Advertisement

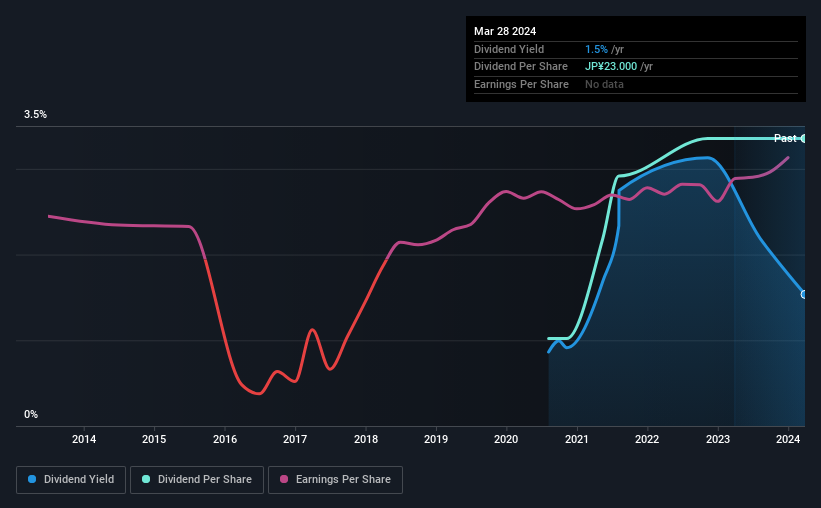

The board of Nagaoka International Corporation (TSE:6239) has announced that it will be increasing its dividend by 30% on the 29th of September to ¥30.00, up from last year's comparable payment of ¥23.00. Even though the dividend went up, the yield is still quite low at only 1.5%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Nagaoka International's stock price has increased by 46% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

View our latest analysis for Nagaoka International

Nagaoka International's Payment Has Solid Earnings Coverage

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Before making this announcement, Nagaoka International was easily earning enough to cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS could expand by 42.1% if recent trends continue. Assuming the dividend continues along recent trends, we think the payout ratio could be 16% by next year, which is in a pretty sustainable range.

Nagaoka International Doesn't Have A Long Payment History

The dividend has been pretty stable looking back, but the company hasn't been paying one for very long. This makes it tough to judge how it would fare through a full economic cycle. Since 2020, the dividend has gone from ¥7.00 total annually to ¥23.00. This means that it has been growing its distributions at 35% per annum over that time. Nagaoka International has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Nagaoka International has seen EPS rising for the last five years, at 42% per annum. Earnings per share is growing at a solid clip, and the payout ratio is low which we think is an ideal combination in a dividend stock as the company can quite easily raise the dividend in the future.

We Really Like Nagaoka International's Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 2 warning signs for Nagaoka International that investors should know about before committing capital to this stock. Is Nagaoka International not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Nagaoka International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6239

Nagaoka International

Develops and sells water intake and treatment systems, and screen internals to oil refining and petrochemical industries in Japan and internationally.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor