Advertisement

### 3 Japanese Growth Stocks With Up To 33% Insider Ownership ###

Simply Wall St

Reviewed by Simply Wall St

Japan's stock markets have faced significant volatility recently, with the Nikkei 225 Index down 5.8% and the broader TOPIX Index losing 4.2%. Despite these challenges, growth companies with high insider ownership can offer stability and confidence to investors in uncertain times. In this article, we explore three Japanese growth stocks where insiders hold up to 33% ownership, providing a closer look at how strong internal commitment can signal potential resilience and long-term value.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 32.7% |

| Hottolink (TSE:3680) | 27% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 43.5% |

| Medley (TSE:4480) | 34% | 30.4% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 63% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| Astroscale Holdings (TSE:186A) | 21.3% | 90% |

| Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

| Soracom (TSE:147A) | 16.5% | 54.1% |

Let's take a closer look at a couple of our picks from the screened companies.

Avant Group (TSE:3836)

Simply Wall St Growth Rating: ★★★★☆☆

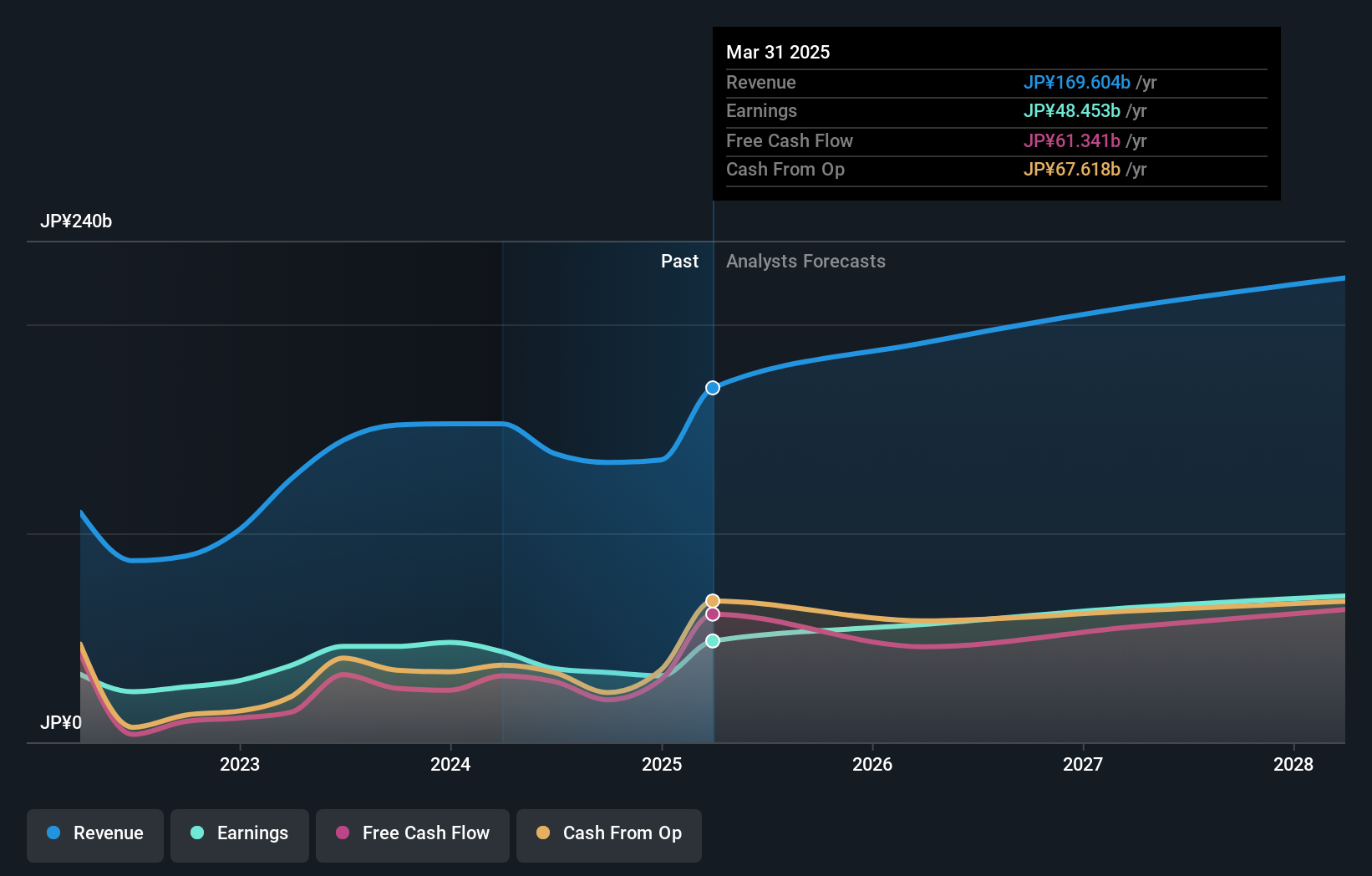

Overview: Avant Group Corporation, with a market cap of ¥71.55 billion, operates through its subsidiaries to provide accounting, business intelligence, and outsourcing services.

Operations: The company's revenue segments include the Management Solutions Business at ¥8.52 billion, Digital Transformation Promotion Business at ¥8.85 billion, and Consolidated Financial Statements Disclosure Business at ¥7.54 billion.

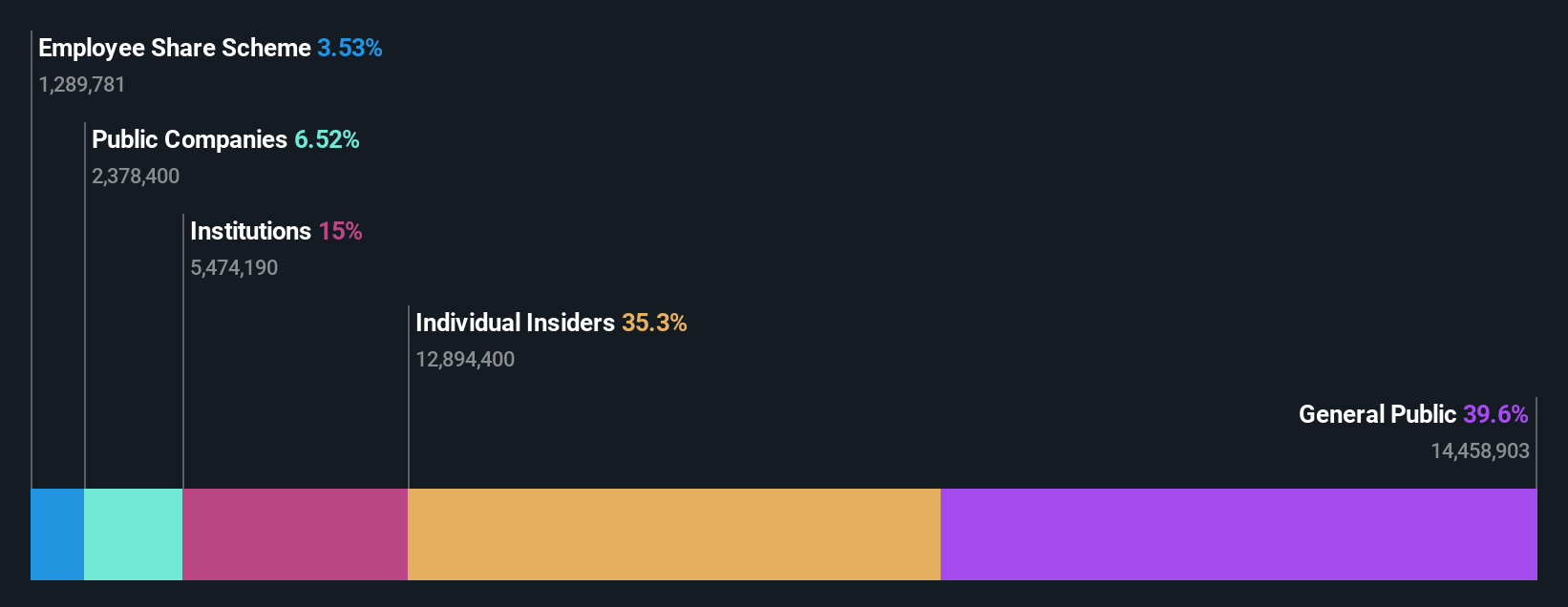

Insider Ownership: 34%

Avant Group demonstrates strong growth potential with earnings forecasted to grow 17.87% annually, outpacing the Japanese market's average. The company trades at 50.9% below estimated fair value, indicating potential undervaluation. Recent events include a dividend increase from ¥15.00 to ¥19.00 per share and a buyback of 364,100 shares for ¥477.64 million, reflecting confidence in its financial health and future prospects despite no significant insider trading activity recently observed.

- Unlock comprehensive insights into our analysis of Avant Group stock in this growth report.

- Our comprehensive valuation report raises the possibility that Avant Group is priced higher than what may be justified by its financials.

BayCurrent Consulting (TSE:6532)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BayCurrent Consulting, Inc. offers consulting services in Japan and has a market cap of ¥746.17 billion.

Operations: BayCurrent Consulting, Inc. generates revenue through consulting services in Japan.

Insider Ownership: 13.9%

BayCurrent Consulting showcases solid growth potential, with earnings forecasted to grow 18.71% annually, surpassing the Japanese market average of 8.6%. The stock trades at 42.9% below its estimated fair value, suggesting potential undervaluation. Despite no significant insider trading activity in the past three months, its high Return on Equity forecast of 34.7% in three years highlights strong financial performance prospects, supported by recent earnings growth of 16.8%.

- Click to explore a detailed breakdown of our findings in BayCurrent Consulting's earnings growth report.

- Our expertly prepared valuation report BayCurrent Consulting implies its share price may be too high.

Capcom (TSE:9697)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Capcom Co., Ltd. is a company that plans, develops, manufactures, sells, and distributes home video games, online games, mobile games, and arcade games both in Japan and internationally with a market cap of ¥1.36 trillion.

Operations: Capcom's revenue segments include Digital Content at ¥103.38 billion, Amusement Equipment at ¥10.34 billion, and Amusement Facilities at ¥20.09 billion.

Insider Ownership: 11.5%

Capcom is positioned for growth, with earnings forecasted to increase 14.5% annually, outpacing the Japanese market's 8.6%. Revenue is expected to grow at 9.5% per year, also above the market average of 4.2%. Despite a highly volatile share price recently and no significant insider trading activity in the past three months, Capcom's Return on Equity is projected to be strong at 20.4% in three years.

- Get an in-depth perspective on Capcom's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Capcom's share price might be on the expensive side.

Taking Advantage

- Discover the full array of 100 Fast Growing Japanese Companies With High Insider Ownership right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3836

Avant Group

Through its subsidiaries, provides accounting, business intelligence, and outsourcing services.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor