Advertisement

YONEX (TSE:7906): Evaluating Valuation Following Strong Share Price Performance

Simply Wall St

Reviewed by Kshitija Bhandaru

YONEX (TSE:7906) shares have seen some movement recently, catching the attention of investors curious about the company’s underlying trends. With performance shifting over the past few months, now may be a good time to take a closer look.

See our latest analysis for YONEX.

Momentum has been on YONEX’s side this year, with a share price return of over 80% year-to-date and strong total shareholder returns of 76.6% over the past twelve months. The latest 90-day move suggests buyers are still in the mix. The long-term picture is even more impressive, as five-year total returns top 598%, highlighting the company’s standout performance compared to many peers.

If you’re interested in expanding your search beyond YONEX, it’s a great moment to discover fast growing stocks with high insider ownership.

The big question for investors now is whether YONEX’s rapid rise has left more upside on the table, or if the market has already factored in all the good news and future growth into the current price.

Price-to-Earnings of 27.3x: Is it justified?

YONEX is trading at a price-to-earnings (P/E) ratio of 27.3x, which is well above both the industry average and the calculated fair ratio. With the last close at ¥3,850, this high multiple suggests the market may be pricing in robust future expectations, but there is clear divergence from typical sector levels.

The P/E ratio tells investors how much they are paying for each yen of current earnings. It is a core valuation tool for companies with positive earnings, especially in established consumer sectors like leisure and sporting goods. A high P/E can indicate strong growth prospects, but it can also mean the stock is expensive relative to its peers.

YONEX’s P/E not only exceeds the JP Leisure industry average of 14.8x, but it also stands considerably higher than the estimated fair P/E of 17.9x. The market is assigning a premium valuation, potentially factoring in the company’s rapid historical profit growth and continued momentum. If market expectations waver or growth slows, there is room for the multiple to compress toward the fair ratio level.

Explore the SWS fair ratio for YONEX

Result: Price-to-Earnings of 27.3x (OVERVALUED)

However, a nearly 10% discount to analyst price targets and compressed valuations could trigger shifts if growth slows or if sentiment weakens.

Find out about the key risks to this YONEX narrative.

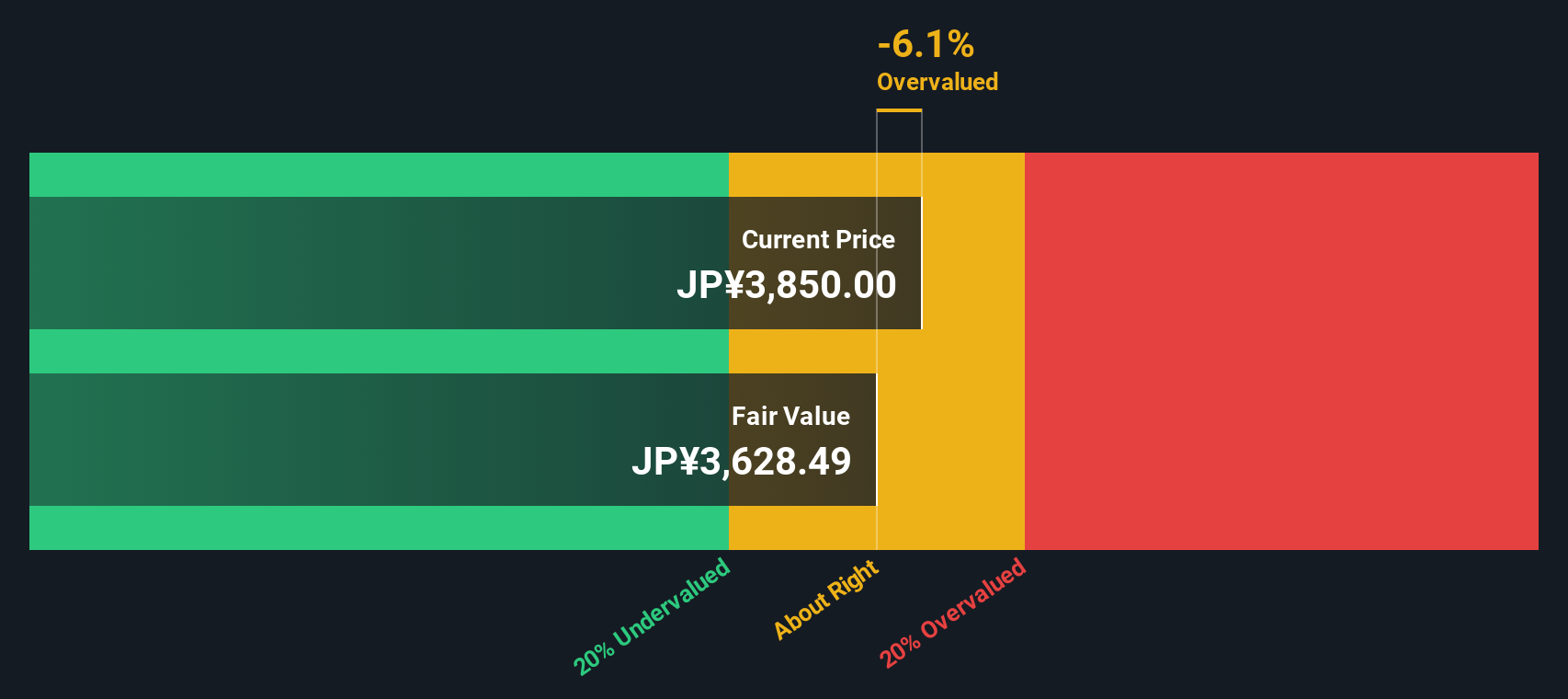

Another View: What Does the SWS DCF Model Say?

While the price-to-earnings approach flags YONEX as expensive, our DCF model offers a different perspective. According to this calculation, the company is trading above its estimated fair value, suggesting it could be overvalued by roughly 6%. Does the market see something the numbers do not or is caution warranted?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out YONEX for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own YONEX Narrative

Whether you have your own take or want to dig into the data yourself, you can easily build a personalized view of YONEX in just a few minutes. Do it your way.

A great starting point for your YONEX research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

The market never stands still, so give yourself the edge by checking out stocks with standout potential that others might overlook. Step beyond your watchlist to seize new opportunities across growing trends and untapped sectors.

- Unlock high-yield potential and steady income by checking out these 19 dividend stocks with yields > 3% with yields above 3% and proven dividend resilience.

- Get ahead of the market by spotting innovation leaders through these 24 AI penny stocks that are transforming industries with artificial intelligence breakthroughs.

- Seize value opportunities many investors miss. Find undervalued stocks using these 892 undervalued stocks based on cash flows and discover hidden gems backed by robust cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7906

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor