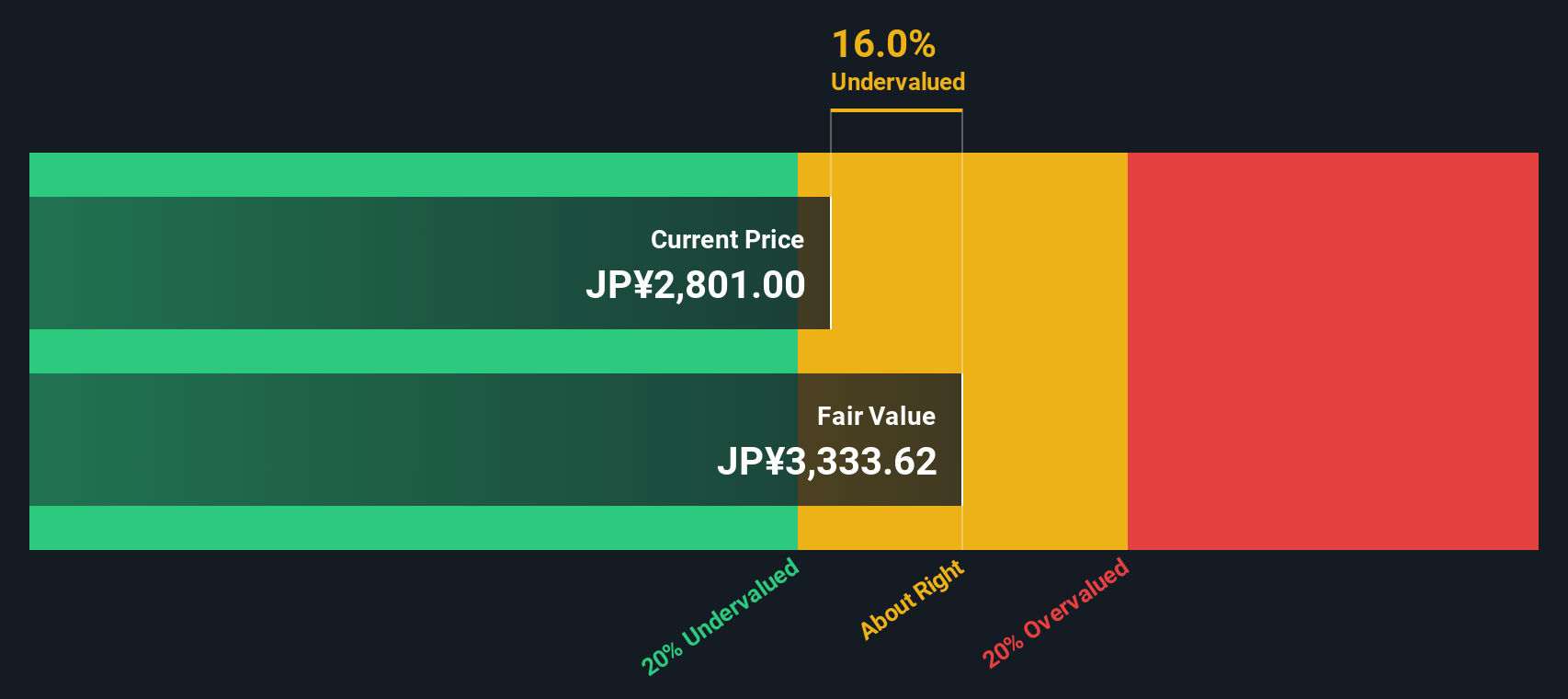

Another View: SWS DCF Model Tells a Different Story

Looking from a different perspective, our DCF model highlights a potentially undervalued situation for Murata Manufacturing, which challenges the conclusion drawn from earnings multiples. Do market expectations overlook something that the DCF is capturing?

If you see things differently or want to dig deeper into the numbers, you can dive in and craft your own perspective in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Murata Manufacturing.

Looking for more investment ideas?

Why settle for just one potential win when you can discover more? Explore opportunities across innovative sectors with Simply Wall Street’s curated stock ideas below.

Find high-growth potential in today's market by focusing on shares with stable cash flows and attractive prices, using our list of undervalued stocks based on cash flows.

Benefit from tech trends that are changing healthcare by identifying companies transforming patient care and diagnostics, all featured in our healthcare AI stocks.

Start your portfolio’s income stream with companies offering standout yields above 3 percent, showcased in our dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.