Advertisement

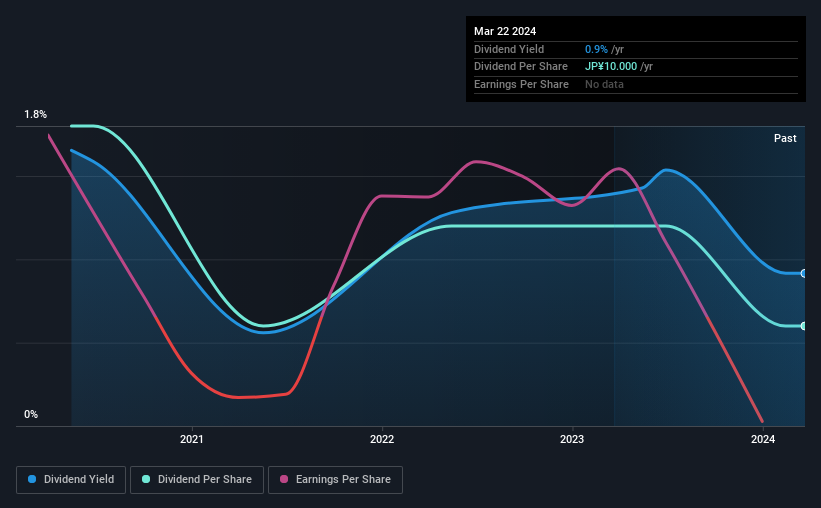

Titan Kogyo, Ltd. (TSE:4098) has announced that on 1st of July, it will be paying a dividend of¥10.00, which a reduction from last year's comparable dividend. This means that the annual payment is 0.9% of the current stock price, which is lower than what the rest of the industry is paying.

Check out our latest analysis for Titan Kogyo

Titan Kogyo's Distributions May Be Difficult To Sustain

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. Titan Kogyo is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

Assuming the trend of the last few years continues, EPS will grow by 0.6% over the next 12 months. While it is good to see income moving in the right direction, it still looks like the company won't achieve profitability. The positive free cash flows give us some comfort, however, that the dividend could continue to be sustained.

Titan Kogyo's Dividend Has Lacked Consistency

Looking back, the dividend has been unstable but with a relatively short history, we think it may be a bit early to draw conclusions about long term dividend sustainability. Since 2020, the annual payment back then was ¥30.00, compared to the most recent full-year payment of ¥10.00. The dividend has fallen 67% over that period. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

Titan Kogyo May Find It Hard To Grow The Dividend

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. However, Titan Kogyo's EPS was effectively flat over the past five years, which could stop the company from paying more every year. With EPS growth hard to come by and the company not turning a profit, we wouldn't be particularly optimistic about the growth prospects for Titan Kogyo's dividend in the future.

Our Thoughts On Titan Kogyo's Dividend

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For example, we've identified 2 warning signs for Titan Kogyo (1 is concerning!) that you should be aware of before investing. Is Titan Kogyo not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Titan Kogyo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4098

Titan Kogyo

Engages in the production and sale of industrial chemicals primarily in Japan.

Fair value with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor