Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6965

Hamamatsu Photonics K.K. Earnings Missed Analyst Estimates: Here's What Analysts Are Forecasting Now

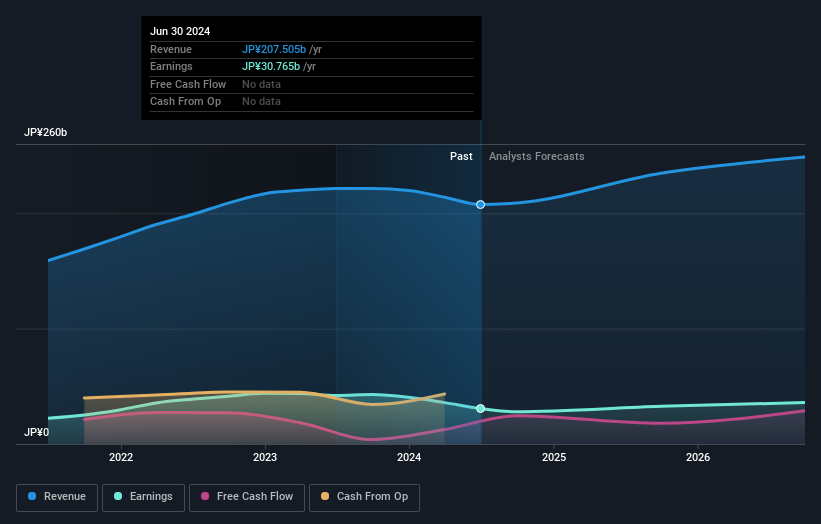

The analysts might have been a bit too bullish on Hamamatsu Photonics K.K. (TSE:6965), given that the company fell short of expectations when it released its third-quarter results last week. Results showed a clear earnings miss, with JP¥47b revenue coming in 8.3% lower than what the analystsexpected. Statutory earnings per share (EPS) of JP¥23.50 missed the mark badly, arriving some 60% below what was expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Hamamatsu Photonics K.K

After the latest results, the eight analysts covering Hamamatsu Photonics K.K are now predicting revenues of JP¥234.7b in 2025. If met, this would reflect a solid 13% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to rise 5.2% to JP¥209. Before this earnings report, the analysts had been forecasting revenues of JP¥235.1b and earnings per share (EPS) of JP¥216 in 2025. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

It might be a surprise to learn that the consensus price target fell 5.8% to JP¥5,917, with the analysts clearly linking lower forecast earnings to the performance of the stock price. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Hamamatsu Photonics K.K, with the most bullish analyst valuing it at JP¥7,200 and the most bearish at JP¥4,100 per share. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 10% growth on an annualised basis. That is in line with its 11% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 7.1% annually. So although Hamamatsu Photonics K.K is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that in mind, we wouldn't be too quick to come to a conclusion on Hamamatsu Photonics K.K. Long-term earnings power is much more important than next year's profits. We have forecasts for Hamamatsu Photonics K.K going out to 2026, and you can see them free on our platform here.

Even so, be aware that Hamamatsu Photonics K.K is showing 1 warning sign in our investment analysis , you should know about...

Valuation is complex, but we're here to simplify it.

Discover if Hamamatsu Photonics K.K might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6965

Hamamatsu Photonics K.K

Manufactures and sells photomultiplier tubes, imaging devices, light sources, opto-semiconductors, and imaging and analyzing systems in Japan and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

15 followersusers have followed this narrative

5 commentsusers have commented on this narrative

2 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.563.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

948 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative