- Japan

- /

- Hospitality

- /

- TSE:6412

Uncovering Three Small Caps With Strong Fundamentals

Reviewed by Simply Wall St

In the current market landscape, small-cap stocks have faced challenges as U.S. indices, including the S&P 600, experienced declines amid cautious Federal Reserve commentary and broad-based losses. Despite these hurdles, strong economic indicators such as robust GDP growth and rising retail sales suggest potential opportunities for investors willing to explore beyond the major indexes. In this environment, identifying small-cap companies with solid fundamentals becomes crucial for uncovering hidden value amidst broader market uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| AB Vilkyskiu pienine | 35.79% | 17.20% | 49.04% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Hermes Transportes Blindados | 50.88% | 4.57% | 3.33% | ★★★★★☆ |

| Intellego Technologies | 12.32% | 73.44% | 78.22% | ★★★★★☆ |

| HOMAG Group | NA | -31.14% | 23.43% | ★★★★★☆ |

| Inverfal PerúA | 31.20% | 10.56% | 17.83% | ★★★★★☆ |

| La Positiva Seguros y Reaseguros | 0.04% | 8.44% | 27.31% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Lavipharm | 39.21% | 9.47% | -15.70% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Kaken Pharmaceutical (TSE:4521)

Simply Wall St Value Rating: ★★★★★★

Overview: Kaken Pharmaceutical Co., Ltd. is engaged in the production, marketing, and sale of medical products, medical devices, and agrochemicals both in Japan and internationally with a market capitalization of ¥158.09 billion.

Operations: Kaken generates revenue primarily from its Pharmaceutical Business, which accounts for ¥84.81 billion, while its Real Estate segment contributes ¥2.44 billion. The company's net profit margin is a key financial indicator to consider when analyzing its profitability trends over time.

Kaken Pharmaceutical, a notable player in its field, has shown impressive earnings growth of 414% over the past year, outpacing the broader Pharmaceuticals industry. The company seems well-positioned financially with more cash than total debt and a reduced debt-to-equity ratio from 3.1 to 2.5 over five years. Its price-to-earnings ratio stands at 9.3x, which is below the JP market average of 13.5x, suggesting potential undervaluation. However, future earnings are forecasted to decline significantly by an average of 56% annually for the next three years, indicating challenges ahead despite its current profitability and high-quality past earnings.

- Unlock comprehensive insights into our analysis of Kaken Pharmaceutical stock in this health report.

Torii Pharmaceutical (TSE:4551)

Simply Wall St Value Rating: ★★★★★★

Overview: Torii Pharmaceutical Co., Ltd. is a company that manufactures and markets pharmaceutical products in Japan, with a market cap of ¥124.50 billion.

Operations: Torii Pharmaceutical generates revenue primarily from the manufacturing and marketing of pharmaceutical products in Japan. The company has a market capitalization of ¥124.50 billion, reflecting its valuation in the market.

Torii Pharmaceutical, a nimble player in the pharmaceutical sector, has showcased impressive earnings growth of 52.7% over the past year, outpacing the industry average of 12.2%. With no debt on its books for five years and high-quality earnings, Torii's financial health appears robust. Recently, Torii submitted a New Drug Application in Japan for TO-208 to treat Molluscum Contagiosum, marking a significant step in its collaboration with Verrica Pharmaceuticals. This move follows successful Phase 3 trials and aligns with prior U.S. approvals under the YCANTH® brand name since August 2023.

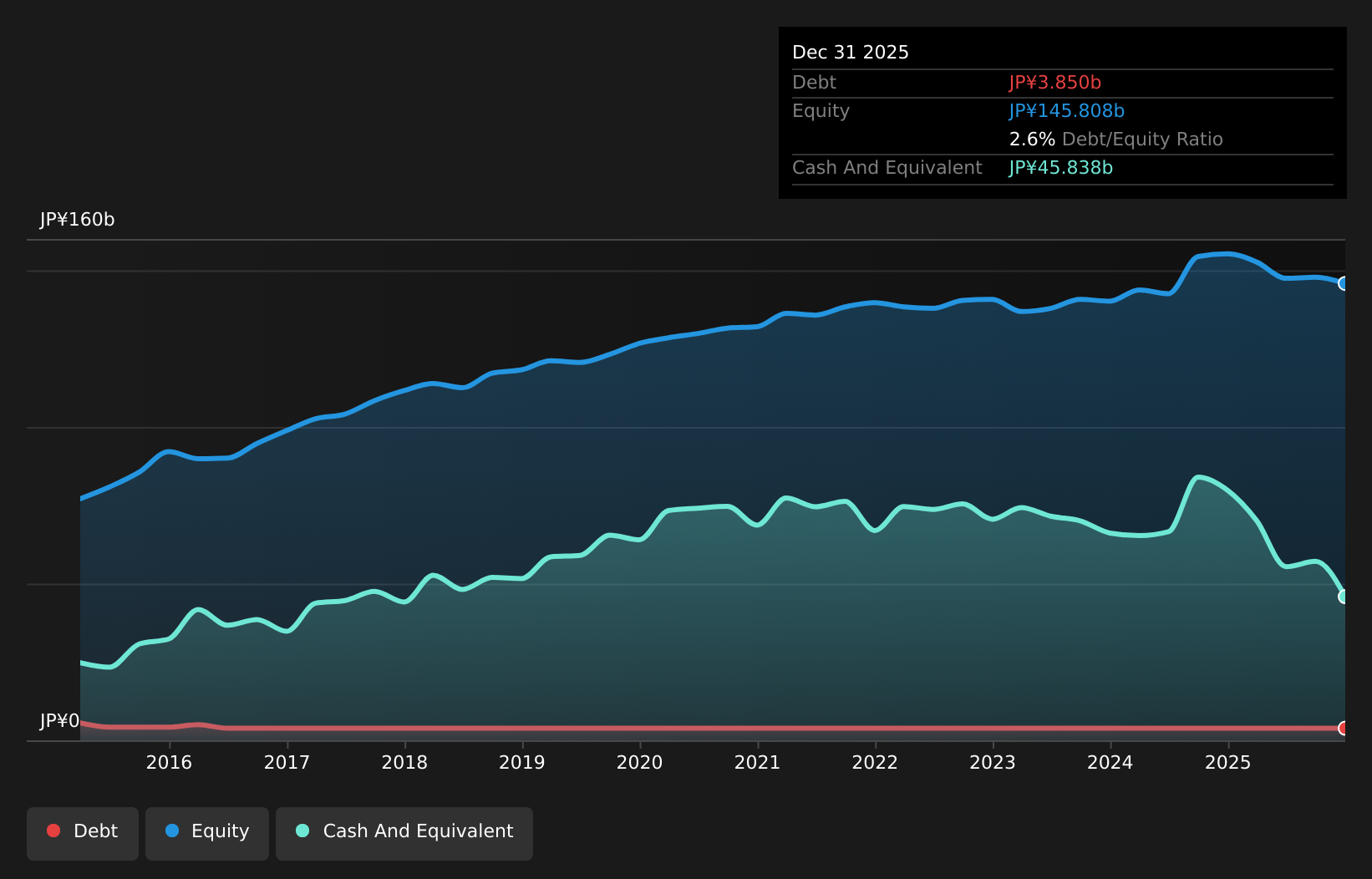

Heiwa (TSE:6412)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Heiwa Corporation develops, manufactures, and sells pachinko and pachislot machines in Japan with a market capitalization of approximately ¥234.73 billion.

Operations: Heiwa generates revenue primarily from its Pachislot and Pachinko Machine Business, contributing ¥43.30 billion, and its Golf Business, which adds ¥98.16 billion. The company's financial structure highlights a significant reliance on these two segments for income generation.

Heiwa, a promising player in its sector, shows potential with a Price-To-Earnings ratio of 12.1x, which is attractively below the JP market average of 13.5x. The company's net debt to equity ratio stands at a satisfactory 22.2%, reflecting prudent financial management over the past five years as it reduced from 50.1% to 45.7%. Although earnings growth last year at 13.1% lagged behind the Hospitality industry’s pace of 25.4%, Heiwa's high-quality earnings and robust EBIT coverage for interest payments (68.9x) underscore its solid operational footing and capacity for future expansion discussions like those involving PJC Investments acquisition plans.

- Click here to discover the nuances of Heiwa with our detailed analytical health report.

Understand Heiwa's track record by examining our Past report.

Where To Now?

- Embark on your investment journey to our 4633 Undiscovered Gems With Strong Fundamentals selection here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Heiwa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6412

Heiwa

Develops, manufactures, and sells pachinko and pachislot machines in Japan.

Reasonable growth potential with adequate balance sheet and pays a dividend.