Advertisement

- South Korea

- /

- Interactive Media and Services

- /

- KOSDAQ:A376300

March 2025 Asian Stocks Estimated To Be Below Fair Value

Simply Wall St

Reviewed by Simply Wall St

In March 2025, Asian markets are navigating a complex landscape marked by geopolitical tensions and varying economic growth forecasts. Amidst these challenges, investors are increasingly focused on identifying stocks that may be undervalued relative to their intrinsic worth, presenting potential opportunities for those who prioritize thorough analysis and a long-term perspective.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Consun Pharmaceutical Group (SEHK:1681) | HK$8.87 | HK$17.63 | 49.7% |

| RACCOON HOLDINGS (TSE:3031) | ¥957.00 | ¥1890.86 | 49.4% |

| Sichuan Kexin Mechanical and Electrical EquipmentLtd (SZSE:300092) | CN¥13.10 | CN¥25.69 | 49% |

| TechnoPro Holdings (TSE:6028) | ¥3306.00 | ¥6593.98 | 49.9% |

| S Foods (TSE:2292) | ¥2556.00 | ¥5084.09 | 49.7% |

| Bide Pharmatech (SHSE:688073) | CN¥54.00 | CN¥106.91 | 49.5% |

| Takara Bio (TSE:4974) | ¥866.00 | ¥1698.81 | 49% |

| ALUX (KOSDAQ:A475580) | ₩11250.00 | ₩22243.70 | 49.4% |

| Kinsus Interconnect Technology (TWSE:3189) | NT$93.10 | NT$182.94 | 49.1% |

| Zhejiang Juhua (SHSE:600160) | CN¥24.28 | CN¥47.60 | 49% |

We're going to check out a few of the best picks from our screener tool.

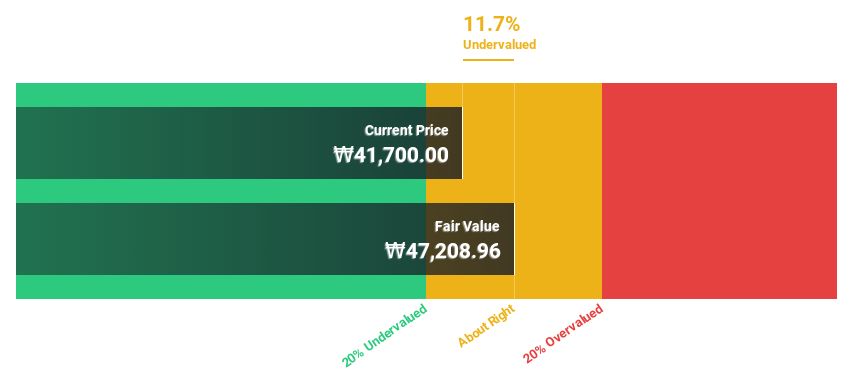

DEAR U (KOSDAQ:A376300)

Overview: Dear U Co., Ltd. is an information technology company with a market cap of approximately ₩956.66 billion.

Operations: Revenue Segments (in millions of ₩):null

Estimated Discount To Fair Value: 13.1%

DEAR U is trading at ₩41,000, approximately 13.1% below its estimated fair value of ₩47,183.6. Despite recent share price volatility, the company's earnings are projected to grow significantly at 31.4% annually over the next three years, outpacing the Korean market's growth rate of 22.9%. Revenue growth is also expected to be robust at 20.2% per year. The recent acquisition by SM Entertainment for KRW 95.57 billion underscores investor confidence in DEAR U's potential value based on cash flows and future performance expectations.

- Our growth report here indicates DEAR U may be poised for an improving outlook.

- Get an in-depth perspective on DEAR U's balance sheet by reading our health report here.

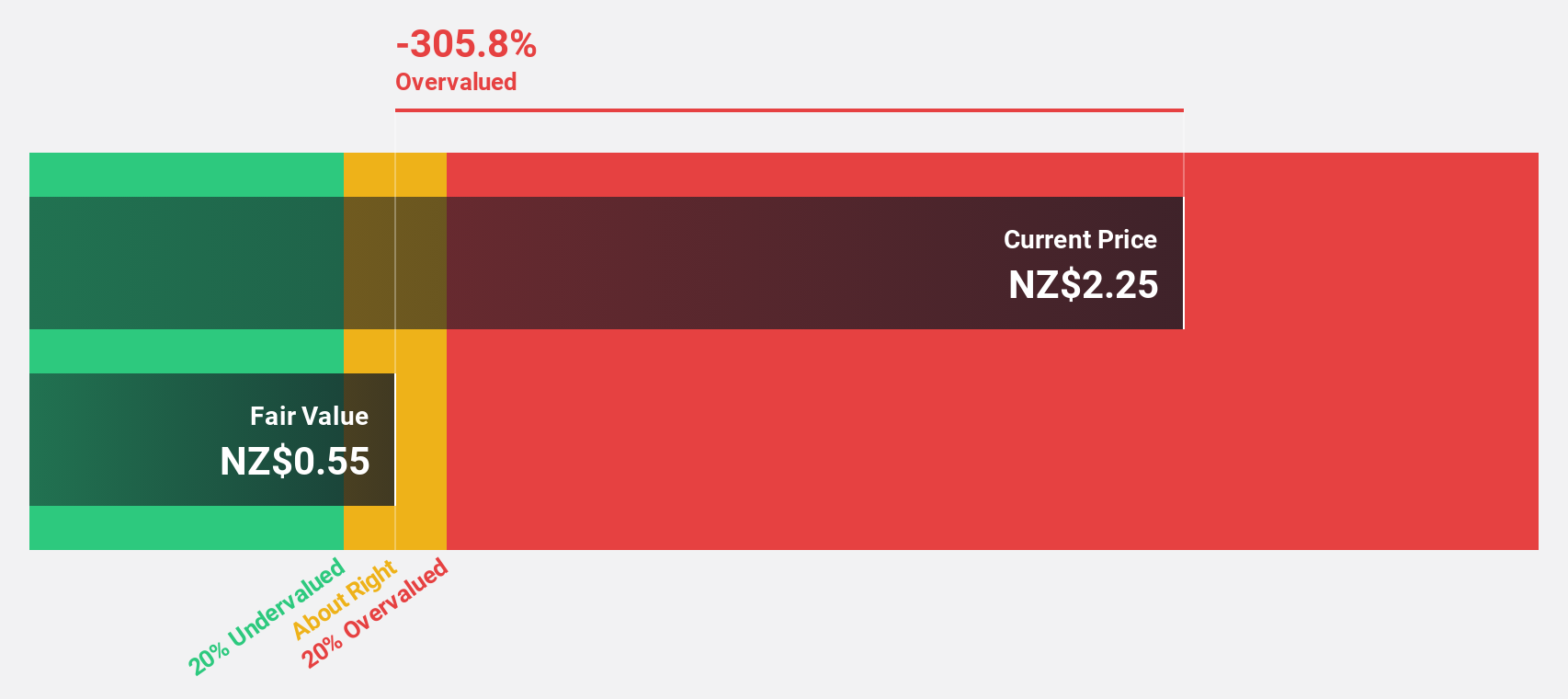

Ryman Healthcare (NZSE:RYM)

Overview: Ryman Healthcare Limited develops, owns, and operates integrated retirement villages, rest homes, and hospitals for elderly people in New Zealand and Australia with a market cap of NZ$2.70 billion.

Operations: The company generates revenue of NZ$720.35 million from its integrated retirement villages for older people in New Zealand and Australia.

Estimated Discount To Fair Value: 33.3%

Ryman Healthcare is trading at NZ$2.8, significantly below its estimated fair value of NZ$4.19, suggesting potential undervaluation based on cash flows. Despite recent shareholder dilution and high debt levels, the company is expected to become profitable within three years with earnings projected to grow 52% annually. Recent equity offerings totaling over NZ$1 billion indicate strategic efforts to strengthen its balance sheet amidst volatile share prices and moderate revenue growth forecasts of 7.9% per year.

- Our earnings growth report unveils the potential for significant increases in Ryman Healthcare's future results.

- Click to explore a detailed breakdown of our findings in Ryman Healthcare's balance sheet health report.

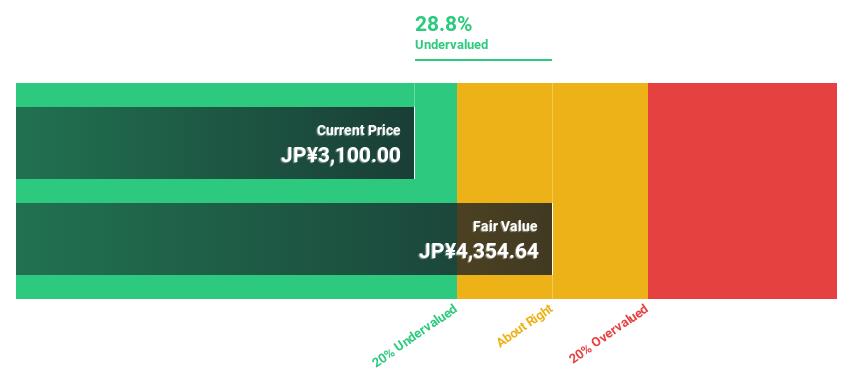

Akatsuki (TSE:3932)

Overview: Akatsuki Inc. operates in the gaming, comic, and other related sectors mainly within Japan, with a market capitalization of ¥45.93 billion.

Operations: The company's revenue is primarily derived from its game segment, which accounts for ¥21.13 billion, followed by the comics segment generating ¥1.18 billion.

Estimated Discount To Fair Value: 28.0%

Akatsuki, trading at ¥3140, is currently 28% below its estimated fair value of ¥4358.6, highlighting potential undervaluation based on cash flows. Despite recent shareholder dilution and high share price volatility over the past three months, Akatsuki became profitable this year. Its earnings are forecast to grow significantly at 43.5% annually over the next three years, outpacing the JP market's expected growth rate of 8%, while revenue is projected to increase by 16% per year.

- The growth report we've compiled suggests that Akatsuki's future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of Akatsuki.

Make It Happen

- Explore the 272 names from our Undervalued Asian Stocks Based On Cash Flows screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A376300

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor