Advertisement

Eisai (TSE:4523) Valuation in Focus After Launch of At-Home Alzheimer’s Treatment Leqembi Iqlik

Simply Wall St

Reviewed by Kshitija Bhandaru

Eisai (TSE:4523) and Biogen have launched Leqembi Iqlik, a subcutaneous autoinjector that allows patients with early-stage Alzheimer's disease in the U.S. to continue maintenance treatment at home after initial intravenous therapy.

See our latest analysis for Eisai.

Eisai’s momentum in Alzheimer’s innovation has arrived amid a volatile year for its investors. The launch of Leqembi Iqlik follows a string of newsworthy events, including major research updates at international oncology conferences and TIME naming Leqembi one of 2025’s Best Inventions. Despite these advances, Eisai’s 1-year total shareholder return is down 12.3% and it has shed over 40% in value over five years. However, the 90-day share price return has rebounded a notable 14.3%, suggesting that sentiment may be shifting on new growth prospects.

Curious about where other healthcare leaders are finding momentum? See the full list for free with our dedicated See the full list for free..

With shares still trading at a meaningful discount to analyst targets and recent gains attributed to breakthrough launches, it is time to ask: Is Eisai undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 9.7% Undervalued

Compared to the last close of ¥4,505, the narrative's fair value of ¥4,988 implies that analysts see meaningful upside from today's price. The narrative is built upon specific future growth drivers and margin improvements that could shift the market's stance.

The launch and approval of the home-administered SC-AI formulation for LEQEMBI, with high physician and patient anticipation, promises to unlock substantial incremental demand through enhanced convenience, improved treatment adherence, and reduced burden on healthcare systems. This could benefit both topline revenues and margins through operational efficiencies and lower administration costs.

Want to know what quantitative forces drive this narrative? The key factors are rising margins, ambitious profit growth, and a premium future earnings multiple. Curious about which bold assumptions shape the fair value? Discover what propels this healthy valuation and why consensus sees more runway ahead.

Result: Fair Value of ¥4,988 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, significant global drug pricing pressures and Eisai's reliance on a narrow drug portfolio could quickly diminish the company's earnings growth outlook.

Find out about the key risks to this Eisai narrative.

Another View: Caution from Multiples

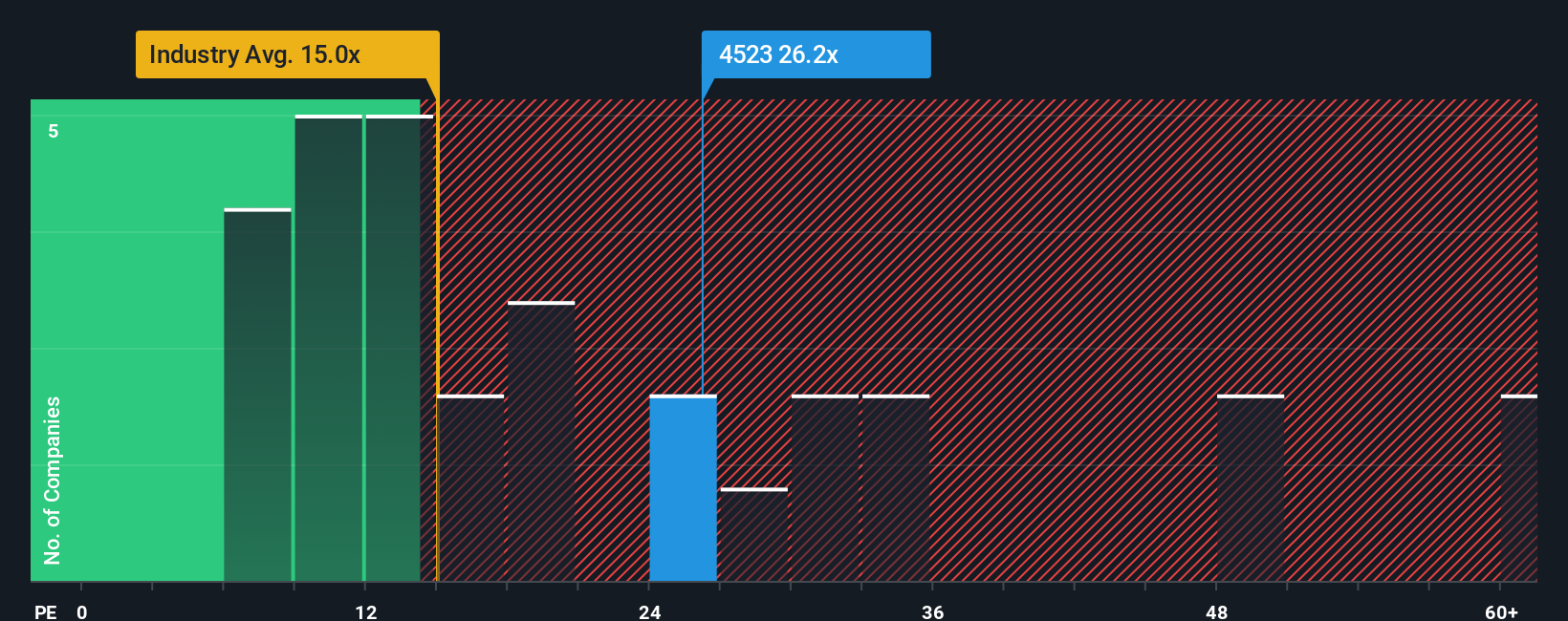

While fair value estimates suggest Eisai is undervalued, its price-to-earnings ratio stands at 25.2x, which is noticeably higher than both the industry average of 15.1x and the peer average of 19.4x. The fair ratio sits at 23.4x, implying the current market price already factors in optimistic future growth. Could this premium signal greater valuation risk for investors?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Eisai Narrative

If you have a different perspective or want to see the numbers for yourself, you can build a personalized valuation story quickly and easily. Do it your way

A great starting point for your Eisai research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Confident investing is all about finding the right opportunities before everyone else. Let Simply Wall Street’s tailored screeners help you take the next smart step.

- Jump on companies setting the pace in artificial intelligence by viewing these 24 AI penny stocks, which could redefine entire industries.

- Capture long-term value by targeting these 870 undervalued stocks based on cash flows with strong cash flow fundamentals and room for growth.

- Tap into robust yield potential by examining these 18 dividend stocks with yields > 3%. Each delivers consistent income above market averages.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eisai might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4523

Eisai

Engages in the research and development, manufacture, sale, and import and export of pharmaceuticals, and other business in Japan, America, China, Europe, Asia and internationally.

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor