Advertisement

Nihon Parkerizing's (TSE:4095) Shareholders Will Receive A Bigger Dividend Than Last Year

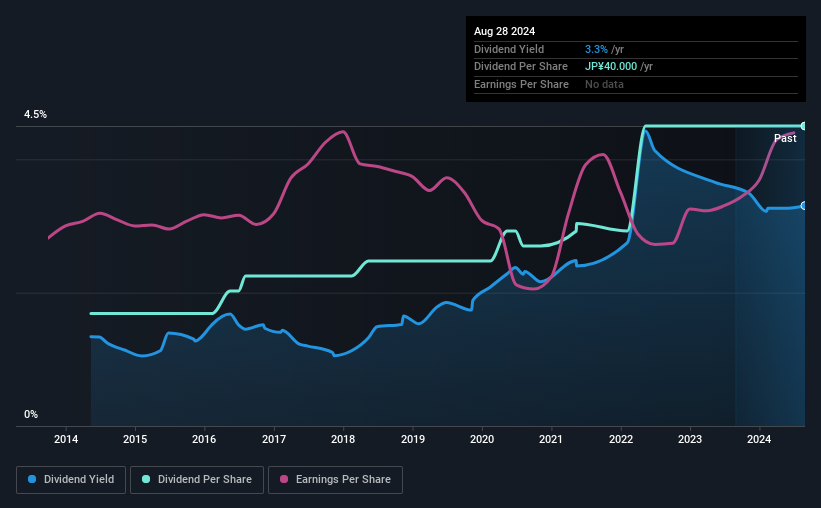

Nihon Parkerizing Co., Ltd.'s (TSE:4095) periodic dividend will be increasing on the 9th of December to ¥25.00, with investors receiving 25% more than last year's ¥20.00. This makes the dividend yield 3.3%, which is above the industry average.

View our latest analysis for Nihon Parkerizing

Nihon Parkerizing's Dividend Is Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much. However, Nihon Parkerizing's earnings easily cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

Looking forward, earnings per share could rise by 3.2% over the next year if the trend from the last few years continues. Assuming the dividend continues along recent trends, we think the payout ratio could be 42% by next year, which is in a pretty sustainable range.

Nihon Parkerizing Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of ¥15.00 in 2014 to the most recent total annual payment of ¥40.00. This works out to be a compound annual growth rate (CAGR) of approximately 10% a year over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

Dividend Growth May Be Hard To Achieve

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Earnings per share has been crawling upwards at 3.2% per year. If Nihon Parkerizing is struggling to find viable investments, it always has the option to increase its payout ratio to pay more to shareholders.

We Really Like Nihon Parkerizing's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Earnings are easily covering distributions, and the company is generating plenty of cash. All in all, this checks a lot of the boxes we look for when choosing an income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Now, if you want to look closer, it would be worth checking out our free research on Nihon Parkerizing management tenure, salary, and performance. Is Nihon Parkerizing not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Nihon Parkerizing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4095

Nihon Parkerizing

Engages in the manufacture and supply of surface treatment chemicals in Japan and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|24.5% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|24.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|97.7% undervalued

RO

Community Contributor