Advertisement

Amid recent declines in Japan's stock markets, with the Nikkei 225 and TOPIX Index both experiencing losses due to election uncertainties and inflationary pressures, investors are increasingly looking towards small-cap opportunities that might offer resilience in a fluctuating market. As we explore these undiscovered gems, it is crucial to consider companies with robust fundamentals and potential for growth despite broader economic challenges.

Top 10 Undiscovered Gems With Strong Fundamentals In Japan

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Tokyo Tekko | 10.81% | 7.30% | 7.30% | ★★★★★★ |

| Central Forest Group | NA | 7.05% | 14.29% | ★★★★★★ |

| Nippon Denko | 18.00% | 4.31% | 48.41% | ★★★★★★ |

| Ad-Sol Nissin | NA | 4.02% | 7.90% | ★★★★★★ |

| Otec | 9.81% | 2.32% | -1.39% | ★★★★★★ |

| HeadwatersLtd | NA | 19.26% | 23.89% | ★★★★★★ |

| Kappa Create | 74.42% | -0.45% | 3.62% | ★★★★★☆ |

| Yukiguni Maitake | 170.63% | -6.51% | -39.66% | ★★★★☆☆ |

| Nippon Sharyo | 61.34% | -1.68% | -17.07% | ★★★★☆☆ |

| Hakuto | 56.93% | 8.02% | 27.72% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

DyDo Group Holdings (TSE:2590)

Simply Wall St Value Rating: ★★★★★☆

Overview: DyDo Group Holdings, Inc. is a company engaged in the production and distribution of beverages across Japan, Turkey, Malaysia, Russia, and China with a market capitalization of approximately ¥95.68 billion.

Operations: DyDo Group Holdings generates revenue primarily from its Domestic Beverages segment, contributing ¥152.38 billion, and the Overseas Beverage Business, which adds ¥42.74 billion. The Food Business and Pharmaceutical Business segments also contribute ¥20.96 billion and ¥13.45 billion, respectively.

DyDo Group Holdings, a notable player in Japan's beverage industry, experienced an impressive 158% earnings growth last year, outpacing the broader food sector's 26%. Despite a debt-to-equity ratio increase from 34.4% to 35.8% over five years, the company has more cash than total debt, ensuring financial stability. A ¥5.1 billion one-off gain impacted recent results significantly. However, future earnings are expected to decrease by an average of 23.5% annually over the next three years. Recent sales volumes hovered around 92-93%, and dividends were halved to ¥15 per share compared to last year’s payout.

- Delve into the full analysis health report here for a deeper understanding of DyDo Group Holdings.

Explore historical data to track DyDo Group Holdings' performance over time in our Past section.

Kanadevia (TSE:7004)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kanadevia Corporation designs, constructs, and manufactures energy-from-waste plants, desalination plants, and water and sewage treatment plants both in Japan and internationally with a market cap of ¥174.92 billion.

Operations: The primary revenue streams for Kanadevia include the Environment segment, generating ¥423.39 billion, and the Carbon Neutral Solution segment, contributing ¥62.65 billion. Additionally, the Machinery & Infrastructure segment accounts for ¥88.71 billion in revenue.

Kanadevia, a promising player in Japan's market, has shown significant improvement with its debt to equity ratio dropping from 82.2% to 46.3% over five years. The company's earnings growth of 15% last year outpaced the Machinery industry average of 12.3%, indicating strong performance relative to peers. Recent corporate guidance suggests an optimistic outlook, with net sales expected at ¥570 billion and profit attributable to shareholders projected at ¥18 billion for the fiscal year ending March 2025. Despite not being free cash flow positive, Kanadevia trades at a notable discount of around 52.9% below estimated fair value, suggesting potential undervaluation in the market.

- Click here and access our complete health analysis report to understand the dynamics of Kanadevia.

Examine Kanadevia's past performance report to understand how it has performed in the past.

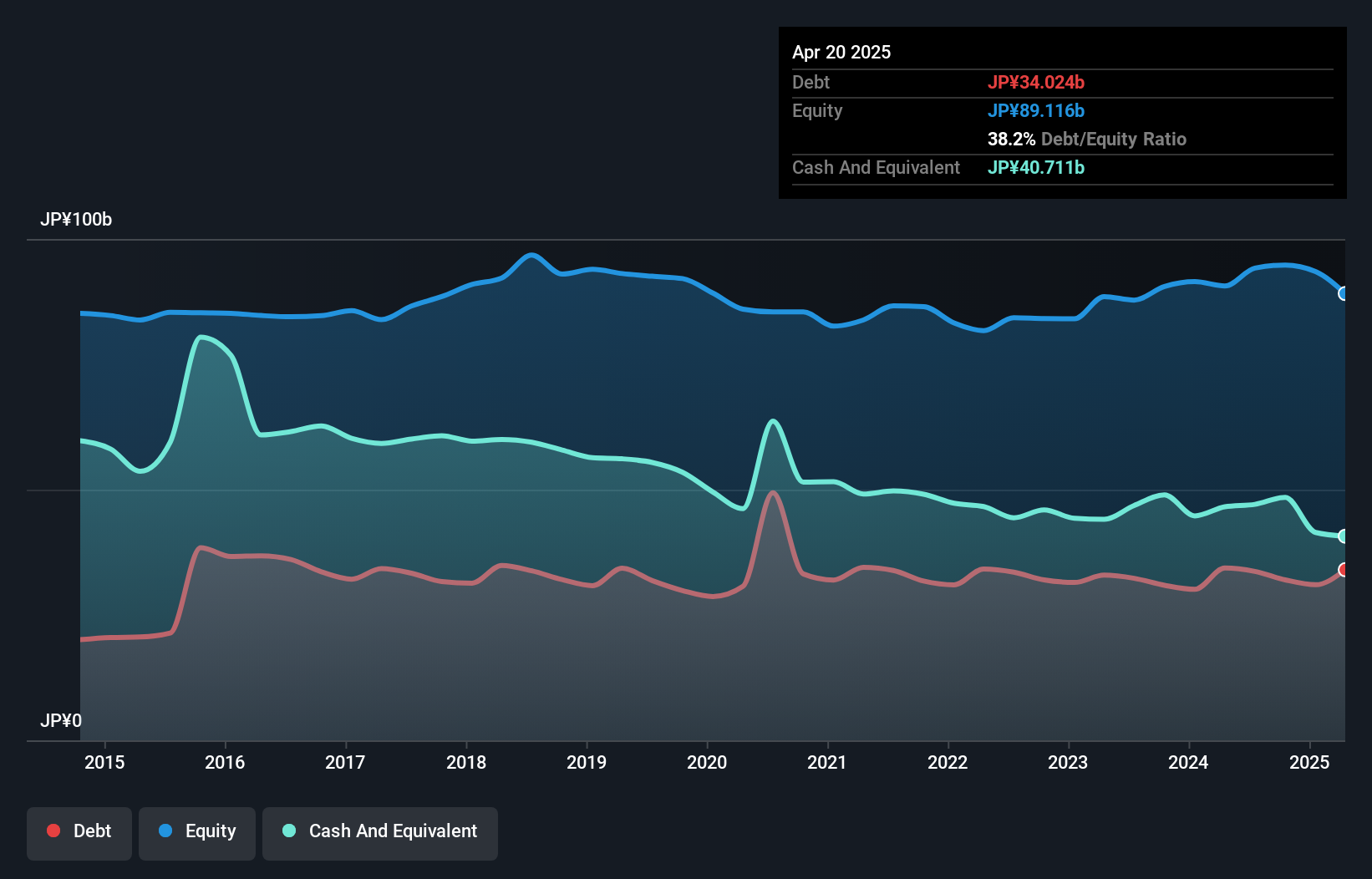

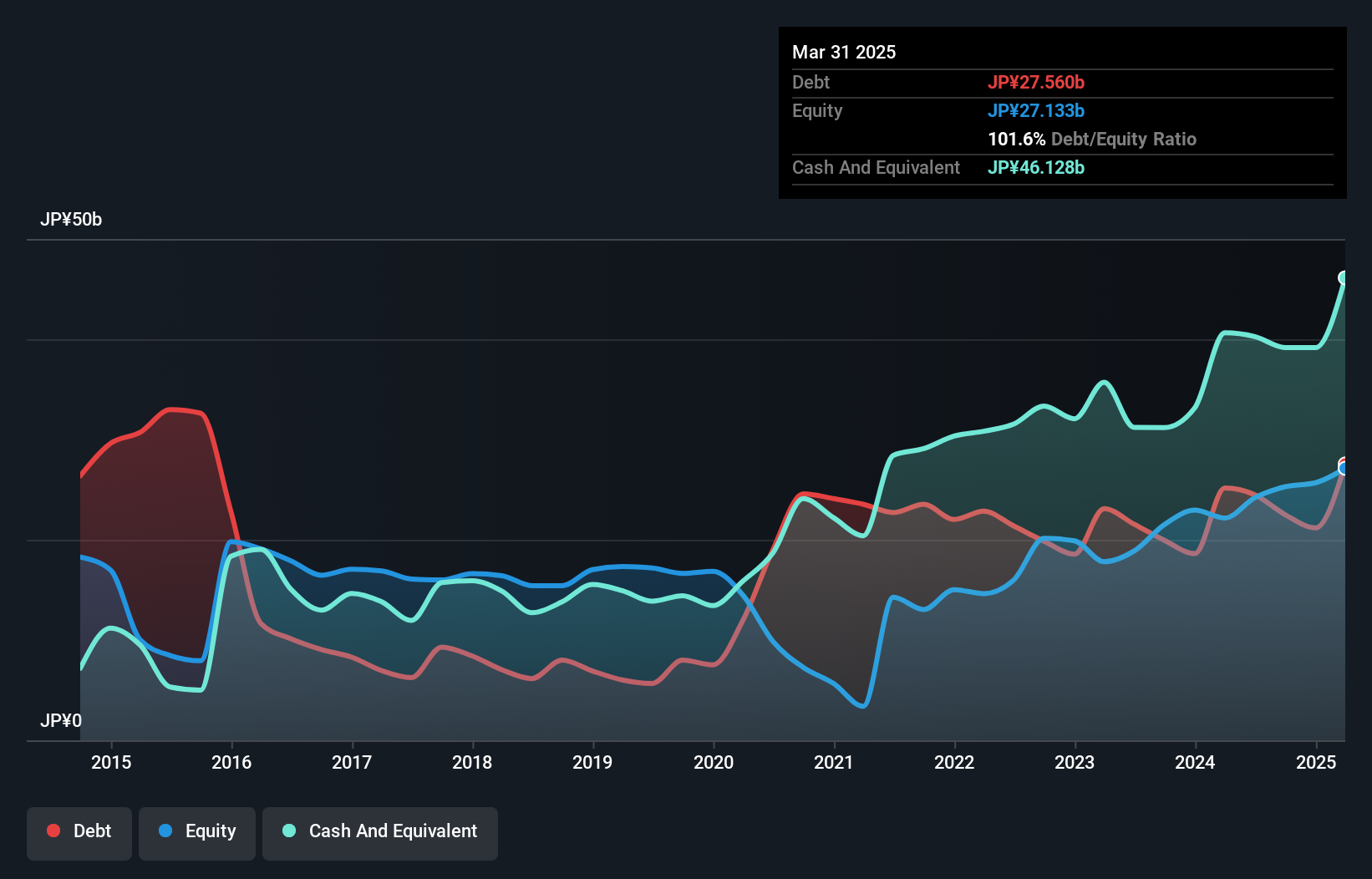

Watami (TSE:7522)

Simply Wall St Value Rating: ★★★★★☆

Overview: Watami Co., Ltd. operates in the food, home food, and agriculture services sectors both in Japan and internationally, with a market cap of ¥38.47 billion.

Operations: Watami Co., Ltd. generates revenue through its diverse operations in the food, home food, and agriculture services sectors across Japan and internationally. The company's financial performance is reflected by its market capitalization of ¥38.47 billion.

Watami, a noteworthy player in Japan's hospitality sector, has seen its earnings surge by 41% over the past year, outpacing the industry average of 28.3%. Despite this impressive growth, a significant one-off loss of ¥1.6 billion has impacted its recent financial results as of June 2024. The company's debt-to-equity ratio has notably risen from 33% to 101.2% over five years; however, it still holds more cash than total debt and covers interest payments comfortably. Trading at nearly 19% below estimated fair value suggests potential for investors seeking undervalued opportunities in Japan’s dynamic market landscape.

- Dive into the specifics of Watami here with our thorough health report.

Evaluate Watami's historical performance by accessing our past performance report.

Taking Advantage

- Discover the full array of 718 Japanese Undiscovered Gems With Strong Fundamentals right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kanadevia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7004

Kanadevia

Kanadevia Corporation design, constructs, and manufactures energy-from-waste plants, desalination plants, and water and sewage treatment plants in Japan and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor