- Japan

- /

- Electronic Equipment and Components

- /

- TSE:3107

Daiwabo Holdings (TSE:3107) Is Paying Out A Larger Dividend Than Last Year

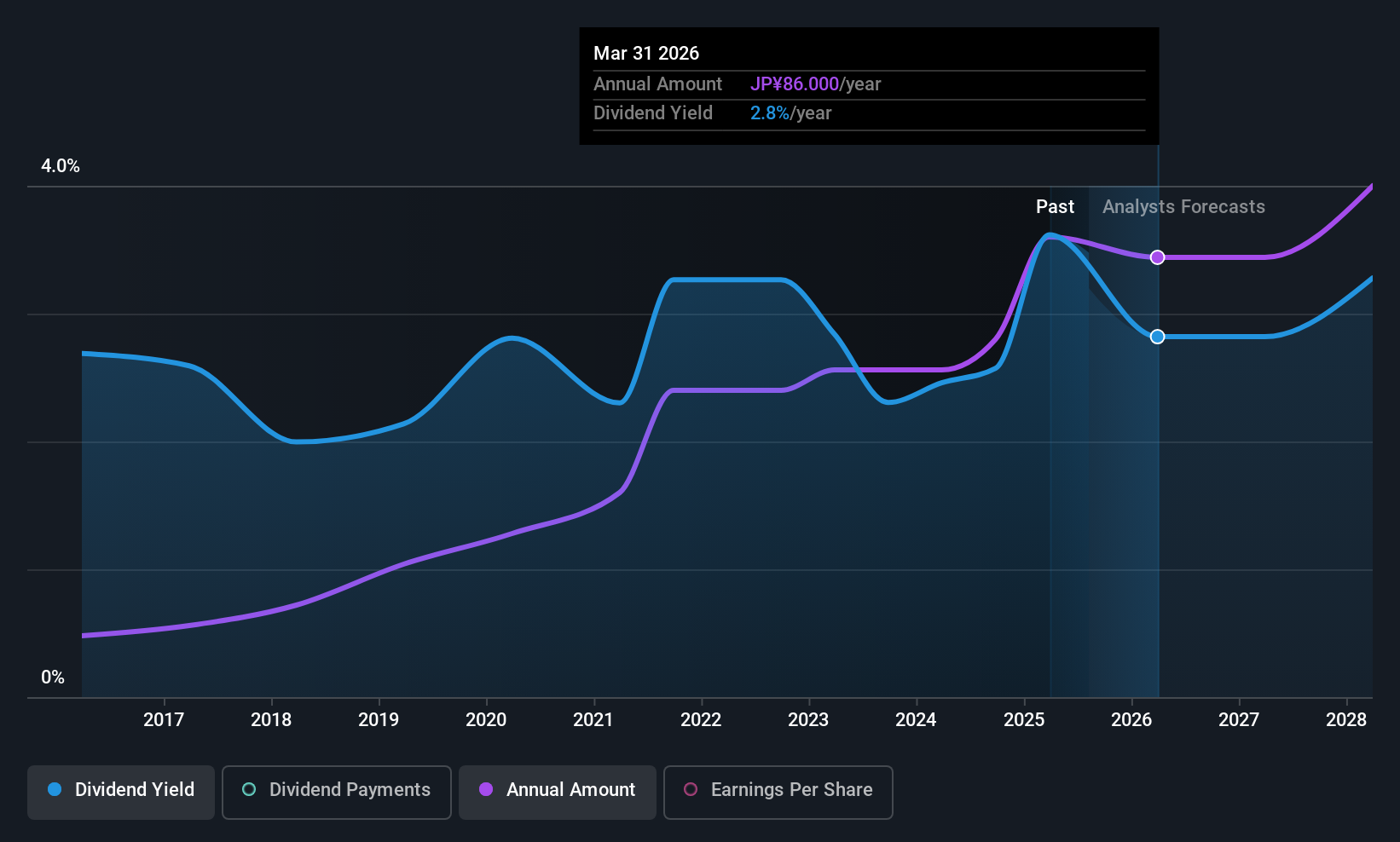

Daiwabo Holdings Co., Ltd. (TSE:3107) has announced that it will be increasing its dividend from last year's comparable payment on the 2nd of December to ¥50.00. This will take the dividend yield to an attractive 3.3%, providing a nice boost to shareholder returns.

Daiwabo Holdings' Payment Could Potentially Have Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. Based on the last payment, Daiwabo Holdings was paying only paying out a fraction of earnings, but the payment was a massive 355% of cash flows. While the business may be attempting to set a balanced dividend policy, a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

Over the next year, EPS is forecast to fall by 4.1%. Assuming the dividend continues along recent trends, we believe the payout ratio could be 36%, which we are pretty comfortable with and we think is feasible on an earnings basis.

See our latest analysis for Daiwabo Holdings

Daiwabo Holdings Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2015, the annual payment back then was ¥12.00, compared to the most recent full-year payment of ¥100.00. This means that it has been growing its distributions at 24% per annum over that time. It is good to see that there has been strong dividend growth, and that there haven't been any cuts for a long time.

We Could See Daiwabo Holdings' Dividend Growing

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Daiwabo Holdings has impressed us by growing EPS at 7.4% per year over the past five years. Daiwabo Holdings definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 2 warning signs for Daiwabo Holdings (of which 1 is a bit unpleasant!) you should know about. Is Daiwabo Holdings not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3107

Flawless balance sheet average dividend payer.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)