- Japan

- /

- Professional Services

- /

- TSE:6532

3 Japanese Growth Stocks With Up To 23% Insider Ownership

Reviewed by Simply Wall St

Amid a challenging week for global markets, Japan's stock indices have also faced significant declines, with the Nikkei 225 and TOPIX Index both registering losses. Despite these broader market challenges, growth companies with high insider ownership can offer unique opportunities for investors seeking stability and potential upside. In this article, we will explore three Japanese growth stocks that boast up to 23% insider ownership. High insider ownership often signals confidence in the company's future prospects and aligns management's interests with those of shareholders.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 32.7% |

| Hottolink (TSE:3680) | 27% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 43.5% |

| Medley (TSE:4480) | 34% | 30.4% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 63% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| Astroscale Holdings (TSE:186A) | 21.3% | 90% |

| Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

| AeroEdge (TSE:7409) | 10.7% | 25.3% |

Let's dive into some prime choices out of the screener.

freee K.K (TSE:4478)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: freee K.K. provides cloud-based accounting and HR software solutions in Japan and has a market cap of ¥157.28 billion.

Operations: The company generates revenue primarily from its platform business, which brought in ¥25.43 billion.

Insider Ownership: 23.9%

freee K.K. is expected to achieve substantial earnings growth of 72.57% per year and become profitable within the next three years, outpacing average market growth. Its revenue is forecasted to grow at 18.3% annually, faster than the Japanese market's 4.2%. Recently, freee K.K. proposed amendments to its articles of incorporation to support business expansion and provided guidance for fiscal year ending June 2025 with net sales expected at ¥33.06 billion (US$0.23 billion).

- Get an in-depth perspective on freee K.K's performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that freee K.K is priced lower than what may be justified by its financials.

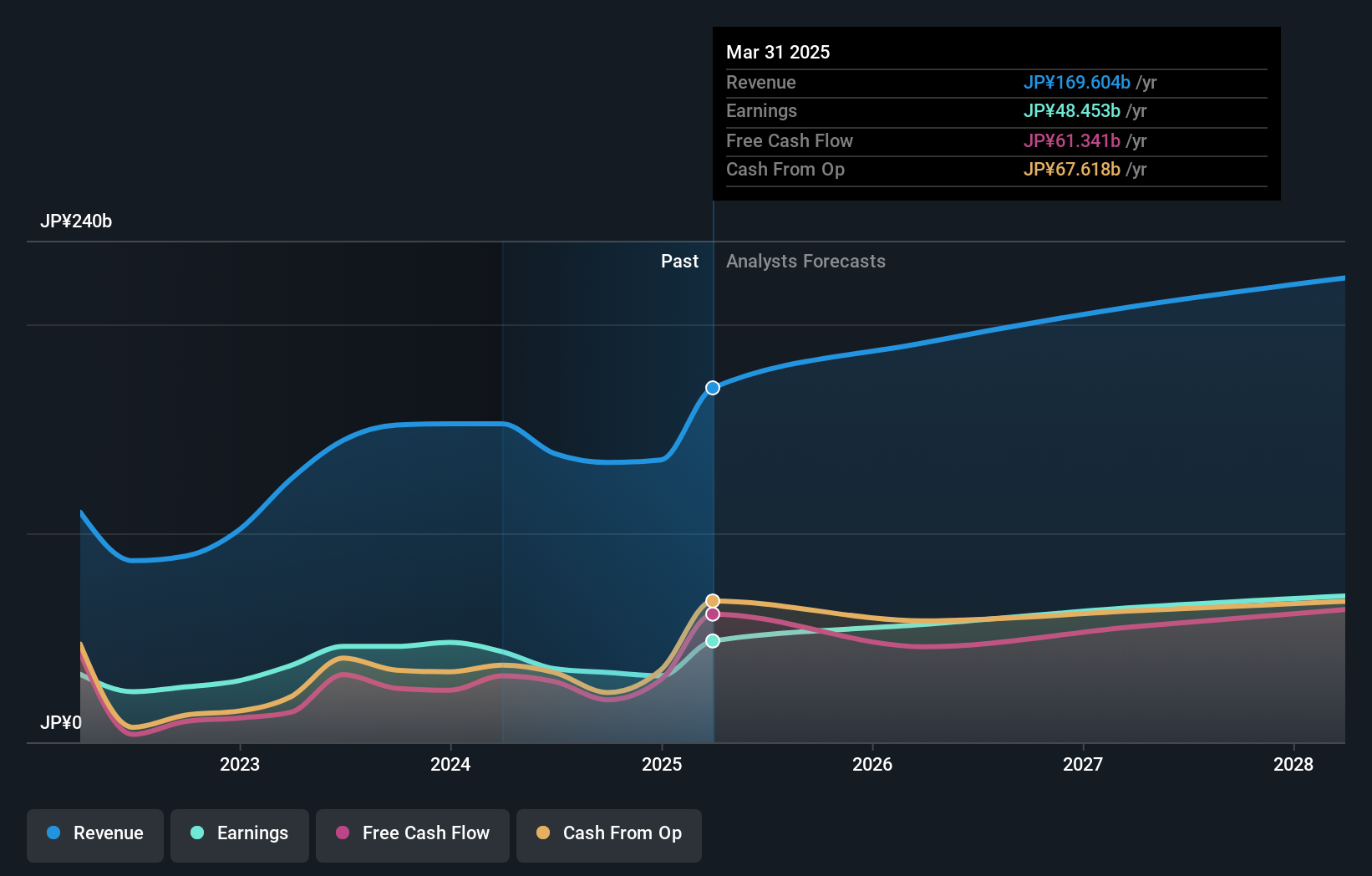

BayCurrent Consulting (TSE:6532)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BayCurrent Consulting, Inc., with a market cap of ¥746.17 billion, provides consulting services in Japan.

Operations: BayCurrent Consulting, Inc. generates revenue through its consulting services in Japan.

Insider Ownership: 13.9%

BayCurrent Consulting is expected to achieve annual earnings growth of 18.71%, outpacing the Japanese market's 8.6%. Its revenue is forecasted to grow at 18.6% per year, significantly faster than the market's 4.2%. Trading at a substantial discount of 42.9% below its estimated fair value, BayCurrent also boasts a high forecasted Return on Equity of 34.7% in three years, indicating strong future profitability and efficient capital use.

- Dive into the specifics of BayCurrent Consulting here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that BayCurrent Consulting is priced higher than what may be justified by its financials.

Capcom (TSE:9697)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Capcom Co., Ltd. is a global company that plans, develops, manufactures, sells, and distributes home video games, online games, mobile games, and arcade games with a market cap of ¥1.36 trillion.

Operations: Capcom's revenue segments include Digital Content at ¥103.38 billion, Amusement Equipment at ¥10.34 billion, and Amusement Facilities at ¥20.09 billion.

Insider Ownership: 11.5%

Capcom's earnings are forecast to grow at 14.5% per year, outpacing the Japanese market's 8.6%. Revenue growth is expected at 9.5% annually, also higher than the market average of 4.2%. Despite recent share price volatility, Capcom shows strong future profitability with a forecasted Return on Equity of 20.4% in three years. The company has scheduled its Q1 2025 earnings call for July 29, highlighting ongoing transparency and investor engagement.

- Click here and access our complete growth analysis report to understand the dynamics of Capcom.

- Upon reviewing our latest valuation report, Capcom's share price might be too optimistic.

Make It Happen

- Discover the full array of 100 Fast Growing Japanese Companies With High Insider Ownership right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if BayCurrent Consulting might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6532

Flawless balance sheet with reasonable growth potential.