- Japan

- /

- Diversified Financial

- /

- TSE:7191

Entrust Inc. (TSE:7191) Looks Like A Good Stock, And It's Going Ex-Dividend Soon

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Entrust Inc. (TSE:7191) is about to trade ex-dividend in the next three days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. Thus, you can purchase Entrust's shares before the 27th of September in order to receive the dividend, which the company will pay on the 4th of December.

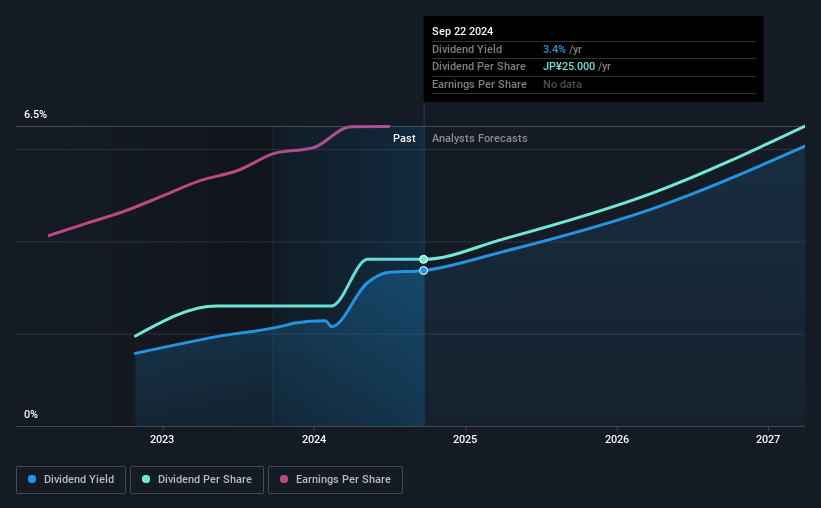

The company's next dividend payment will be JP¥12.50 per share. Last year, in total, the company distributed JP¥25.00 to shareholders. Calculating the last year's worth of payments shows that Entrust has a trailing yield of 3.4% on the current share price of JP¥742.00. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Entrust can afford its dividend, and if the dividend could grow.

View our latest analysis for Entrust

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Entrust paid out a comfortable 33% of its profit last year.

When a company paid out less in dividends than it earned in profit, this generally suggests its dividend is affordable. The lower the % of its profit that it pays out, the greater the margin of safety for the dividend if the business enters a downturn.

Click here to see how much of its profit Entrust paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. With that in mind, it's good to see earnings have grown 9.5% on last year.

One year is not very long in the grand scheme of things though, so we wouldn't draw too strong a conclusion based on these results.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Entrust has delivered an average of 36% per year annual increase in its dividend, based on the past two years of dividend payments. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

To Sum It Up

Should investors buy Entrust for the upcoming dividend? Entrust has seen its earnings per share grow slowly in recent years, and the company reinvests more than half of its profits in the business, which generally bodes well for its future prospects. In summary, Entrust appears to have some promise as a dividend stock, and we'd suggest taking a closer look at it.

With that in mind, a critical part of thorough stock research is being aware of any risks that stock currently faces. For example - Entrust has 1 warning sign we think you should be aware of.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Entrust might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7191

Flawless balance sheet with moderate growth potential.

Market Insights

Community Narratives