- Sweden

- /

- Capital Markets

- /

- OM:EQT

3 Growth Companies Insiders Are Betting On

Reviewed by Simply Wall St

In the current global market landscape, marked by cautious Federal Reserve commentary and broad-based declines in U.S. stocks, investors are increasingly seeking stability amidst uncertainty. With central banks around the world adjusting their monetary policies and economic data presenting a mixed picture, insider ownership can serve as a strong indicator of confidence in a company's growth potential.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 25.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Medley (TSE:4480) | 34% | 31.7% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

| HANA Micron (KOSDAQ:A067310) | 18.5% | 110.9% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Underneath we present a selection of stocks filtered out by our screen.

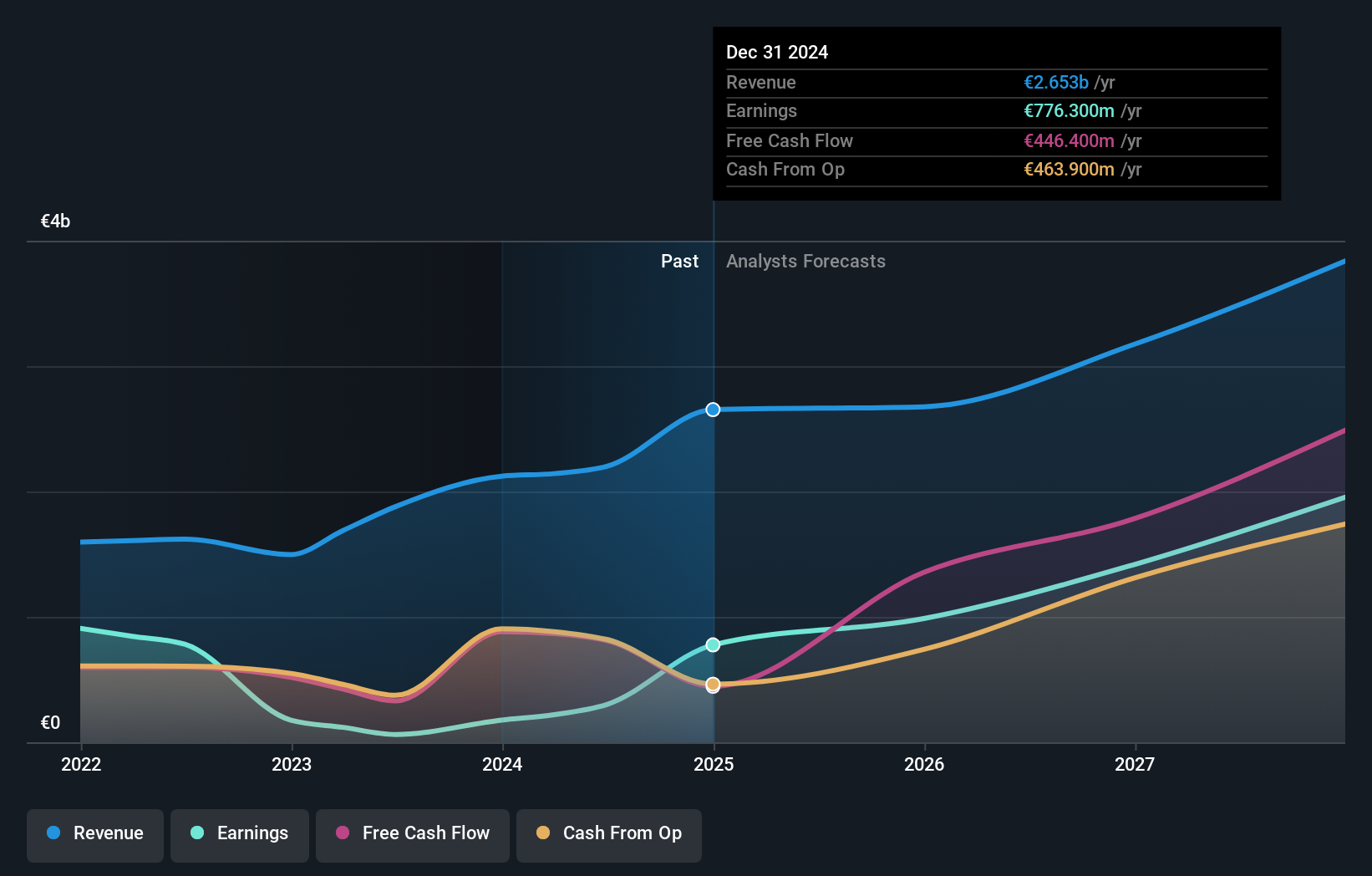

EQT (OM:EQT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: EQT AB (publ) is a global private equity firm focusing on private capital and real asset segments, with a market cap of approximately SEK357.47 billion.

Operations: The company's revenue is derived from its central operations (€37.20 million), real assets (€878.70 million), and private capital segments (€1.28 billion).

Insider Ownership: 12.2%

Earnings Growth Forecast: 33.3% p.a.

EQT AB is experiencing robust growth, with earnings forecasted to increase by 33.3% annually, outpacing the Swedish market's average. Despite trading slightly below its estimated fair value, recent insider activity shows significant selling over the past three months. The company is actively involved in strategic M&A discussions, including potential acquisitions and IPOs that could enhance its portfolio and market position. However, large one-off items have impacted financial results recently.

- Click to explore a detailed breakdown of our findings in EQT's earnings growth report.

- Insights from our recent valuation report point to the potential overvaluation of EQT shares in the market.

Shenzhen New Industries Biomedical Engineering (SZSE:300832)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen New Industries Biomedical Engineering Co., Ltd. is a bio-medical company that focuses on the research, development, production, and sale of clinical laboratory instruments and in vitro diagnostic reagents for hospitals both in China and internationally, with a market cap of CN¥55.87 billion.

Operations: The company generates revenue primarily from its in vitro diagnostic segment, totaling CN¥4.44 billion.

Insider Ownership: 21.8%

Earnings Growth Forecast: 21.7% p.a.

Shenzhen New Industries Biomedical Engineering's recent earnings report showed sales of CNY 3.41 billion, up from CNY 2.91 billion the previous year, with net income rising to CNY 1.38 billion. Despite an unstable dividend record, the company is trading below estimated fair value and is expected to grow revenue at 21.2% annually, surpassing market averages. Analysts agree on a potential stock price increase of over 20%, reflecting strong growth prospects despite slower profit growth compared to the broader market.

- Take a closer look at Shenzhen New Industries Biomedical Engineering's potential here in our earnings growth report.

- The analysis detailed in our Shenzhen New Industries Biomedical Engineering valuation report hints at an deflated share price compared to its estimated value.

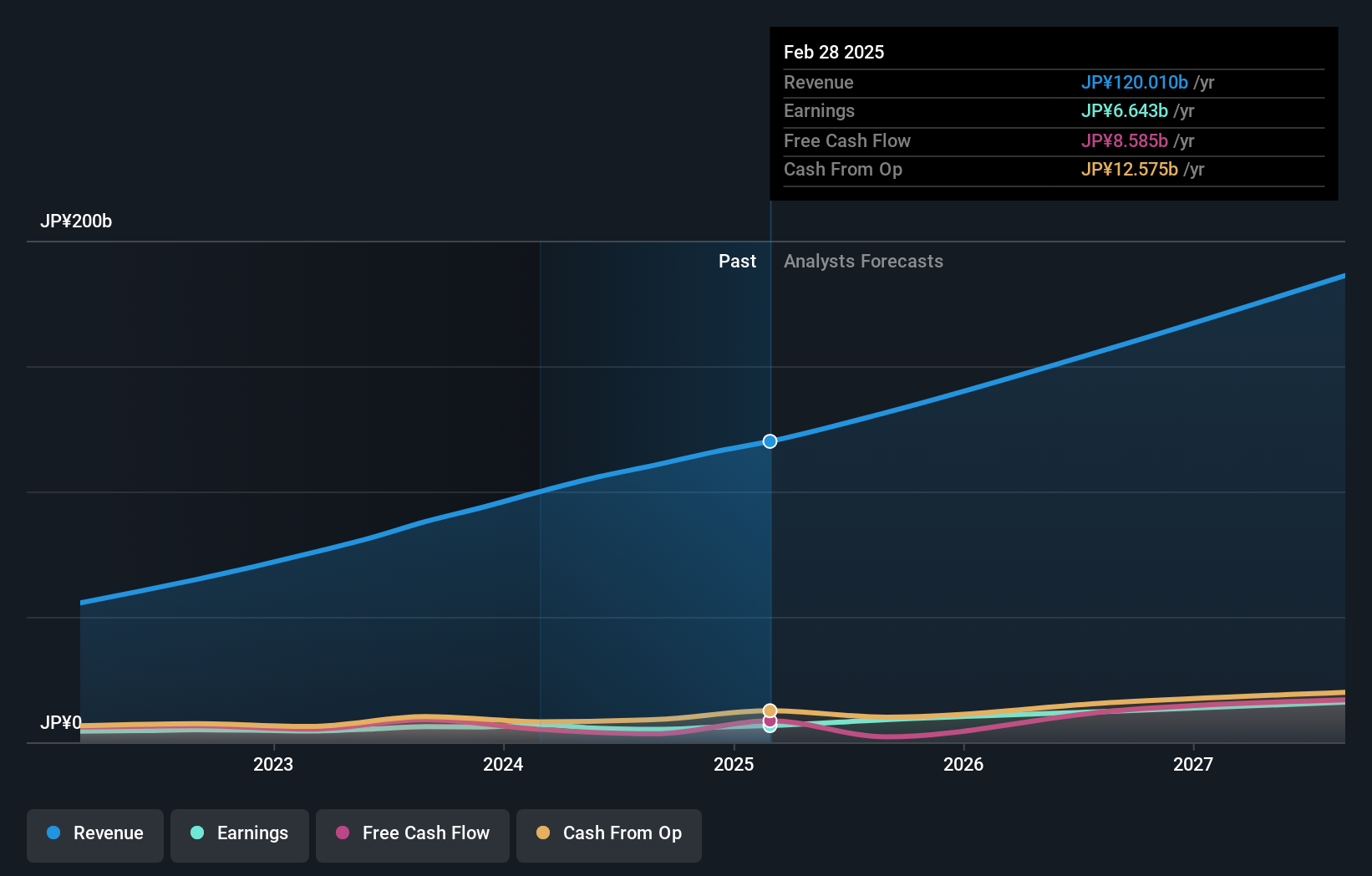

SHIFT (TSE:3697)

Simply Wall St Growth Rating: ★★★★★☆

Overview: SHIFT Inc. offers software quality assurance and testing solutions in Japan, with a market cap of ¥311.05 billion.

Operations: The company generates revenue primarily from Software Testing Related Services, amounting to ¥71.34 billion, and Software Development Related Services, amounting to ¥35.01 billion.

Insider Ownership: 32.9%

Earnings Growth Forecast: 30.1% p.a.

SHIFT Inc. is expected to experience significant earnings growth of 30.1% annually over the next three years, outpacing the JP market's average. Despite a recent decline in profit margins and a highly volatile share price, SHIFT is trading at 12.8% below its estimated fair value. The company recently completed a share buyback program worth ¥999.61 million, aimed at enhancing corporate value and shareholder returns, indicating confidence in its future performance.

- Unlock comprehensive insights into our analysis of SHIFT stock in this growth report.

- The valuation report we've compiled suggests that SHIFT's current price could be inflated.

Turning Ideas Into Actions

- Gain an insight into the universe of 1511 Fast Growing Companies With High Insider Ownership by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if EQT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:EQT

EQT

A global private equity & venture capital firm specializing in private capital and real asset segments.

High growth potential with solid track record.

Similar Companies

Market Insights

Community Narratives