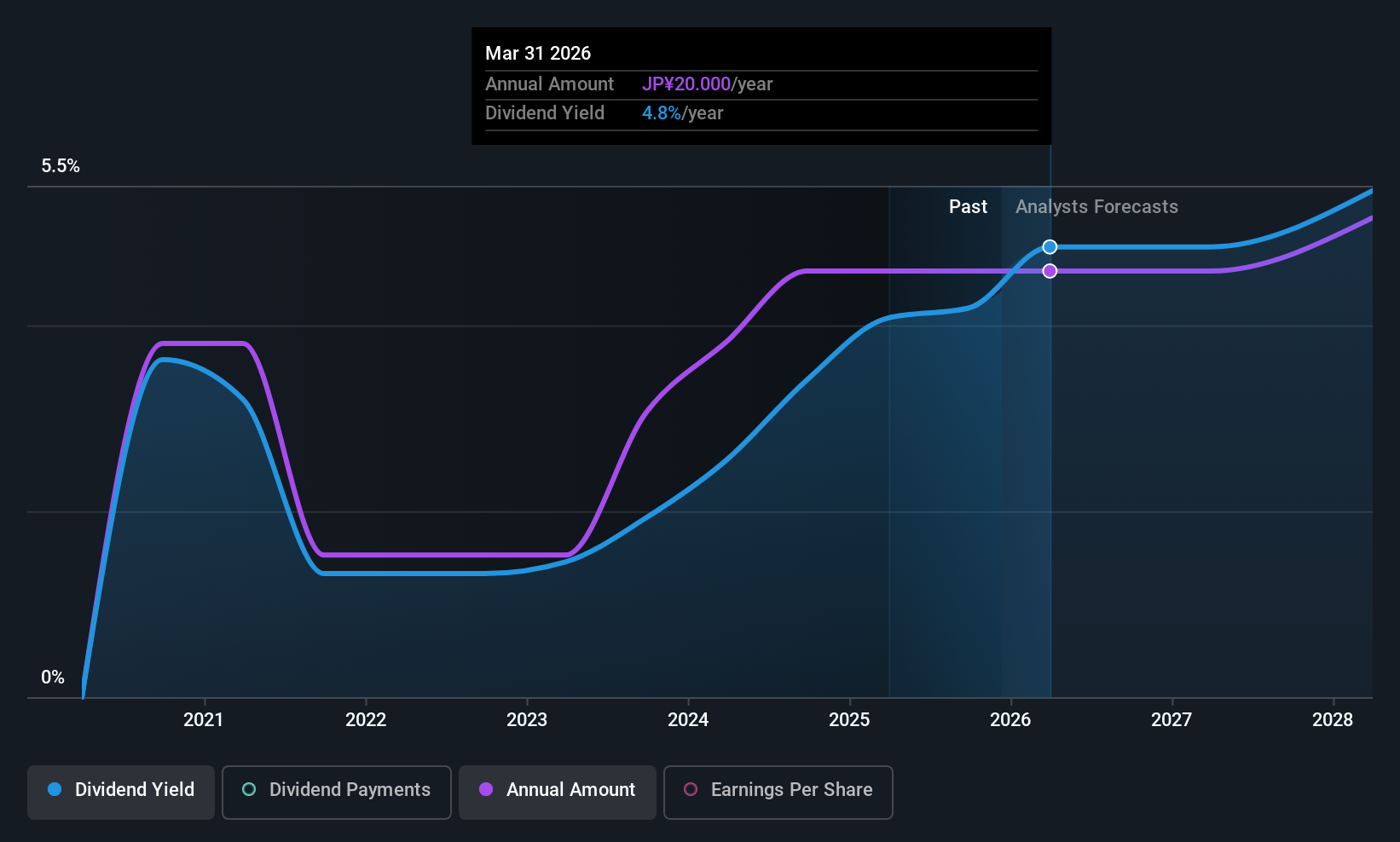

HitoMile Co., Ltd.'s (TSE:7686) investors are due to receive a payment of ¥10.00 per share on 10th of June. The dividend yield will be 4.8% based on this payment which is still above the industry average.

HitoMile's Future Dividend Projections Appear Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Before making this announcement, HitoMile was paying out quite a large proportion of both earnings and cash flow, with the dividend being 314% of cash flows. Paying out such a high proportion of cash flows can expose the business to needing to cut the dividend if the business runs into some challenges.

Over the next year, EPS is forecast to expand by 54.3%. If the dividend continues along recent trends, we estimate the payout ratio will be 67%, which would make us comfortable with the sustainability of the dividend, despite the levels currently being quite high.

Check out our latest analysis for HitoMile

HitoMile Is Still Building Its Track Record

Even though the company has been paying a consistent dividend for a while, we would like to see a few more years before we feel comfortable relying on it. The dividend has gone from an annual total of ¥16.60 in 2020 to the most recent total annual payment of ¥20.00. This means that it has been growing its distributions at 3.8% per annum over that time. HitoMile hasn't been paying a dividend for very long, so we wouldn't get to excited about its record of growth just yet.

HitoMile Might Find It Hard To Grow Its Dividend

The company's investors will be pleased to have been receiving dividend income for some time. HitoMile has seen EPS rising for the last five years, at 54% per annum. Fast growing earnings are great, but this can rarely be sustained without some reinvestment into the business, which HitoMile hasn't been doing.

The Dividend Could Prove To Be Unreliable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. While we generally think the level of distributions are a bit high, we wouldn't rule it out as becoming a good dividend payer in the future as its earnings are growing healthily. We don't think HitoMile is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 5 warning signs for HitoMile (of which 1 can't be ignored!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if HitoMile might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7686

HitoMile

Engages in wholesale business of alcoholic beverages and other foodstuffs in Japan.

High growth potential with moderate risk.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion