Slammed 35% Hodogaya Chemical Co., Ltd. (TSE:4112) Screens Well Here But There Might Be A Catch

Hodogaya Chemical Co., Ltd. (TSE:4112) shareholders won't be pleased to see that the share price has had a very rough month, dropping 35% and undoing the prior period's positive performance. Indeed, the recent drop has reduced its annual gain to a relatively sedate 8.6% over the last twelve months.

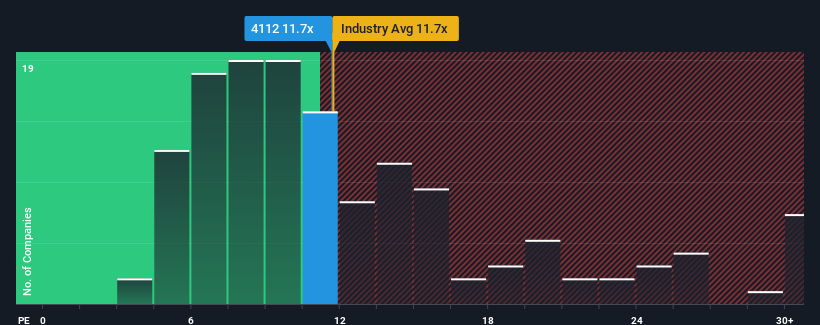

Although its price has dipped substantially, you could still be forgiven for feeling indifferent about Hodogaya Chemical's P/E ratio of 11.7x, since the median price-to-earnings (or "P/E") ratio in Japan is also close to 13x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Recent earnings growth for Hodogaya Chemical has been in line with the market. It seems that many are expecting the mediocre earnings performance to persist, which has held the P/E back. If you like the company, you'd be hoping this can at least be maintained so that you could pick up some stock while it's not quite in favour.

View our latest analysis for Hodogaya Chemical

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Hodogaya Chemical would need to produce growth that's similar to the market.

Retrospectively, the last year delivered a decent 11% gain to the company's bottom line. Still, lamentably EPS has fallen 21% in aggregate from three years ago, which is disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Shifting to the future, estimates from the only analyst covering the company suggest earnings should grow by 25% per annum over the next three years. That's shaping up to be materially higher than the 9.6% each year growth forecast for the broader market.

With this information, we find it interesting that Hodogaya Chemical is trading at a fairly similar P/E to the market. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Hodogaya Chemical's P/E

Hodogaya Chemical's plummeting stock price has brought its P/E right back to the rest of the market. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Hodogaya Chemical currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Having said that, be aware Hodogaya Chemical is showing 1 warning sign in our investment analysis, you should know about.

Of course, you might also be able to find a better stock than Hodogaya Chemical. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Hodogaya Chemical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4112

Hodogaya Chemical

Primarily engages in the production and sale of organic industrial chemicals in Japan.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Community Narratives