ORIX Corporation (TSE:8591) has announced that it will be increasing its dividend from last year's comparable payment on the 5th of June to ¥51.20. Based on this payment, the dividend yield for the company will be 3.1%, which is fairly typical for the industry.

Check out our latest analysis for ORIX

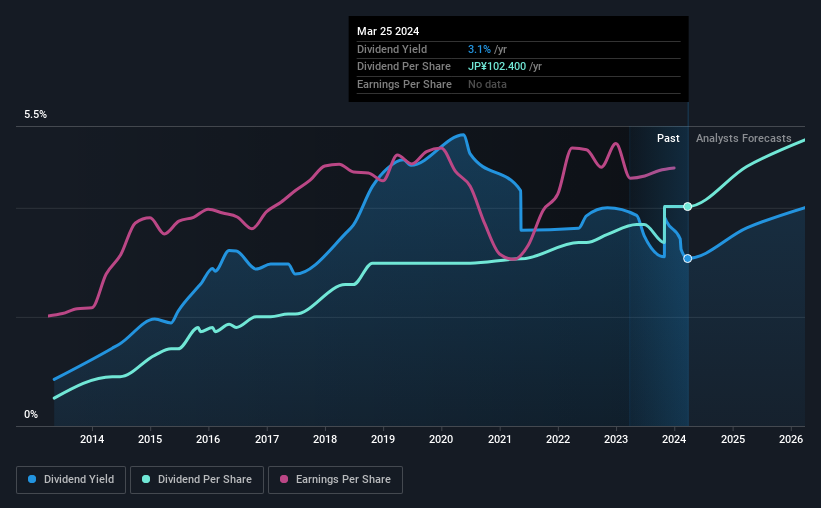

ORIX's Dividend Is Well Covered By Earnings

Unless the payments are sustainable, the dividend yield doesn't mean too much. Prior to this announcement, ORIX's dividend was only 36% of earnings, however it was paying out 1,785% of free cash flows. The business might be trying to strike a balance between returning cash to shareholders and reinvesting back into the business, but this high of a payout ratio could definitely force the dividend to be cut if the company runs into a bit of a tough spot.

The next year is set to see EPS grow by 62.2%. If the dividend continues on this path, the payout ratio could be 27% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The dividend has gone from an annual total of ¥13.00 in 2014 to the most recent total annual payment of ¥102.40. This works out to be a compound annual growth rate (CAGR) of approximately 23% a year over that time. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. However, ORIX's EPS was effectively flat over the past five years, which could stop the company from paying more every year. While growth may be thin on the ground, ORIX could always pay out a higher proportion of earnings to increase shareholder returns.

In Summary

Overall, we always like to see the dividend being raised, but we don't think ORIX will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 2 warning signs for ORIX that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8591

ORIX

Provides diversified financial services in Japan, the United States, Asia, Europe, Australasia, and the Middle East.

Very undervalued with proven track record.