Advertisement

- Japan

- /

- Consumer Durables

- /

- TSE:1911

Sumitomo Forestry (TSE:1911): Evaluating Valuation After 57% Net Income Surge and Strategic North American Growth

Simply Wall St

Reviewed by Kshitija Bhandaru

Sumitomo Forestry (TSE:1911) just reported a 57% year-over-year jump in net income, highlighting improved profitability and efficient operations. The company’s strategic focus on North American growth and sustainability continues to shape its market outlook.

See our latest analysis for Sumitomo Forestry.

Sumitomo Forestry’s financial and strategic progress over the past year has not translated into headline-grabbing share price gains. With a relatively steady latest share price of ¥1,734, investors are weighing strong profit growth against a 1-year total shareholder return of just -0.18%. Recent initiatives in North America and a focus on sustainability are building long-term potential. The overall market momentum appears steady for now, with investors possibly waiting on the next earnings signal before making larger moves.

If you’re interested in uncovering other companies with rapid growth and strong insider conviction, now’s a great time to explore fast growing stocks with high insider ownership

With such strong earnings momentum and ambitious expansion plans, the question remains: is Sumitomo Forestry’s stock still undervalued, or has the market already factored in its future growth and sustainability ambitions?

Price-to-Earnings of 9.7x: Is it justified?

Sumitomo Forestry is trading at a price-to-earnings (P/E) ratio of 9.7x, which is noticeably below both the Japanese market and Consumer Durables industry averages. At the last close of ¥1,734, this valuation may signal that the stock is attractively priced versus its peers.

The P/E ratio shows what investors are willing to pay for each yen of earnings. For Sumitomo Forestry, this lower multiple could reflect investor skepticism about sustained profit growth or some conservatism given the company’s cyclical sector exposure.

Compared to the Consumer Durables industry average (11.3x) and peer companies (12.6x), Sumitomo Forestry’s P/E ratio stands out as a discount. Regression analysis also suggests a fair P/E could be as high as 20.3x, which could indicate more upside potential if the market re-rates the stock toward this level.

Explore the SWS fair ratio for Sumitomo Forestry

Result: Price-to-Earnings of 9.7x (UNDERVALUED)

However, slower revenue growth or continued lackluster total returns could undermine optimism about Sumitomo Forestry’s valuation advantage and growth prospects.

Find out about the key risks to this Sumitomo Forestry narrative.

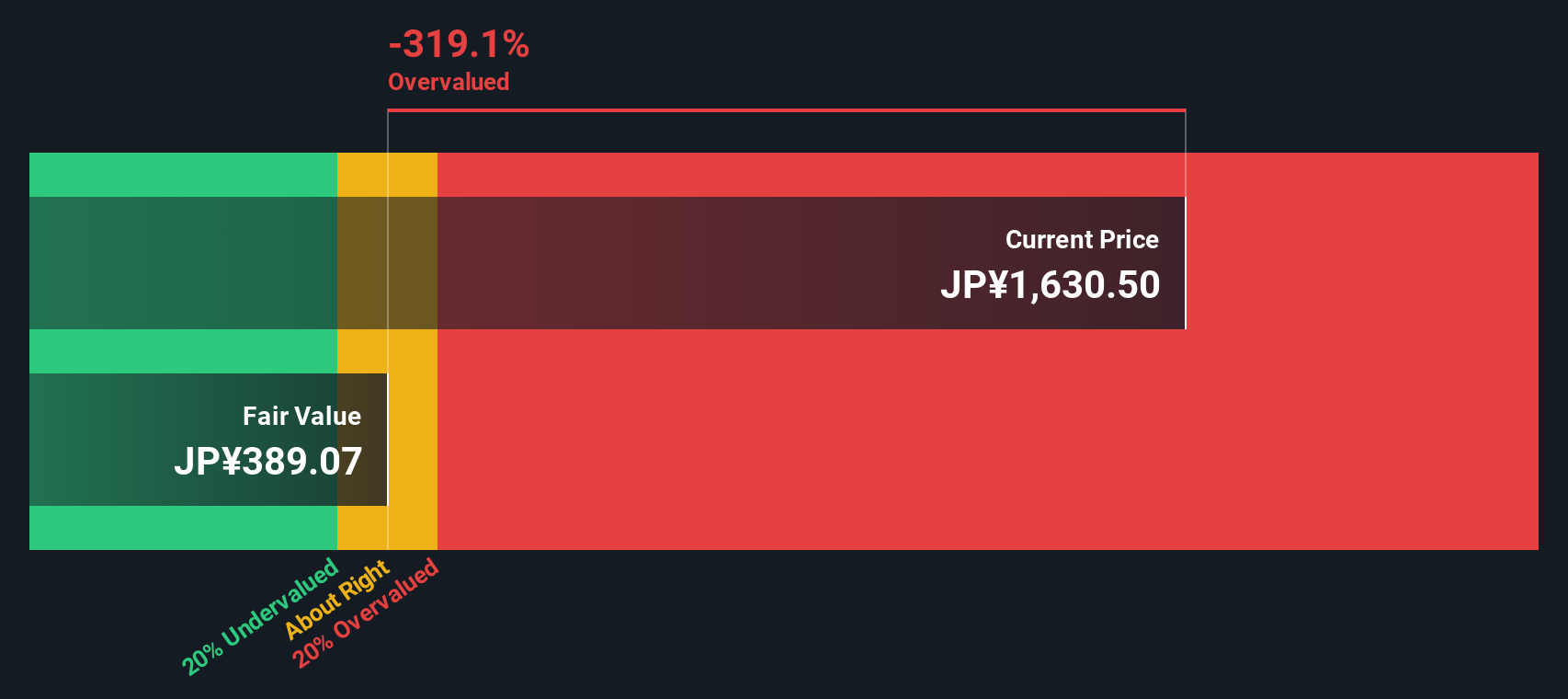

Another View: Discounted Cash Flow Model Says Overvalued

While the price-to-earnings ratio paints Sumitomo Forestry as undervalued, our SWS DCF model tells a different story. Based on this approach, the stock is trading well above its estimated fair value of ¥388.84. This challenges the optimism suggested by multiples analysis. Is the market right to ignore the DCF signal, or is risk being underestimated?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sumitomo Forestry for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sumitomo Forestry Narrative

If you have a different perspective or want to investigate the numbers for yourself, it’s easy to craft your own view in just a few minutes. Do it your way

A great starting point for your Sumitomo Forestry research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle on a single opportunity. Give yourself every advantage by checking out hand-picked stocks targeting bold growth, income, and future trends right now.

- Capture consistent income by reviewing these 19 dividend stocks with yields > 3%, which returns dividends above 3% and is handpicked for strong fundamentals and stability.

- Jump ahead of the curve with these 24 AI penny stocks, featuring companies advancing artificial intelligence in groundbreaking ways.

- Amplify your search for value with these 900 undervalued stocks based on cash flows, showing strong cash flow yet trading for less than they are truly worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1911

Sumitomo Forestry

Engages in the timber building materials, housing, overseas housing, construction, and real estate, and resources and environment businesses in Japan, the United States, Australia, China, Indonesia, New Zealand, and internationally.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor