Takashimaya Company (TSE:8233) has seen its stock catch the attention of investors recently, not due to a major single event, but because the steady movement in its share price is prompting questions about what comes next. For those wondering if this pattern is hinting at a new direction or simply reflecting ongoing shifts in market confidence, it might be worth taking a closer look at what is driving this retail giant.

Over the past year, Takashimaya Company has delivered returns that may surprise some; its shares are up nearly 30% in twelve months, and they have gained even more in recent months. There is momentum building here, particularly as the company continues to report stable revenue and net income growth. However, there is no big news announcement behind the trend, making the performance all the more intriguing.

After all this positive movement in the share price, do the fundamentals still suggest Takashimaya Company is undervalued, or is the market fully pricing in future growth from here?

Advertisement

Price-to-Earnings of 12.5x: Is it justified?

Takashimaya Company is currently valued at a price-to-earnings (P/E) ratio of 12.5x, which is lower than both the peer average (17.4x) and the Japan Multiline Retail industry average (17.6x). This below-average multiple suggests that investors may be assigning a discount relative to its sector peers.

The price-to-earnings ratio reflects how much investors are willing to pay today for each unit of the company's earnings. In retail, the P/E ratio is a key benchmark, helping to compare companies’ profitability and expected growth within the sector.

A below-average P/E can signal undervaluation if the company’s fundamentals remain strong, or it may reflect tempered expectations for future earnings growth. In this case, Takashimaya’s multiple implies the market may be underestimating its potential, even as the company’s earnings continue to grow.

However, risks remain, such as slowing annual revenue growth. The stock is now trading above analyst targets, which could prompt a reassessment by investors.

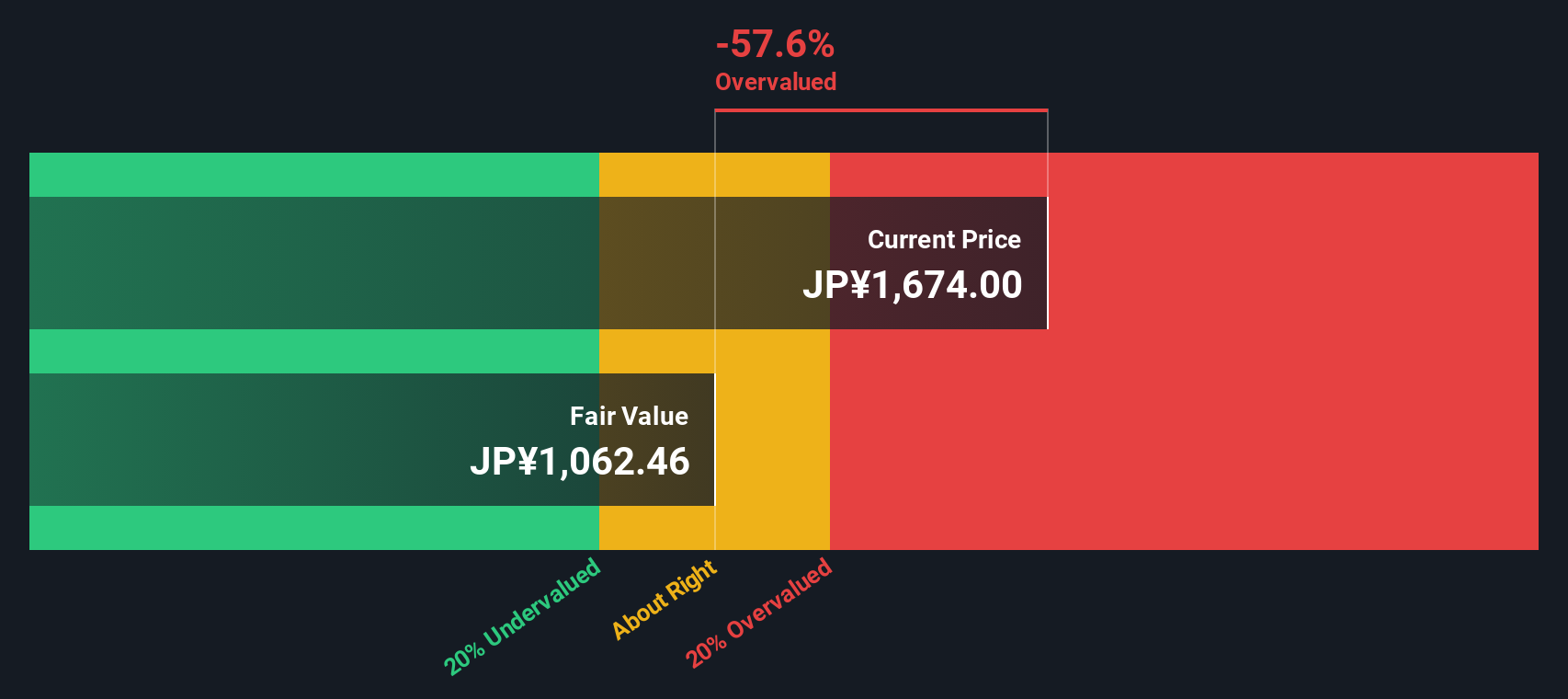

Looking at Takashimaya Company from the perspective of our DCF model produces a markedly different valuation, suggesting the stock could be significantly overvalued. When different models provide contrasting results, it raises the question of which one investors should trust.

If these conclusions do not align with your perspective, or if you would prefer to analyze the data yourself, you can quickly create your own comprehensive view of Takashimaya Company. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Takashimaya Company.

Looking for More Smart Investment Ideas?

Unlock even more opportunities by checking out promising sectors that could transform your portfolio. Miss this and you could pass up market leaders of tomorrow.

Spot high-growth opportunities by checking out AI penny stocks, which are shaping everything from software to smart retail.

Capture steady income streams as you browse dividend stocks with yields > 3%, featuring reliable companies with strong yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Takashimaya Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.