Advertisement

CyberAgent (TSE:4751) Eyes Growth with AI and Gaming Investments Despite Financial Challenges

Simply Wall St

Reviewed by Simply Wall St

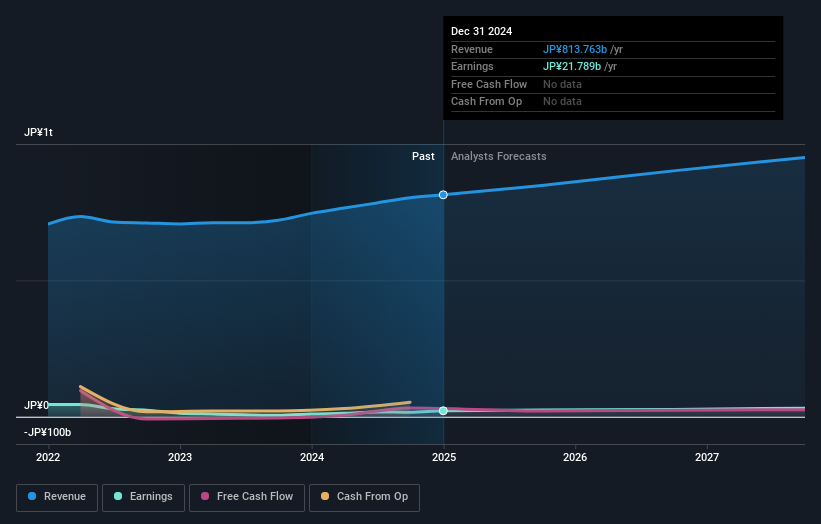

CyberAgent (TSE:4751) has been making headlines with its impressive earnings growth of 204.7% over the past year and a notable increase in net profit margin to 2%. The company's strategic focus on media, especially through ABEMA, has significantly contributed to its financial performance, while its advertising segment continues to outpace market growth. However, challenges such as a below-industry return on equity and volatility in the gaming sector highlight areas for improvement. The upcoming report will explore these core advantages, internal limitations, expansion opportunities, and competitive pressures shaping CyberAgent's trajectory.

Dive into the specifics of CyberAgent here with our thorough analysis report.

Core Advantages Driving Sustained Success for CyberAgent

CyberAgent has demonstrated remarkable financial health, with earnings growth of 204.7% over the past year, significantly surpassing its five-year average of 6.8%. This performance is further supported by a net profit margin increase to 2%, up from 0.7% the previous year. The company's strategic focus on media, particularly through ABEMA, has been pivotal. As noted by President Susumu Fujita, ABEMA's sales growth and reduced losses have substantially boosted overall sales and profitability. Additionally, the advertising segment has outpaced market growth, enhancing CyberAgent's competitive position. These strengths, combined with a reliable dividend history and a low payout ratio of 49.9%, underscore the company's solid financial foundation. Furthermore, the current share price of ¥1078, trading below the estimated fair value of ¥1534.84, suggests potential undervaluation, reinforcing investor confidence.

Internal Limitations Hindering CyberAgent's Growth

Despite its financial strengths, CyberAgent faces challenges, particularly in maintaining consistent returns. The return on equity stands at 8.1%, which is below the industry threshold of 20%, indicating room for improvement. The gaming sector's volatility, as highlighted by Fujita, presents ongoing challenges, with performance peaks and drops akin to Mount Fuji. Additionally, the company's Price-To-Earnings Ratio of 33.6x suggests it is expensive compared to industry and peer averages. A notable weakness is the ¥10.7B one-off loss impacting recent financial results, which highlights potential vulnerabilities in financial management. These factors, coupled with a forecasted earnings growth of 14.3% over three years, which lags behind industry standards, suggest areas needing strategic focus.

Areas for Expansion and Innovation for CyberAgent

CyberAgent's investment in AI for advertising offers promising avenues for enhanced effectiveness and growth. Fujita's emphasis on AI applications reflects a strategic move to leverage technology for competitive advantage. Moreover, the company's commitment to new game releases and intellectual property development, with five titles launched in FY 2024, positions it well for future growth in the gaming sector. This proactive approach to product diversification and innovation can help capitalize on emerging market opportunities. Additionally, with revenue growth projected at 5.6% per year, surpassing the JP market's 4.2%, CyberAgent is poised to strengthen its market position further.

Competitive Pressures and Market Risks Facing CyberAgent

While CyberAgent has shown resilience, it must navigate market volatility and competitive pressures. Fujita acknowledges the impact of seasonal and external factors on the advertising business, which could pose threats to stability. The company's strategic efforts to diversify content, as seen during events like the World Cup, aim to mitigate risks of over-reliance on specific content types. However, the presence of large one-off items in financial results introduces uncertainty, potentially affecting investor sentiment. Furthermore, the high valuation could deter potential investors, emphasizing the need for CyberAgent to maintain its growth trajectory and strategic agility in a dynamic market environment.

Conclusion

CyberAgent's impressive earnings growth of 204.7% over the past year, driven by strategic initiatives in media and advertising, highlights its strong financial foundation and potential for future profitability. However, challenges such as a return on equity of 8.1%, below industry standards, and a Price-To-Earnings Ratio of 33.6x indicate areas requiring strategic improvement, particularly in managing gaming sector volatility and financial vulnerabilities. The company's proactive investment in AI and new gaming titles positions it well for capitalizing on market opportunities, with projected revenue growth of 5.6% annually. Notably, the current share price of ¥1078, significantly below the estimated fair value of ¥1534.84, suggests an attractive investment opportunity, reinforcing confidence in CyberAgent's capacity to enhance shareholder value despite existing market pressures.

Next Steps

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4751

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor