Advertisement

- Japan

- /

- Specialty Stores

- /

- TSE:3333

Asahi Co., Ltd.'s (TSE:3333) Fundamentals Look Pretty Strong: Could The Market Be Wrong About The Stock?

With its stock down 13% over the past three months, it is easy to disregard Asahi (TSE:3333). But if you pay close attention, you might find that its key financial indicators look quite decent, which could mean that the stock could potentially rise in the long-term given how markets usually reward more resilient long-term fundamentals. Particularly, we will be paying attention to Asahi's ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Asahi is:

8.9% = JP¥3.5b ÷ JP¥39b (Based on the trailing twelve months to November 2024).

The 'return' is the income the business earned over the last year. So, this means that for every ¥1 of its shareholder's investments, the company generates a profit of ¥0.09.

See our latest analysis for Asahi

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

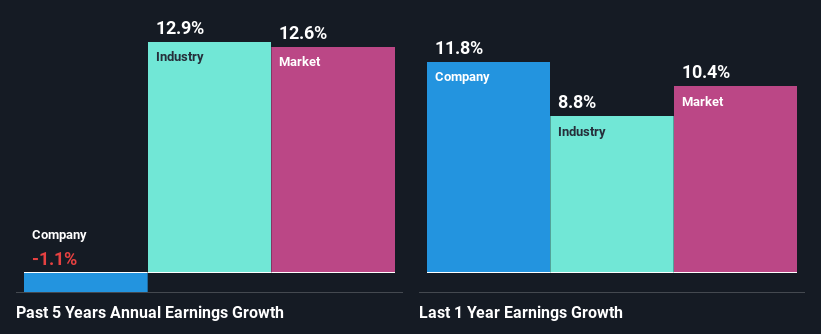

Asahi's Earnings Growth And 8.9% ROE

To begin with, Asahi seems to have a respectable ROE. Even when compared to the industry average of 9.3% the company's ROE looks quite decent. Despite this, Asahi's five year net income growth was quite flat over the past five years. We reckon that there could be some other factors at play here that's limiting the company's growth. Such as, the company pays out a huge portion of its earnings as dividends, or is faced with competitive pressures.

We then compared Asahi's net income growth with the industry and found that the average industry growth rate was 13% in the same 5-year period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Asahi's's valuation, check out this gauge of its price-to-earnings ratio , as compared to its industry.

Is Asahi Using Its Retained Earnings Effectively?

Despite having a moderate three-year median payout ratio of 35% (meaning the company retains65% of profits) in the last three-year period, Asahi's earnings growth was more or les flat. Therefore, there might be some other reasons to explain the lack in that respect. For example, the business could be in decline.

Moreover, Asahi has been paying dividends for four years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer dividends over earnings growth.

Conclusion

Overall, we feel that Asahi certainly does have some positive factors to consider. Although, we are disappointed to see a lack of growth in earnings even in spite of a high ROE and and a high reinvestment rate. We believe that there might be some outside factors that could be having a negative impact on the business. That being so, the latest industry analyst forecasts show that the analysts are expecting to see a huge improvement in the company's earnings growth rate. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3333

Asahi

Sells bicycles, parts, accessories, and other related products in Japan and China.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|13.6% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|69.8% undervalued

OI

Community Contributor