Advertisement

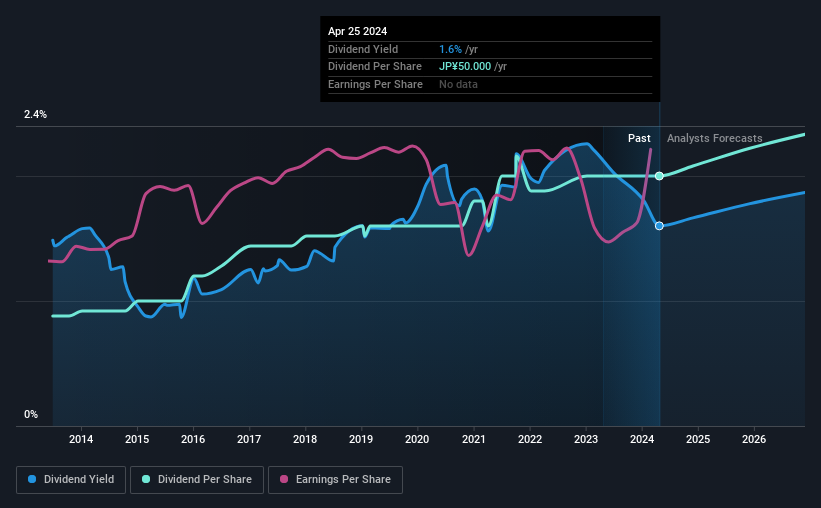

Kewpie Corporation's (TSE:2809) investors are due to receive a payment of ¥23.00 per share on 7th of August. Based on this payment, the dividend yield will be 1.6%, which is fairly typical for the industry.

Check out our latest analysis for Kewpie

Kewpie's Payment Has Solid Earnings Coverage

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue. Based on the last payment, Kewpie was paying only paying out a fraction of earnings, but the payment was a massive 111% of cash flows. The business might be trying to strike a balance between returning cash to shareholders and reinvesting back into the business, but this high of a payout ratio could definitely force the dividend to be cut if the company runs into a bit of a tough spot.

Over the next year, EPS is forecast to expand by 23.1%. If the dividend continues on this path, the payout ratio could be 34% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was ¥22.00 in 2014, and the most recent fiscal year payment was ¥50.00. This implies that the company grew its distributions at a yearly rate of about 8.6% over that duration. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Kewpie might have put its house in order since then, but we remain cautious.

Dividend Growth May Be Hard To Achieve

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. However, Kewpie's EPS was effectively flat over the past five years, which could stop the company from paying more every year. While growth may be thin on the ground, Kewpie could always pay out a higher proportion of earnings to increase shareholder returns.

In Summary

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Kewpie's payments, as there could be some issues with sustaining them into the future. While Kewpie is earning enough to cover the payments, the cash flows are lacking. This company is not in the top tier of income providing stocks.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For instance, we've picked out 1 warning sign for Kewpie that investors should take into consideration. Is Kewpie not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Kewpie might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2809

Kewpie

Through its subsidiaries, manufactures and sales food products in Japan and internationally.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor