- Japan

- /

- Hospitality

- /

- TSE:9616

Kyoritsu Maintenance Co., Ltd.'s (TSE:9616) Stock Retreats 25% But Earnings Haven't Escaped The Attention Of Investors

To the annoyance of some shareholders, Kyoritsu Maintenance Co., Ltd. (TSE:9616) shares are down a considerable 25% in the last month, which continues a horrid run for the company. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 23% share price drop.

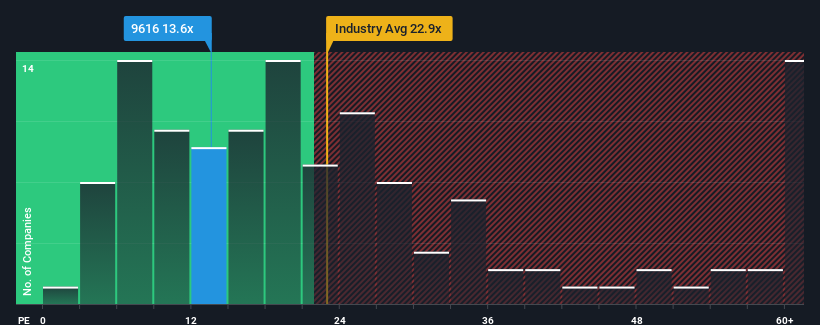

Although its price has dipped substantially, there still wouldn't be many who think Kyoritsu Maintenance's price-to-earnings (or "P/E") ratio of 13.6x is worth a mention when the median P/E in Japan is similar at about 13x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

With earnings growth that's superior to most other companies of late, Kyoritsu Maintenance has been doing relatively well. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

See our latest analysis for Kyoritsu Maintenance

What Are Growth Metrics Telling Us About The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Kyoritsu Maintenance's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 193%. Although, its longer-term performance hasn't been as strong with three-year EPS growth being relatively non-existent overall. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 10.0% per year during the coming three years according to the seven analysts following the company. That's shaping up to be similar to the 9.6% each year growth forecast for the broader market.

In light of this, it's understandable that Kyoritsu Maintenance's P/E sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

What We Can Learn From Kyoritsu Maintenance's P/E?

Kyoritsu Maintenance's plummeting stock price has brought its P/E right back to the rest of the market. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Kyoritsu Maintenance maintains its moderate P/E off the back of its forecast growth being in line with the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings won't throw up any surprises. Unless these conditions change, they will continue to support the share price at these levels.

Plus, you should also learn about these 2 warning signs we've spotted with Kyoritsu Maintenance (including 1 which is a bit concerning).

If you're unsure about the strength of Kyoritsu Maintenance's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Kyoritsu Maintenance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9616

Solid track record and fair value.

Market Insights

Community Narratives