December 2024's Noteworthy Stocks Estimated To Be Priced Below Intrinsic Value

Reviewed by Simply Wall St

As December 2024 unfolds, global markets present a mixed picture with major U.S. stock indexes hitting record highs amid a rally in growth stocks, while value segments and smaller-cap indices like the Russell 2000 see declines. With geopolitical events in Europe and economic data from the U.S. shaping investor sentiment, identifying stocks potentially priced below their intrinsic value becomes crucial for those seeking opportunities amidst diverse market conditions. In this environment, a good stock is often characterized by strong fundamentals that remain resilient despite broader market fluctuations and political uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Shandong Bailong Chuangyuan Bio-Tech (SHSE:605016) | CN¥16.64 | CN¥33.16 | 49.8% |

| NBT Bancorp (NasdaqGS:NBTB) | US$50.26 | US$99.93 | 49.7% |

| Gaming Realms (AIM:GMR) | £0.36 | £0.72 | 49.7% |

| Management SolutionsLtd (TSE:7033) | ¥1713.00 | ¥3407.79 | 49.7% |

| West Bancorporation (NasdaqGS:WTBA) | US$23.32 | US$46.38 | 49.7% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP289.40 | CLP576.08 | 49.8% |

| EnomotoLtd (TSE:6928) | ¥1450.00 | ¥2884.09 | 49.7% |

| Nidaros Sparebank (OB:NISB) | NOK99.60 | NOK198.62 | 49.9% |

| Visional (TSE:4194) | ¥8500.00 | ¥16990.44 | 50% |

| Zalando (XTRA:ZAL) | €34.70 | €69.28 | 49.9% |

Let's dive into some prime choices out of the screener.

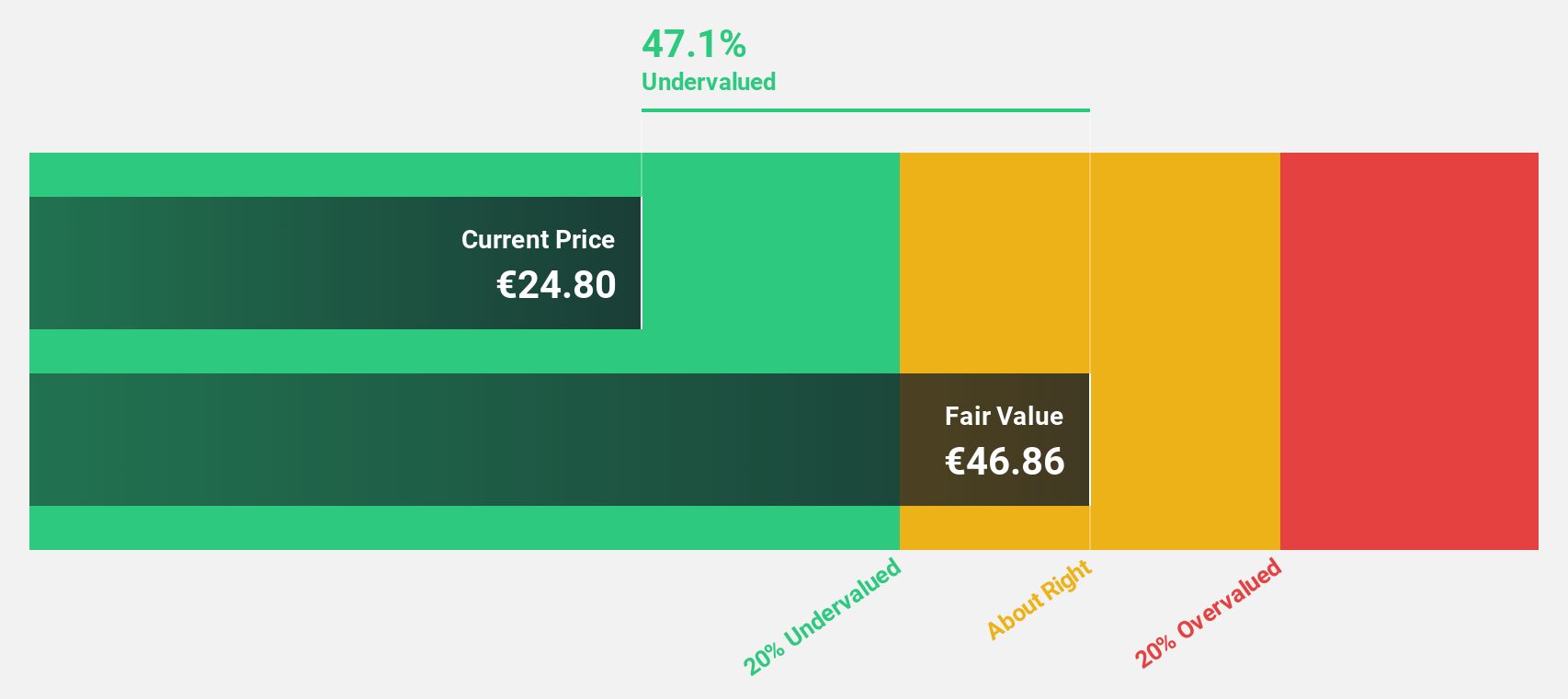

Lectra (ENXTPA:LSS)

Overview: Lectra SA offers industrial intelligence solutions tailored for the fashion, automotive, and furniture industries across Northern Europe, Southern Europe, the Americas, and the Asia Pacific with a market cap of €1.08 billion.

Operations: The company's revenue segments include €172.19 million from the Americas and €124.33 million from the Asia-Pacific region.

Estimated Discount To Fair Value: 30.3%

Lectra is trading at €28.35, significantly below its estimated fair value of €40.66, suggesting it may be undervalued based on cash flows. Despite recent earnings showing a decline in net income to €22.77 million from €25.87 million, the company's annual profit growth is forecasted at 25.6%, outpacing the French market's 12.5%. While revenue growth is modest at 5.7% annually, Lectra's strong earnings potential supports its valuation appeal.

- Our growth report here indicates Lectra may be poised for an improving outlook.

- Dive into the specifics of Lectra here with our thorough financial health report.

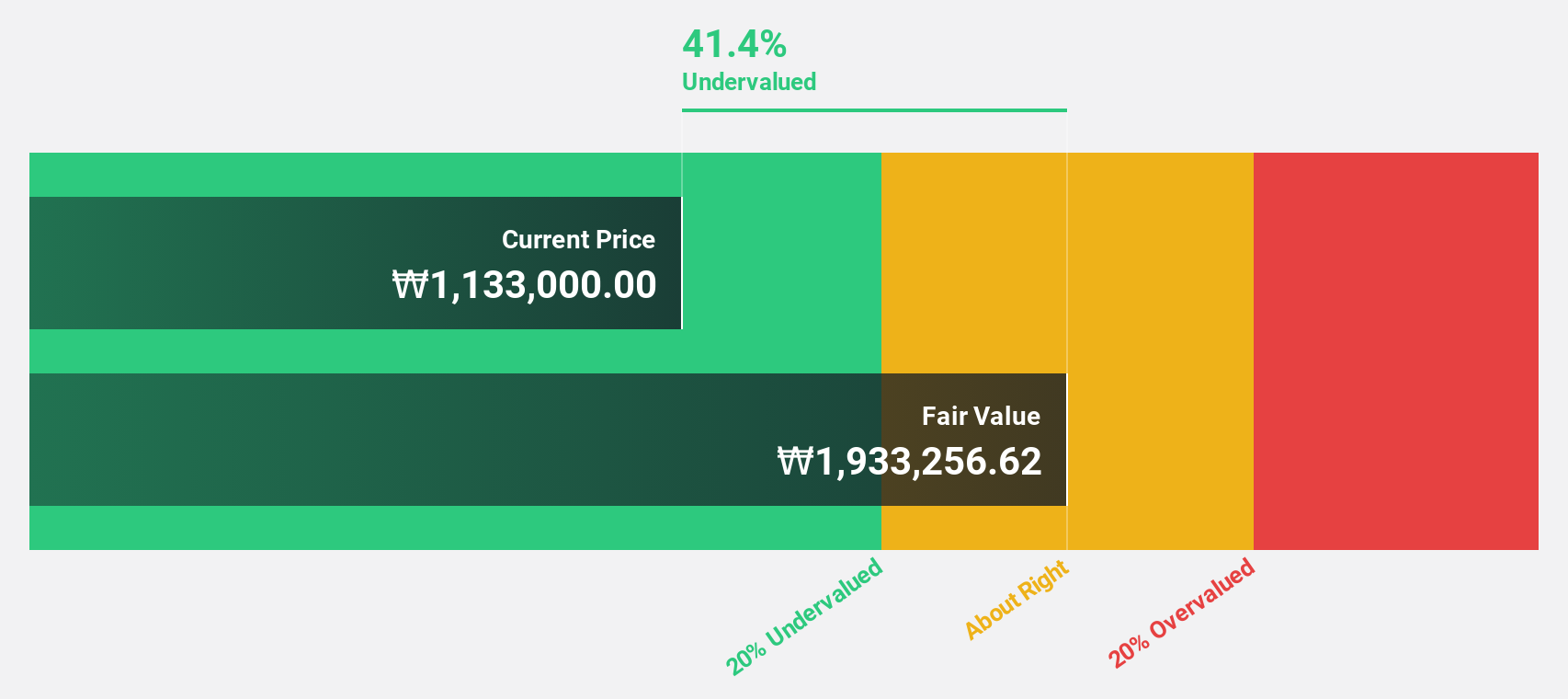

Samyang Foods (KOSE:A003230)

Overview: Samyang Foods Co., Ltd., along with its subsidiaries, operates in the food industry both domestically in South Korea and internationally, with a market capitalization of ₩4.46 trillion.

Operations: Revenue Segments (in millions of ₩):

Estimated Discount To Fair Value: 41.8%

Samyang Foods, trading at ₩668,000, is considerably undervalued with a fair value estimate of ₩1.15 million. The company's revenue is expected to grow at 17.1% annually, surpassing the Korean market's average growth rate of 8.9%. Although its earnings growth forecast of 22.6% per year lags behind the market's 28.7%, Samyang Foods' robust earnings expansion and high future return on equity (30.5%) highlight its investment potential based on cash flows.

- Our comprehensive growth report raises the possibility that Samyang Foods is poised for substantial financial growth.

- Get an in-depth perspective on Samyang Foods' balance sheet by reading our health report here.

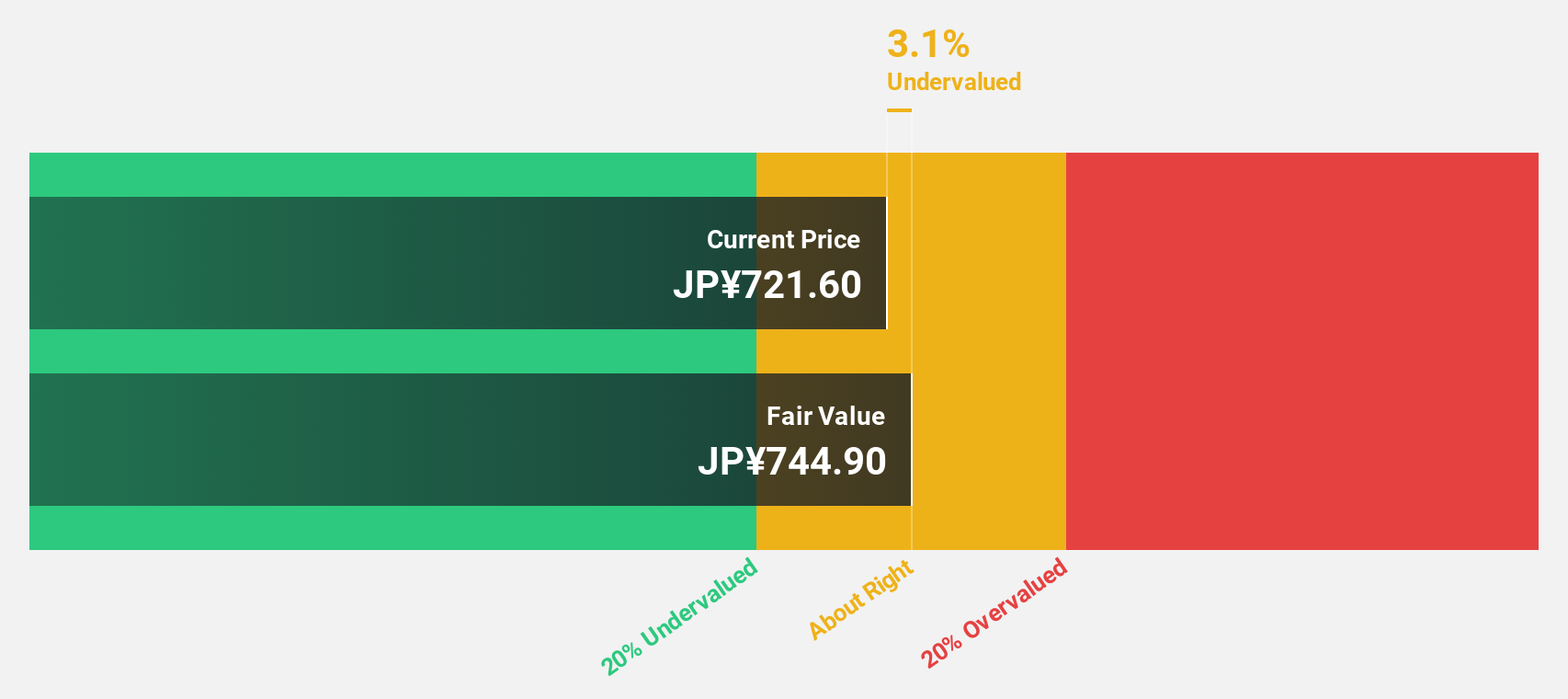

Nihon M&A Center Holdings (TSE:2127)

Overview: Nihon M&A Center Holdings Inc. offers mergers and acquisitions services both in Japan and internationally, with a market cap of approximately ¥201.50 billion.

Operations: The company generates revenue from its M&A Consulting Business, amounting to ¥43.56 billion.

Estimated Discount To Fair Value: 19.7%

Nihon M&A Center Holdings, trading at ¥649.4, is undervalued with a fair value estimate of ¥808.99. Earnings are projected to grow 9% annually, outpacing the Japanese market's 7.8%. Revenue growth is expected at 9.3%, also above the market average of 4.1%. The company offers a reliable dividend yield and recently increased its quarterly dividend from ¥11 to ¥14 per share, reflecting solid cash flow management and potential for future returns.

- Our earnings growth report unveils the potential for significant increases in Nihon M&A Center Holdings' future results.

- Unlock comprehensive insights into our analysis of Nihon M&A Center Holdings stock in this financial health report.

Taking Advantage

- Dive into all 886 of the Undervalued Stocks Based On Cash Flows we have identified here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:LSS

Lectra

Provides industrial intelligence solutions for fashion, automotive, and furniture markets in Northern Europe, Southern Europe, the Americas, and the Asia Pacific.

Reasonable growth potential and fair value.