- Japan

- /

- Hospitality

- /

- TSE:7522

None And 2 Other Promising Small Caps Backed By Strong Fundamentals

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by accelerating inflation and fluctuating interest rate expectations, small-cap stocks have recently lagged behind their larger counterparts, with the Russell 2000 Index trailing the S&P 500. However, this environment can often present unique opportunities for discerning investors seeking companies with strong fundamentals that may be overlooked in broader market movements. Identifying promising small caps involves focusing on solid financial health and growth potential, attributes that can help these companies thrive despite macroeconomic challenges.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Central Forest Group | NA | 5.93% | 20.71% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Segar Kumala Indonesia | NA | 21.81% | 18.21% | ★★★★★★ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| Societe de Limonaderies et de Boissons Rafraichissantes d'Afrique | 39.37% | 4.38% | -14.46% | ★★★★★☆ |

| Sparta | NA | -5.54% | -15.40% | ★★★★★☆ |

| Primadaya Plastisindo | 10.46% | 15.41% | 23.92% | ★★★★★☆ |

| Procimmo Group | 157.49% | 0.65% | 4.94% | ★★★★☆☆ |

| Krom Bank Indonesia | NA | 40.04% | 35.44% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

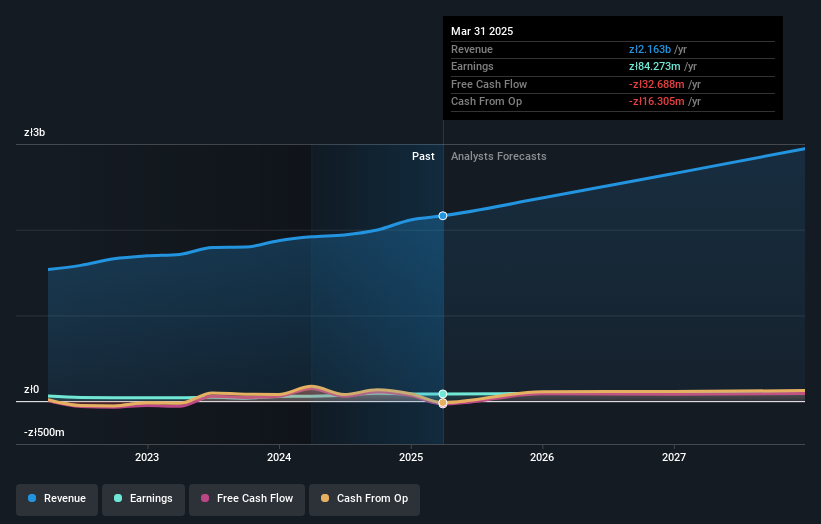

AGTech Holdings (SEHK:8279)

Simply Wall St Value Rating: ★★★★★★

Overview: AGTech Holdings Limited is an integrated technology and services company operating in the People’s Republic of China and Macau, with a market capitalization of approximately HK$2.56 billion.

Operations: AGTech Holdings generates revenue primarily from its Lottery Operation, which contributed HK$261.14 million, and Electronic Payment and Related Services, which brought in HK$338.92 million.

AGTech Holdings, a small player in the market, has shown a strong performance with earnings growth of 69.9% over the past year, outpacing the diversified financial industry. The company boasts a debt-free status, improving from a debt-to-equity ratio of 7.3% five years ago. Despite not being free cash flow positive recently, AGTech's high level of non-cash earnings and improved net income to HK$1.97 million from a previous loss highlight its resilience. Recent board changes and shareholder meetings suggest active management engagement in strategic decisions that could shape future directions for this promising entity.

- Click here to discover the nuances of AGTech Holdings with our detailed analytical health report.

Understand AGTech Holdings' track record by examining our Past report.

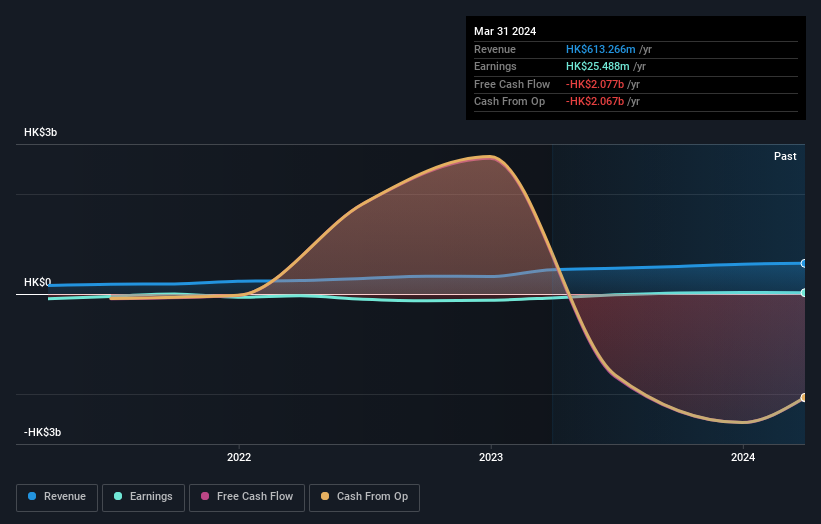

Watami (TSE:7522)

Simply Wall St Value Rating: ★★★★★☆

Overview: Watami Co., Ltd. operates in the food, home food, and agriculture services sectors both in Japan and internationally, with a market cap of ¥41.79 billion.

Operations: Watami generates revenue from its food, home food, and agriculture services across Japan and internationally. The company's financial performance is influenced by various factors within these sectors.

Watami, a smaller player in the hospitality sector, shows promising signs despite some challenges. Its earnings growth of 43% over the past year outpaced the industry average of 24%, indicating robust performance. However, a ¥1.3B one-off loss has impacted recent financial results, highlighting potential volatility in earnings quality. The company's debt to equity ratio increased from 45% to 83% over five years, yet it holds more cash than total debt, suggesting manageable leverage levels. Trading at about 12% below estimated fair value presents an attractive opportunity for investors seeking undervalued stocks with growth potential.

- Take a closer look at Watami's potential here in our health report.

Review our historical performance report to gain insights into Watami's's past performance.

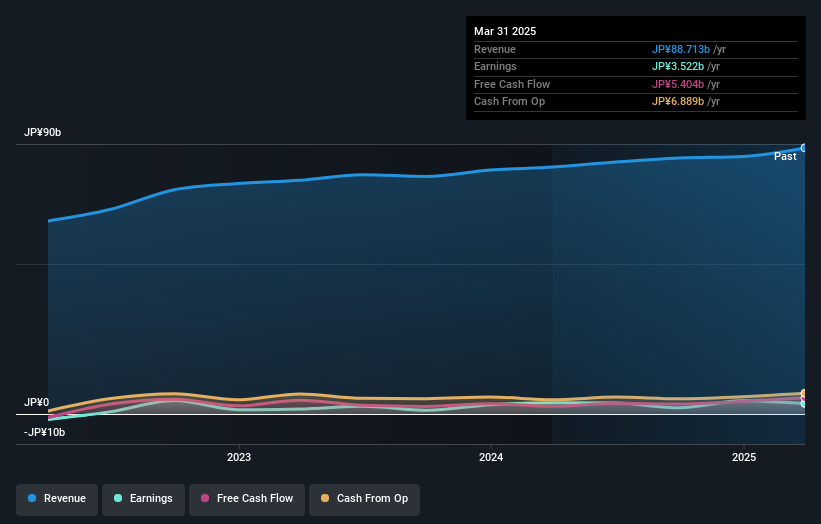

Oponeo.pl (WSE:OPN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Oponeo.pl S.A. operates as an online retailer specializing in tires and wheels for motor vehicles, serving both the Polish and international markets, with a market capitalization of PLN1.05 billion.

Operations: Revenue primarily stems from car accessories and tools, contributing PLN 1.69 billion and PLN 91.02 million respectively, with bicycles and bicycle accessories adding PLN 271.55 million. The company recorded a segment adjustment of -PLN 53.98 million in its financials.

Oponeo.pl, a small player in the specialty retail sector, has shown impressive earnings growth of 166% over the past year, outpacing its industry peers. Trading at a value 10.8% below fair estimates suggests potential for appreciation. Despite a high net debt to equity ratio of 49.7%, interest payments are well covered by EBIT at 17 times coverage, indicating strong operational efficiency. The company boasts high-quality earnings and remains free cash flow positive, which could be appealing for investors seeking robust financial health amid market volatility in this segment.

- Unlock comprehensive insights into our analysis of Oponeo.pl stock in this health report.

Gain insights into Oponeo.pl's past trends and performance with our Past report.

Next Steps

- Get an in-depth perspective on all 4725 Undiscovered Gems With Strong Fundamentals by using our screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Watami might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7522

Watami

Engages in the food, home food, and agriculture services business in Japan and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives