Fuji Oil Holdings Inc. (TSE:2607) Stocks Shoot Up 25% But Its P/S Still Looks Reasonable

Despite an already strong run, Fuji Oil Holdings Inc. (TSE:2607) shares have been powering on, with a gain of 25% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 38% in the last year.

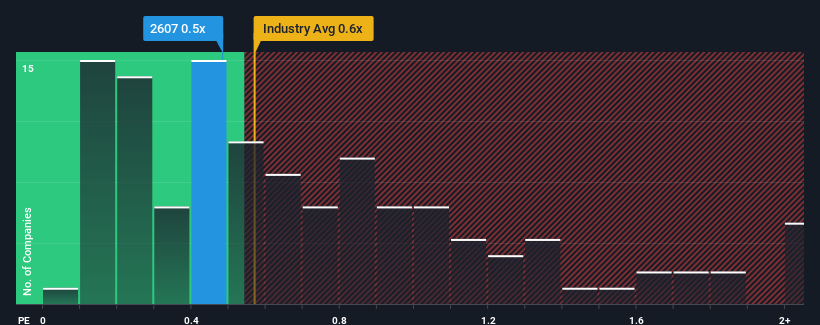

Although its price has surged higher, there still wouldn't be many who think Fuji Oil Holdings' price-to-sales (or "P/S") ratio of 0.5x is worth a mention when the median P/S in Japan's Food industry is similar at about 0.6x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Fuji Oil Holdings

What Does Fuji Oil Holdings' Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Fuji Oil Holdings has been relatively sluggish. Perhaps the market is expecting future revenue performance to lift, which has kept the P/S from declining. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Fuji Oil Holdings will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The P/S?

The only time you'd be comfortable seeing a P/S like Fuji Oil Holdings' is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a decent 4.4% gain to the company's revenues. The latest three year period has also seen an excellent 54% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 3.2% per annum as estimated by the five analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 3.7% each year, which is not materially different.

In light of this, it's understandable that Fuji Oil Holdings' P/S sits in line with the majority of other companies. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Final Word

Its shares have lifted substantially and now Fuji Oil Holdings' P/S is back within range of the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've seen that Fuji Oil Holdings maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. If all things remain constant, the possibility of a drastic share price movement remains fairly remote.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Fuji Oil Holdings (1 shouldn't be ignored!) that you should be aware of before investing here.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2607

Fuji Oil Holdings

Develops, produces, and sells a range of food ingredients in Japan and internationally.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives