If you have been keeping an eye on Rengo (TSE:3941), the recent movement in its stock price might have caught your attention, especially as investors weigh up what is driving sentiment. While there is no big headline event in the news, the steady activity has some market watchers wondering if this is just the usual ebb and flow or if there is something more significant under the surface.

Looking at the bigger picture, Rengo's shares have delivered moderate gains this year. Most of the momentum has built up over the past three months. Recent weeks brought stronger movement compared to its relatively flat performance over the past year. This suggests a shift in how the market perceives its prospects, whether due to changing fundamentals or simply the natural cycle in valuations.

After this period of renewed interest, is Rengo now offering value that the market has yet to recognize, or is everything already priced in?

Advertisement

Price-to-Earnings of 11.4x: Is It Justified?

Rengo currently trades at a price-to-earnings (P/E) ratio of 11.4x, slightly above both its peer group and industry averages. This positions the stock as relatively expensive on this widely followed valuation metric.

The price-to-earnings ratio reflects how much investors are willing to pay for every yen of the company's earnings. It is a key gauge in evaluating whether a company's share price is high or low relative to its earnings. In the packaging sector, stable cash flows and margins often lead to tight P/E ranges.

The fact that Rengo carries a higher P/E multiple than its peers might suggest that investors expect stronger profitability or growth than the competition. However, recent performance and forecasts indicate that this premium may not be justified given the company's earnings trajectory relative to industry averages.

However, slower revenue growth or unexpected shifts in packaging demand could quickly change investor sentiment and challenge the current valuation level.

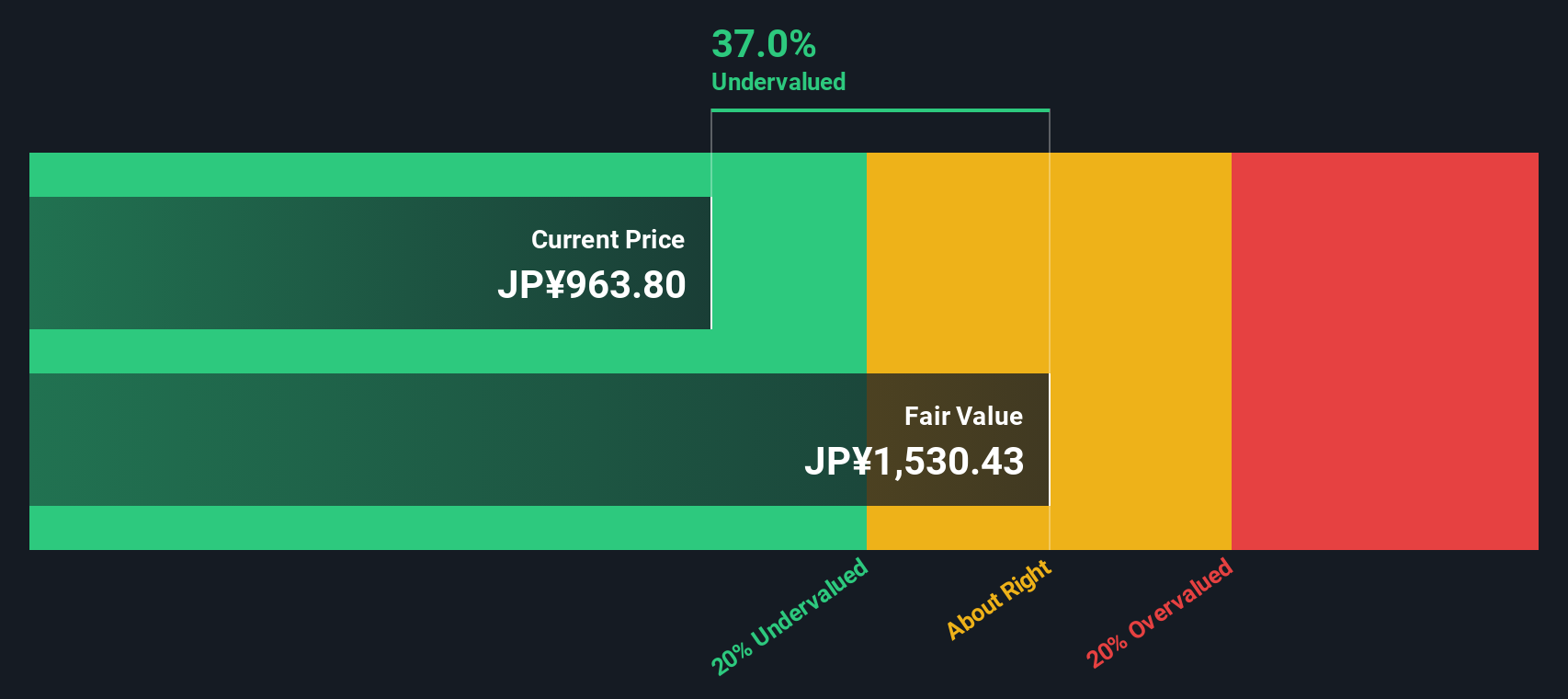

While the current market price appears elevated based on common valuation multiples, our DCF model presents a different perspective. The model indicates significant undervaluation, raising the question of whether the market is overlooking the long-term cash flow potential here.

Expand your investment horizons by tapping into exciting themes and companies, handpicked to spark fresh thinking and reveal new opportunities you do not want to miss.

Uncover overlooked gems with strong fundamentals by starting your search among penny stocks with strong financials. These stocks have the potential to surprise the market.

Capture growth from tomorrow’s tech by checking out AI penny stocks that are driving AI-powered transformation across various industries.

Boost your portfolio’s income stream with reliable payouts by exploring a suite of dividend stocks with yields > 3% with yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.