- Japan

- /

- Personal Products

- /

- TSE:4452

Kao's (TSE:4452) Shareholders Will Receive A Bigger Dividend Than Last Year

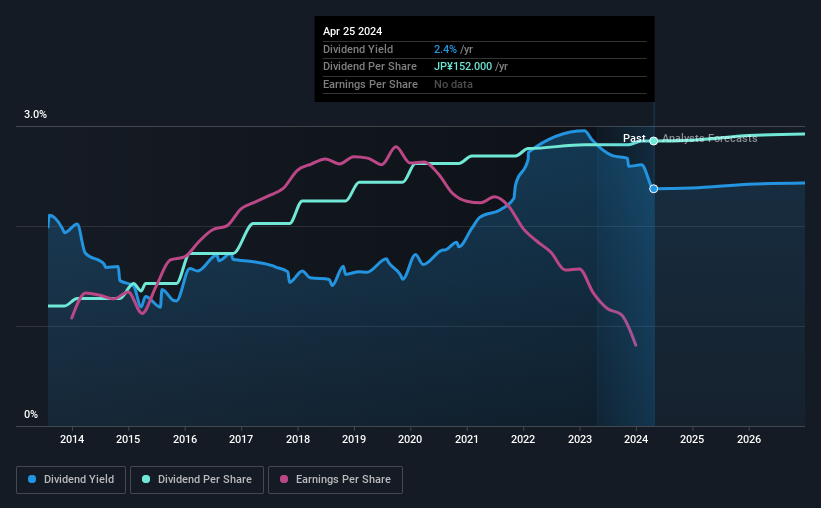

Kao Corporation (TSE:4452) has announced that it will be increasing its dividend from last year's comparable payment on the 2nd of September to ¥76.00. This takes the annual payment to 2.4% of the current stock price, which is about average for the industry.

See our latest analysis for Kao

Kao's Payment Has Solid Earnings Coverage

Solid dividend yields are great, but they only really help us if the payment is sustainable. Before making this announcement, Kao's dividend was higher than its profits, but the free cash flows quite comfortably covered it. Given that the dividend is a cash outflow, we think that cash is more important than accounting measures of profit when assessing the dividend, so this is a mitigating factor.

Over the next year, EPS is forecast to expand by 198.3%. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 58% which brings it into quite a comfortable range.

Kao Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2014, the dividend has gone from ¥64.00 total annually to ¥152.00. This works out to be a compound annual growth rate (CAGR) of approximately 9.0% a year over that time. Companies like this can be very valuable over the long term, if the decent rate of growth can be maintained.

The Dividend Has Limited Growth Potential

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. However, things aren't all that rosy. Over the past five years, it looks as though Kao's EPS has declined at around 21% a year. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Kao's payments are rock solid. The company is generating plenty of cash, but we still think the dividend is a bit high for comfort. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Taking the debate a bit further, we've identified 3 warning signs for Kao that investors need to be conscious of moving forward. Is Kao not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Kao might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4452

Kao

Develops and sells hygiene and living care, health and beauty care, life care, cosmetics, and chemical products.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives