- Japan

- /

- Medical Equipment

- /

- TSE:7741

Global Market Highlights 3 Stocks Possibly Trading Below Estimated Value

Reviewed by Simply Wall St

In recent weeks, global markets have experienced a mix of volatility and cautious optimism, with U.S. consumer confidence dropping significantly and ongoing concerns about inflation and trade policies impacting investor sentiment. Amid these fluctuations, identifying stocks that may be trading below their estimated value can offer potential opportunities for investors seeking to navigate the current economic landscape. A good stock in such conditions often exhibits strong fundamentals or growth potential that might not yet be fully recognized by the market, providing an opportunity for future appreciation as broader economic uncertainties persist.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Chifeng Jilong Gold MiningLtd (SHSE:600988) | CN¥18.16 | CN¥36.02 | 49.6% |

| Hyosung Heavy Industries (KOSE:A298040) | ₩432500.00 | ₩855375.21 | 49.4% |

| CD Projekt (WSE:CDR) | PLN221.60 | PLN441.21 | 49.8% |

| Tinexta (BIT:TNXT) | €7.77 | €15.40 | 49.6% |

| Vestas Wind Systems (CPSE:VWS) | DKK101.40 | DKK202.76 | 50% |

| LITALICO (TSE:7366) | ¥1088.00 | ¥2154.23 | 49.5% |

| Vinte Viviendas Integrales. de (BMV:VINTE *) | MX$32.50 | MX$65.00 | 50% |

| Canatu Oyj (HLSE:CANATU) | €12.50 | €24.76 | 49.5% |

| Surgical Science Sweden (OM:SUS) | SEK157.50 | SEK310.93 | 49.3% |

| Nexstim (HLSE:NXTMH) | €8.48 | €16.75 | 49.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

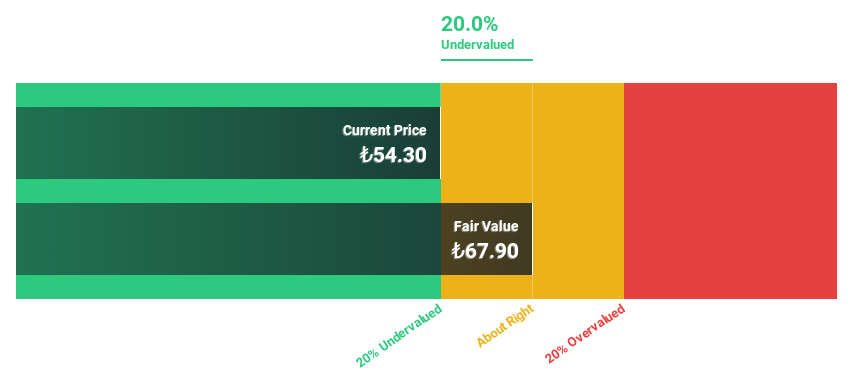

Torunlar Gayrimenkul Yatirim Ortakligi (IBSE:TRGYO)

Overview: Torunlar Gayrimenkul Yatirim Ortakligi Anonim Sirketi, known as Torunlar REIC, is a real estate investment company with a market capitalization of TRY53.43 billion, focusing on the development and management of commercial and residential properties.

Operations: Torunlar REIC generates its revenue primarily through the development and management of commercial and residential properties.

Estimated Discount To Fair Value: 20.8%

Torunlar Gayrimenkul Yatirim Ortakligi is trading at TRY53.75, below its estimated fair value of TRY67.87, reflecting a discount of over 20%. Despite lower profit margins than last year and a dividend yield of 4.37% not fully covered by earnings or free cash flows, the company shows strong growth potential with earnings expected to grow significantly at 113.48% annually, outpacing both revenue and market averages in Turkey.

- Our comprehensive growth report raises the possibility that Torunlar Gayrimenkul Yatirim Ortakligi is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of Torunlar Gayrimenkul Yatirim Ortakligi.

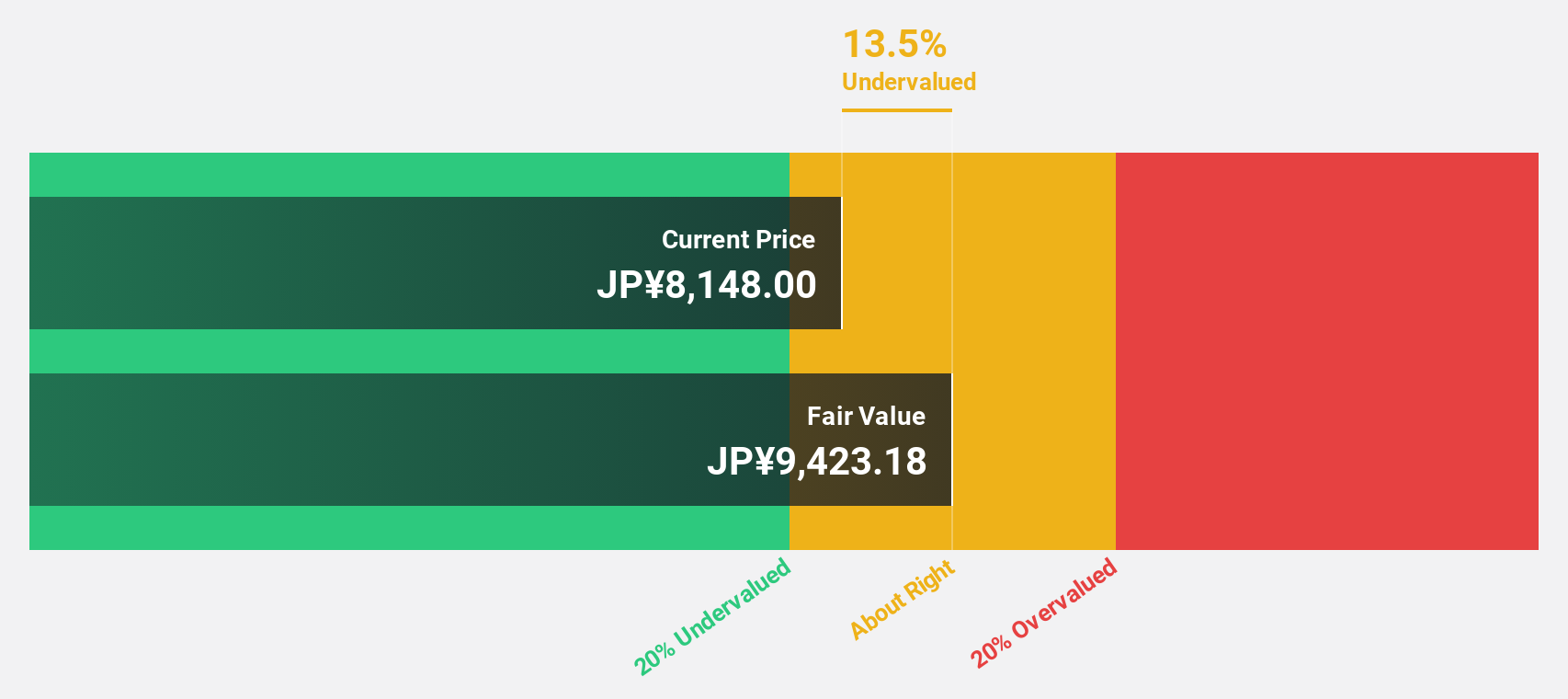

Zensho Holdings (TSE:7550)

Overview: Zensho Holdings Co., Ltd. operates food service chain restaurants both in Japan and internationally, with a market cap of ¥1.19 trillion.

Operations: The company's revenue segments include Restaurants at ¥152.62 billion, Global Sukiya at ¥288.67 billion, Global Fast Food at ¥309.49 billion, Global Hamasushi at ¥234.23 billion, Retail at ¥77.59 billion, and Corporate and Support services contributing ¥398.06 billion.

Estimated Discount To Fair Value: 34.7%

Zensho Holdings, trading at ¥7992, is undervalued with a fair value estimate of ¥12239.37, offering a potential upside of over 20%. Despite high debt levels and slower revenue growth forecasts of 6.9% per year compared to the market's 4.2%, its earnings are projected to grow robustly at 18.1% annually. Recent fixed-income offerings include unsecured bonds with a fixed coupon rate of 1.349%, indicating strategic financial maneuvers amidst strong profit growth prospects.

- The analysis detailed in our Zensho Holdings growth report hints at robust future financial performance.

- Click to explore a detailed breakdown of our findings in Zensho Holdings' balance sheet health report.

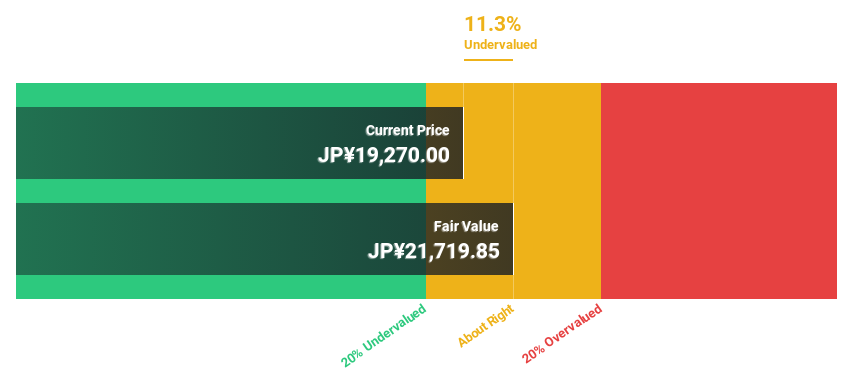

HOYA (TSE:7741)

Overview: HOYA Corporation is a med-tech company that offers high-tech and medical products globally, with a market cap of ¥6.04 trillion.

Operations: The company's revenue is derived from its high-tech and medical product segments, contributing significantly to its global operations.

Estimated Discount To Fair Value: 11.7%

HOYA Corporation is trading at ¥18,035, below its fair value estimate of ¥20,428.41. Analysts anticipate a 28.2% stock price increase as earnings are projected to grow annually by 11.2%, outpacing the JP market's 8%. Revenue growth is also expected at 7.7% per year. A recent share buyback program aims to enhance shareholder returns and capital efficiency, reflecting strategic financial management amidst moderate undervaluation based on cash flows.

- Upon reviewing our latest growth report, HOYA's projected financial performance appears quite optimistic.

- Unlock comprehensive insights into our analysis of HOYA stock in this financial health report.

Make It Happen

- Click this link to deep-dive into the 510 companies within our Undervalued Global Stocks Based On Cash Flows screener.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HOYA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7741

HOYA

A med-tech company, provides high-tech and medical products worldwide.

Outstanding track record with excellent balance sheet.

Market Insights

Community Narratives