- Japan

- /

- Specialty Stores

- /

- TSE:8185

Undiscovered Gems in Japan to Explore This October 2024

Reviewed by Simply Wall St

As Japan's stock markets experience a downturn, with the Nikkei 225 Index and the TOPIX Index both declining, investors are closely watching the country's economic indicators for signs of stability. Amid easing domestic inflation and fluctuating export numbers, this environment presents a unique opportunity to explore lesser-known stocks that may offer potential value in an evolving market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In Japan

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Toho | 69.52% | 2.84% | 55.65% | ★★★★★★ |

| Ohashi Technica | NA | 1.57% | -20.55% | ★★★★★★ |

| Toukei Computer | NA | 5.46% | 12.14% | ★★★★★★ |

| Techno Smart | NA | 6.07% | -0.57% | ★★★★★★ |

| Yashima Denki | 2.93% | -2.38% | 13.99% | ★★★★★★ |

| Imuraya Group | 26.21% | 2.37% | 32.09% | ★★★★★☆ |

| MIRARTH HOLDINGSInc | 266.33% | 3.00% | -2.40% | ★★★★☆☆ |

| Hakuto | 56.93% | 8.02% | 27.72% | ★★★★☆☆ |

| Toho Bank | 98.27% | 0.43% | 22.80% | ★★★★☆☆ |

| FDK | 89.57% | -0.88% | 25.34% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

TAUNS LaboratoriesInc (TSE:197A)

Simply Wall St Value Rating: ★★★★★☆

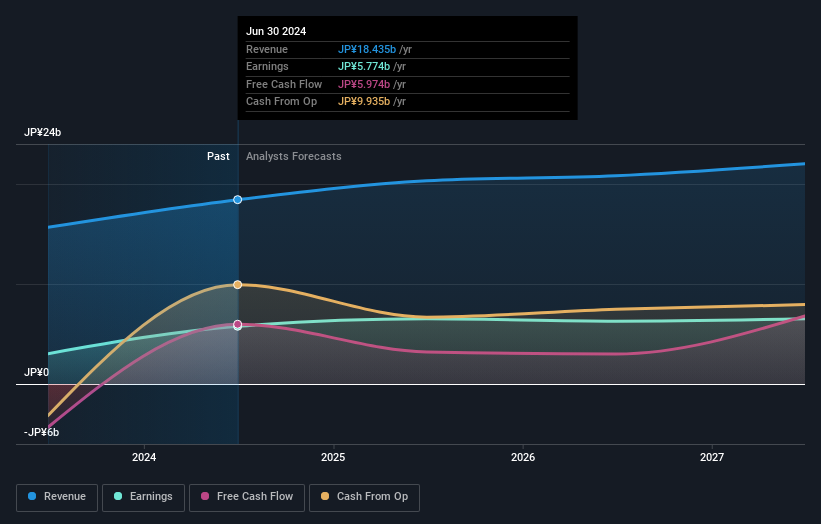

Overview: TAUNS Laboratories, Inc. is involved in the development, manufacture, export/import, and sale of in vitro diagnostics and research reagents globally with a market cap of ¥55.30 billion.

Operations: TAUNS Laboratories generates revenue primarily from its IVD Business, amounting to ¥18.43 billion. The company's net profit margin is a key financial indicator to consider when evaluating its profitability.

TAUNS Laboratories, a notable player in the medical equipment sector, has shown impressive earnings growth of 90% over the past year, outpacing the industry average of 3%. Trading at a valuation that's about 44% below its estimated fair value suggests potential upside. The company's debt is well-managed with an interest coverage ratio of 341x and a net debt to equity ratio of just 0.8%, indicating financial stability. Recent executive appointments and dividend announcements reflect strategic positioning for future growth, with expected net income for fiscal year ending June 2025 projected at ¥6 billion (US$).

Fuji Seal International (TSE:7864)

Simply Wall St Value Rating: ★★★★★★

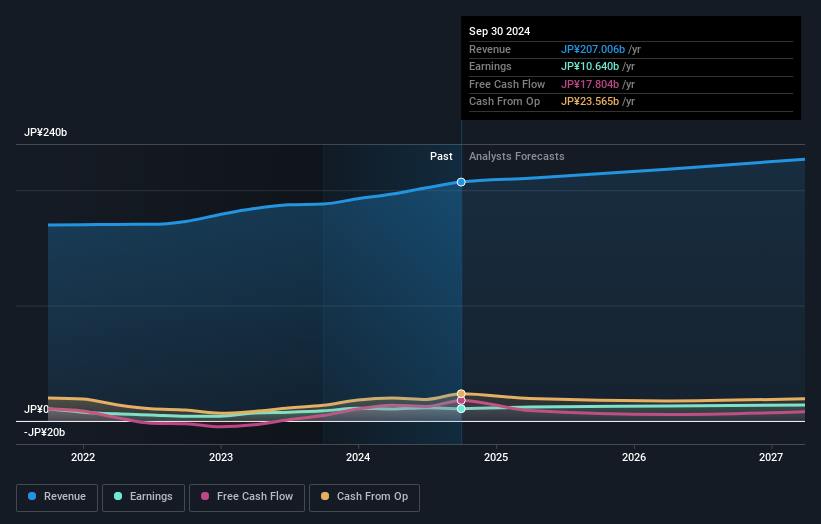

Overview: Fuji Seal International, Inc. offers packaging solutions mainly for the food, beverage, home and personal care, and medical fluid diet sectors with a market capitalization of ¥1.39 billion.

Operations: Fuji Seal International generates revenue from its key markets in Japan, the Americas, Europe, and ASEAN, with Japan contributing ¥100.11 billion and the Americas ¥60.81 billion. The company's financial performance is reflected in its market capitalization of ¥138.80 billion.

Fuji Seal International, a notable player in the packaging industry, showcases strong financial health with its debt to equity ratio dropping from 12.8% to 4.8% over five years. The company boasts high-quality earnings and has seen an impressive earnings growth of 53.9%, outpacing the industry average of 33.7%. Despite announcing a share repurchase program worth ¥3 billion for up to 1,250,000 shares aimed at enhancing capital efficiency and shareholder returns, no shares have been repurchased yet as of late September 2024. With these dynamics at play, Fuji Seal seems well-positioned within its sector for future potential growth.

Chiyoda (TSE:8185)

Simply Wall St Value Rating: ★★★★★★

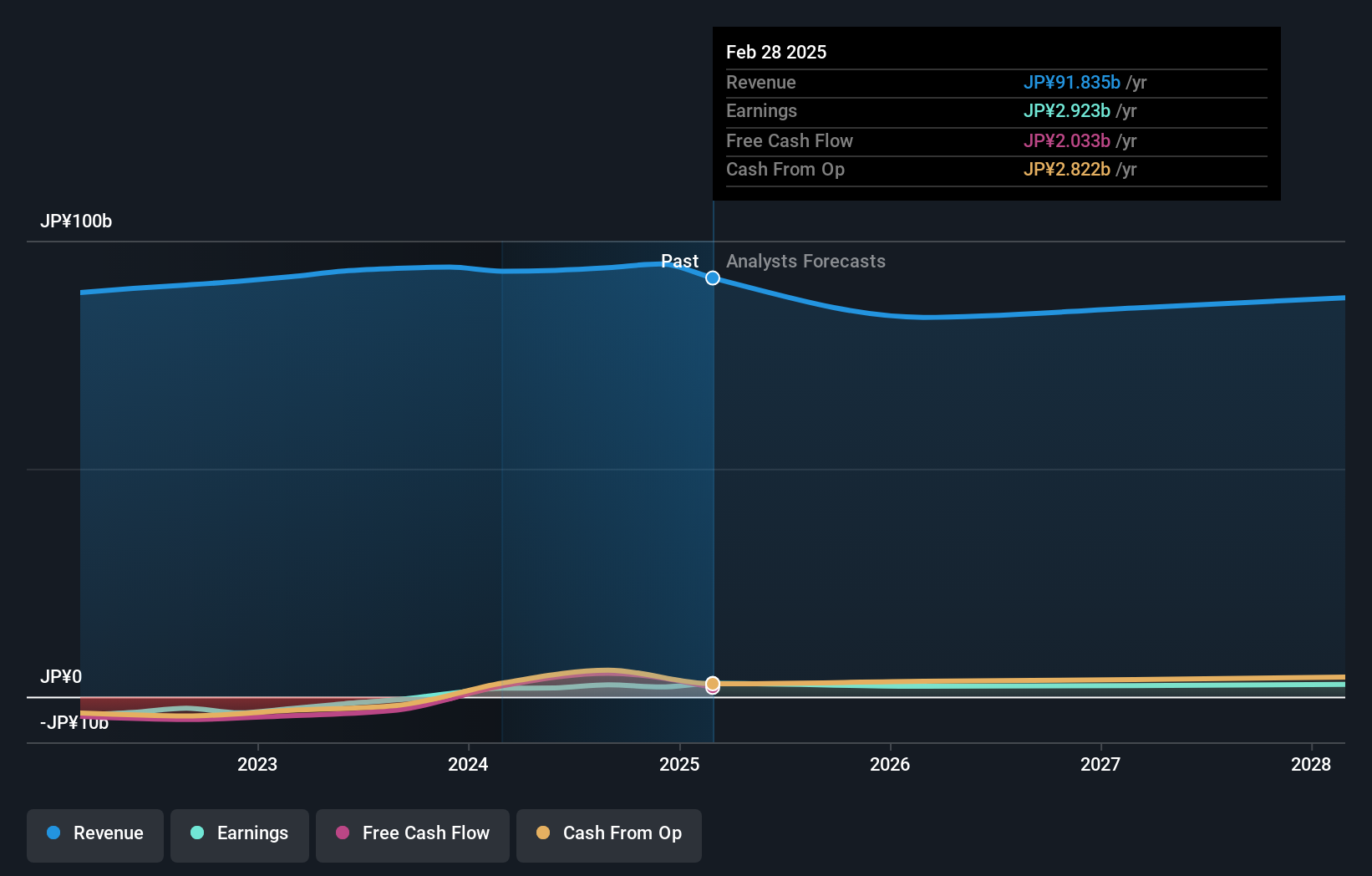

Overview: Chiyoda Co., Ltd., along with its subsidiaries, operates in the retail sector focusing on shoes and sneakers in Japan, with a market capitalization of ¥47.61 billion.

Operations: Chiyoda generates revenue primarily through the retail sale of shoes and sneakers in Japan. The company's cost structure includes expenses related to inventory procurement, store operations, and marketing activities. Notably, its net profit margin has shown variability over recent periods.

Chiyoda, operating in the specialty retail sector, has recently turned profitable, outperforming industry growth of 4.6%. Trading at 93.6% below its estimated fair value, it presents an intriguing opportunity despite forecasts of a 2.7% annual earnings decline over the next three years. The company is debt-free now compared to five years ago when its debt-to-equity ratio was 1.9%, which bolsters its financial stability and eliminates concerns over interest payments. With high-quality past earnings and positive free cash flow, Chiyoda's current financial health seems robust even as future growth prospects appear modestly challenging.

- Unlock comprehensive insights into our analysis of Chiyoda stock in this health report.

Gain insights into Chiyoda's historical performance by reviewing our past performance report.

Taking Advantage

- Embark on your investment journey to our 723 Japanese Undiscovered Gems With Strong Fundamentals selection here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8185

Flawless balance sheet with proven track record.

Market Insights

Community Narratives