Metaplanet (TSE:3350) has recently seen meaningful shifts in its stock performance, with shares sliding nearly 12% over the past week. Investors are keeping an eye on its movement, especially considering last month’s 7% drop.

Zooming out to the bigger picture, Metaplanet has experienced some eye-catching momentum swings. While the recent 7% weekly drop and volatile moves may have some investors cautious, it is worth noting the stock remains up nearly 54% year-to-date by share price. Long-term shareholders are still sitting on a staggering 476% total return over the past year. Momentum appears to be cooling off after an explosive rally; however, the long-term story hasn’t been erased by recent turbulence.

The question now is whether Metaplanet’s recent pullback signals an undervalued opportunity or if the market has already factored in all its potential growth. Could this be a smart entry point, or is future upside already priced in?

Advertisement

Price-to-Earnings of 58.8x: Is it justified?

Metaplanet is currently valued at a price-to-earnings (P/E) ratio of 58.8x, significantly higher than both its industry and peer averages. With a last close price of ¥550, this lofty multiple raises the question of whether investors are expecting too much growth compared to typical hospitality sector valuations.

The P/E ratio shows what investors are willing to pay for each yen of company earnings. For a fast-growing or transformational business, a high ratio can signal market optimism about continued rapid profit expansion. In Metaplanet's case, the premium multiple places pressure on future results to justify current expectations.

Compared to competitors, Metaplanet’s 58.8x P/E is well above the JP Hospitality industry average of 24.2x and also surpasses the peer average of 15.7x. Despite this, the ratio is still below its "fair" level of 104.6x, leaving room for upside if bold growth projections are realized. This creates a tension between premium pricing and possible value that investors are watching closely.

However, weaker revenue growth or a slowdown in net income gains could challenge current optimism and put additional pressure on Metaplanet's premium valuation.

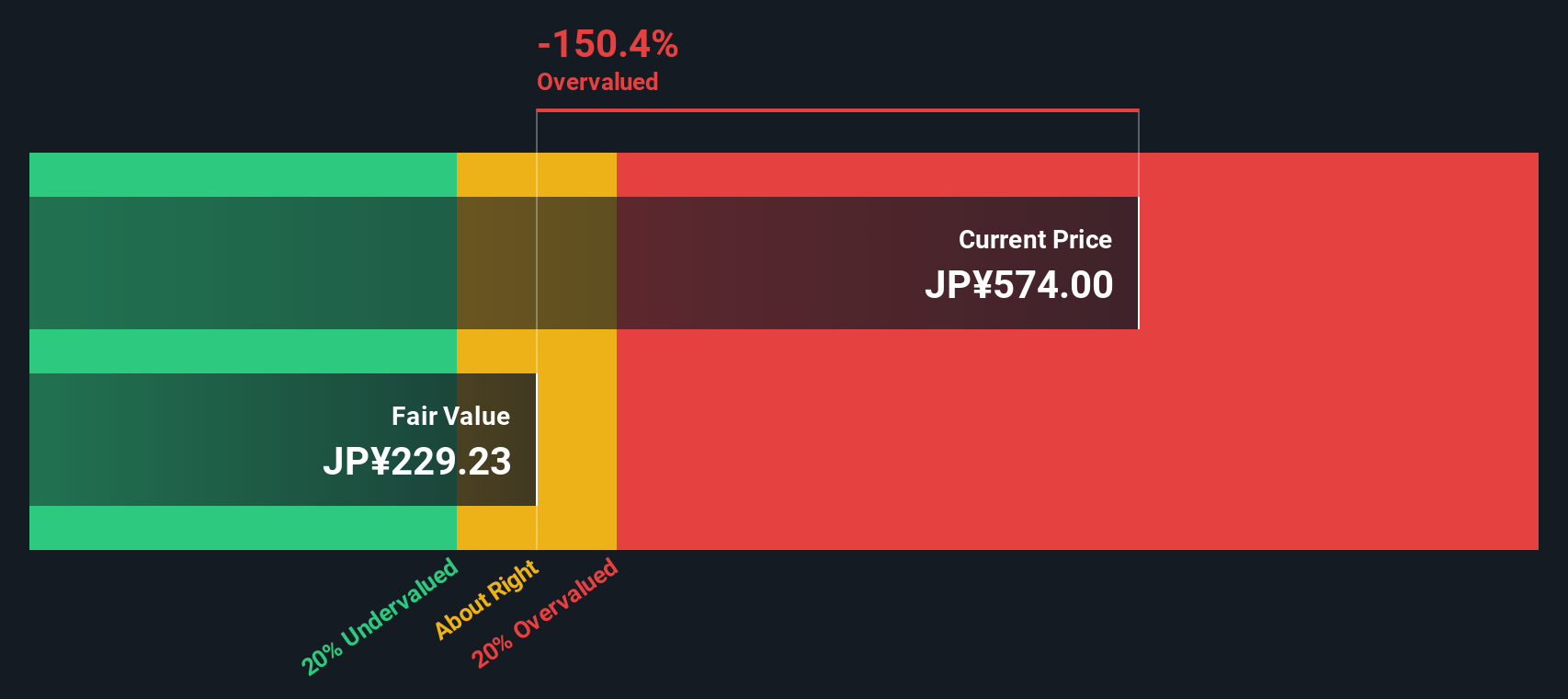

Taking a different approach, our DCF model suggests Metaplanet is trading significantly above its calculated fair value of ¥229.84. This indicates an overvalued position based on projected future cash flows. This finding stands in clear contrast to the premium justified by the current price-to-earnings ratio. Is the market betting too heavily on growth, or is the DCF being too cautious?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Metaplanet for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Metaplanet Narrative

If you prefer taking charge of your own analysis or want to challenge these findings, you can quickly pull together your own perspective in just minutes. Do it your way

Smart investors never stick to just one path. Discover high-potential opportunities and expand your portfolio with handpicked stock ideas that reflect real trends and market shifts.

Unlock future technology leaders with these 25 AI penny stocks leading the way in artificial intelligence innovation and advancement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks