- Japan

- /

- Personal Products

- /

- TSE:4917

3 Stocks Estimated To Be Trading At Discounts Of Up To 12.5%

Reviewed by Simply Wall St

As global markets navigate a period of mixed performance, with most major stock indexes declining and only select sectors showing gains, investors are keenly observing economic indicators such as inflation rates and central bank policies. Amidst these fluctuations, the search for undervalued stocks becomes particularly pertinent as they may offer opportunities for value-oriented investors in an environment where growth stocks have recently outperformed. Identifying undervalued stocks involves assessing their intrinsic value compared to current market prices, especially when broader market conditions suggest potential discounts.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| UMB Financial (NasdaqGS:UMBF) | US$123.38 | US$244.22 | 49.5% |

| Sudarshan Chemical Industries (BSE:506655) | ₹1132.90 | ₹2237.94 | 49.4% |

| Business First Bancshares (NasdaqGS:BFST) | US$27.78 | US$54.95 | 49.4% |

| Absolent Air Care Group (OM:ABSO) | SEK254.00 | SEK506.18 | 49.8% |

| Equity Bancshares (NYSE:EQBK) | US$46.66 | US$92.69 | 49.7% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP291.50 | CLP578.67 | 49.6% |

| BYD Electronic (International) (SEHK:285) | HK$40.30 | HK$79.63 | 49.4% |

| Wetteri Oyj (HLSE:WETTERI) | €0.297 | €0.59 | 49.9% |

| Constellium (NYSE:CSTM) | US$11.01 | US$21.77 | 49.4% |

| Gold Road Resources (ASX:GOR) | A$2.12 | A$4.16 | 49% |

Let's uncover some gems from our specialized screener.

OceanaGold (Philippines) (PSE:OGP)

Overview: OceanaGold (Philippines) Inc. focuses on the exploration, development, production, and utilization of gold, copper, and other mineral resources in the Philippines with a market capitalization of ₱31.56 billion.

Operations: The company generates revenue primarily from its Metals & Mining segment, specifically in Gold & Other Precious Metals, amounting to $372.89 million.

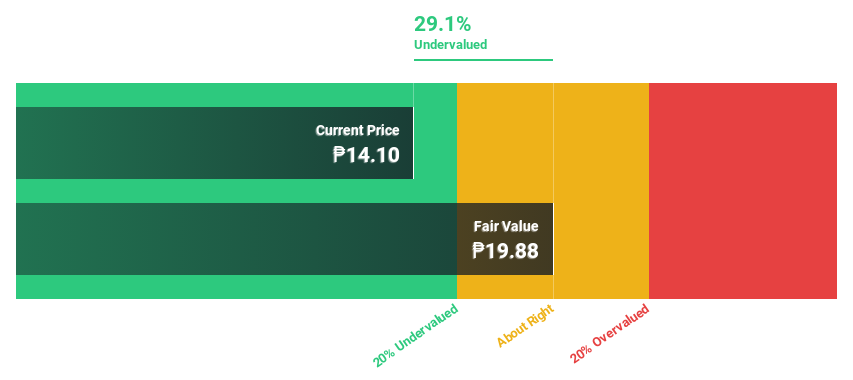

Estimated Discount To Fair Value: 29.1%

OceanaGold (Philippines) is trading at ₱14.1, significantly below its estimated fair value of ₱19.88, indicating it may be undervalued based on cash flows. Despite a decline in profit margins from 9.5% to 6.2%, the company's earnings are projected to grow substantially at 38.6% annually, outpacing the Philippine market's growth rate of 11.7%. Recent financials show improved quarterly sales and net income year-over-year, suggesting potential for future profitability enhancement despite current dividend coverage concerns.

- In light of our recent growth report, it seems possible that OceanaGold (Philippines)'s financial performance will exceed current levels.

- Click to explore a detailed breakdown of our findings in OceanaGold (Philippines)'s balance sheet health report.

Mandom (TSE:4917)

Overview: Mandom Corporation manufactures and sells cosmetics, perfumes, and quasi-drugs in Japan, Indonesia, and internationally with a market cap of ¥58.63 billion.

Operations: The company's revenue segments are comprised of ¥45.54 billion from Japan, ¥18.23 billion from Indonesia, and ¥21.42 billion from other overseas markets.

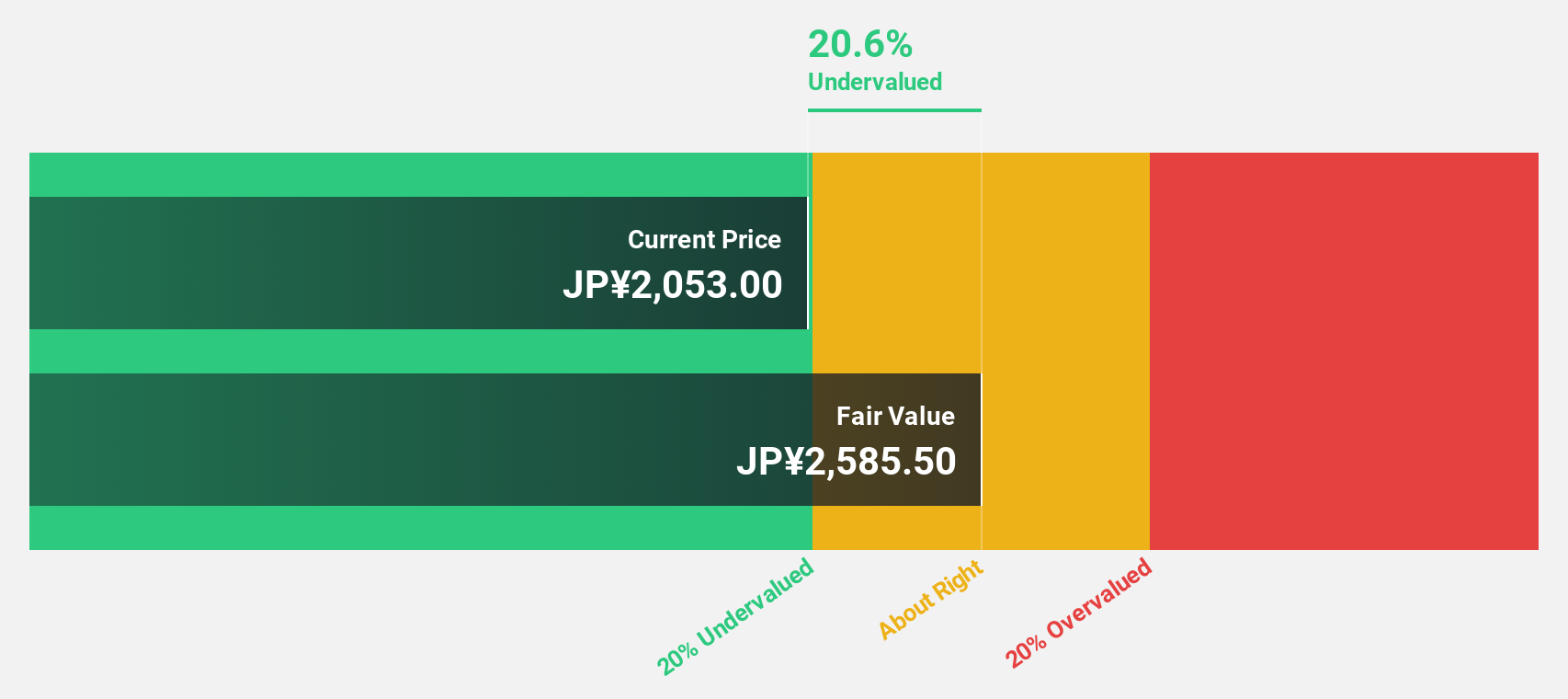

Estimated Discount To Fair Value: 12.5%

Mandom, trading at ¥1,320, is priced below its estimated fair value of ¥1,507.86. The company's earnings are projected to grow significantly at 27.13% annually over the next three years, surpassing the Japanese market's growth rate of 7.9%. Despite this positive outlook on earnings growth and reliable dividend yield of 3.03%, Mandom's forecasted return on equity remains low at 5.7%, which may temper investor enthusiasm for its undervaluation based on cash flows.

- Our earnings growth report unveils the potential for significant increases in Mandom's future results.

- Click here to discover the nuances of Mandom with our detailed financial health report.

Visual Photonics Epitaxy (TWSE:2455)

Overview: Visual Photonics Epitaxy Co., Ltd. specializes in the R&D, manufacturing, and sales of optoelectronic semiconductor epitaxy and components globally, with a market cap of NT$30.79 billion.

Operations: The company's revenue primarily comes from its Semiconductor Equipment and Services segment, which generated NT$3.46 billion.

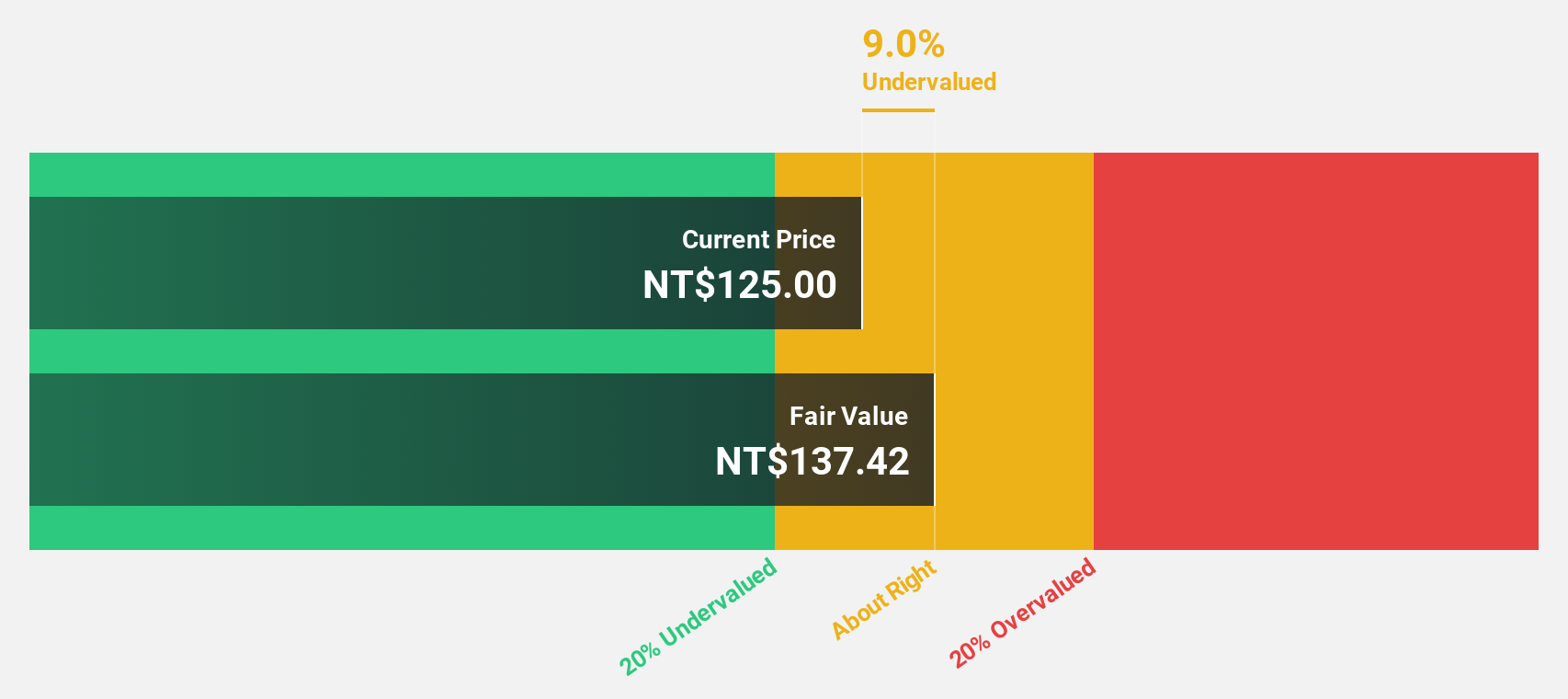

Estimated Discount To Fair Value: 7.5%

Visual Photonics Epitaxy, priced at NT$175, trades below its fair value estimate of NT$189.15. Although the company's earnings are set to grow significantly at 29.1% annually over the next three years, surpassing Taiwan's market growth rate of 6.1%, recent earnings reports show stable net income with significant year-over-year sales growth for nine months ended September 2024. Despite high forecasted return on equity reaching 30%, share price volatility may concern investors seeking undervaluation based on cash flows.

- The growth report we've compiled suggests that Visual Photonics Epitaxy's future prospects could be on the up.

- Get an in-depth perspective on Visual Photonics Epitaxy's balance sheet by reading our health report here.

Seize The Opportunity

- Explore the 880 names from our Undervalued Stocks Based On Cash Flows screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4917

Mandom

Engages in the manufacture and sale of cosmetics, perfumes, and quasi-drugs in Japan, Indonesia, and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives