Advertisement

TBS Holdings (TSE:9401) Valuation in Focus After Major Profit Forecast Upgrade

Simply Wall St

Reviewed by Kshitija Bhandaru

TBS Holdings Inc (TSE:9401) has raised its full-year profit guidance, increasing projected profit attributable to owners from JPY 27,500 million to JPY 52,500 million and nearly doubling expected earnings per share.

See our latest analysis for TBS HoldingsInc.

TBS Holdings Inc’s sharply upgraded earnings outlook has arrived just as momentum in the share price and investor optimism have started to cool off. While the stock surged 31.7% year-to-date, recent declines, including a 9% drop over the past 30 days, suggest traders are recalibrating after a long rally. That said, the three- and five-year total shareholder returns of over 200% still speak to the company’s capacity to deliver substantial long-term growth even as the pace may be moderating.

If this shift in sentiment has you curious about emerging opportunities, now is an ideal time to explore fast growing stocks with high insider ownership.

With earnings forecasts now looking significantly stronger, investors are left to wonder: does TBS Holdings’ current valuation underplay the improved outlook, or is the market already factoring in much of this future growth?

Price-to-Earnings of 16.9x: Is it justified?

With TBS Holdings Inc trading on a price-to-earnings (P/E) ratio of 16.9x at its last close of ¥5,152, the stock stands out as attractively valued compared to the broader Japanese media sector.

The P/E ratio reflects how much investors are willing to pay for each yen of the company’s earnings. For TBS Holdings Inc, a P/E of 16.9x indicates the market has moderate expectations of future growth and profitability. In the context of its solid earnings performance and media sector dynamics, this may suggest the price understates earnings power.

What makes this multiple compelling is its comparison to industry benchmarks. The current P/E is not only below the Japanese media industry average of 17.7x, but also well under the estimated fair P/E of 25x derived from valuation models. This further signals that the market could be discounting the company’s growth outlook relative to its peers and potential fair value levels.

Explore the SWS fair ratio for TBS HoldingsInc

Result: Price-to-Earnings of 16.9x (UNDERVALUED)

However, softer revenue and net income growth rates could challenge sustained optimism if competitive or market headwinds intensify in coming quarters.

Find out about the key risks to this TBS HoldingsInc narrative.

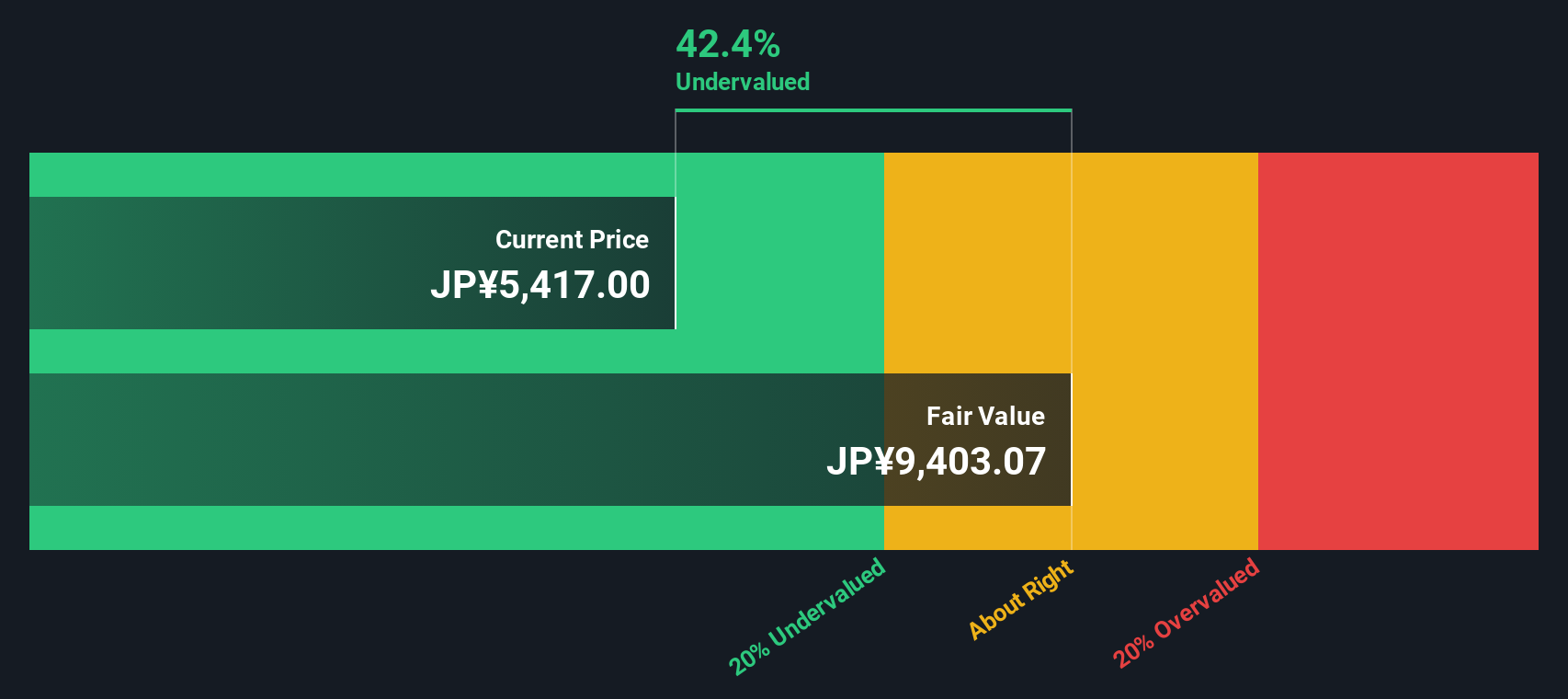

Another View: What Does the SWS DCF Model Say?

While the market multiple paints TBS Holdings as undervalued, our SWS DCF model takes a different angle by estimating the fair value at ¥9,524 per share, which is far above the current price. This suggests a much deeper undervaluation, but does this outlook hold up if growth slows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TBS HoldingsInc for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own TBS HoldingsInc Narrative

If you would rather form your own perspective or build your own story around the numbers, you can do so quickly and easily in just a few minutes. Do it your way.

A great starting point for your TBS HoldingsInc research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let market trends pass you by. Use the Simply Wall Street Screener to find stocks with untapped potential before everyone else does.

- Grow your passive income stream by accessing these 19 dividend stocks with yields > 3%, which offers solid yields and consistent performance above 3%.

- Secure your place in the next technological revolution with these 24 AI penny stocks, which powers advances in artificial intelligence and machine learning.

- Position yourself ahead of undervalued opportunities through these 901 undervalued stocks based on cash flows, based on strong cash flow fundamentals that many investors overlook.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TBS HoldingsInc might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9401

TBS HoldingsInc

Engages in the broadcasting and real estate businesses primarily in Japan.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor