HASEKO (TSE:1808) has been catching the eye of investors lately, and it is not just by chance. With steady developments unfolding, questions are swirling about whether the latest moves in the stock signal a shift in the company’s trajectory, or if it is simply part of the market’s usual ebb and flow. For anyone keeping an eye on Japan’s consumer durables sector, the recent attention is hard to ignore.

Looking at the numbers, HASEKO’s stock has climbed over 42% in the past year, well outpacing broad market indexes. Momentum seems to be gathering pace, with gains accelerating in recent months. These strong returns arrive as revenue and net income have both turned higher over the past year, further fueling discussions about where HASEKO is headed after a solid run.

So, after a year of notable growth, is there still value left on the table for investors, or are today’s prices already baking in all the future optimism?

Advertisement

Price-to-Earnings of 18.9x: Is it justified?

At a price-to-earnings (P/E) ratio of 18.9x, HASEKO’s shares appear expensive compared to both its peer group average and the overall industry. This suggests investors are currently paying a premium for the company’s earnings relative to sector norms.

The price-to-earnings multiple compares a company’s current share price to its per-share earnings. It is a common measure to assess whether a stock is undervalued or overvalued. In the consumer durables sector, it serves as a useful benchmark for evaluating expectations of future growth and profitability.

HASEKO’s above-average P/E ratio may indicate that the market is expecting stronger earnings ahead, or it could reflect heightened enthusiasm after recent share price gains. However, given its earnings growth outlook and recent performance, investors should weigh whether such optimism is warranted or if the valuation has outrun fundamentals.

However, risks remain, including potential slowing revenue growth or a downturn in net income. These factors could challenge the sustainability of recent gains.

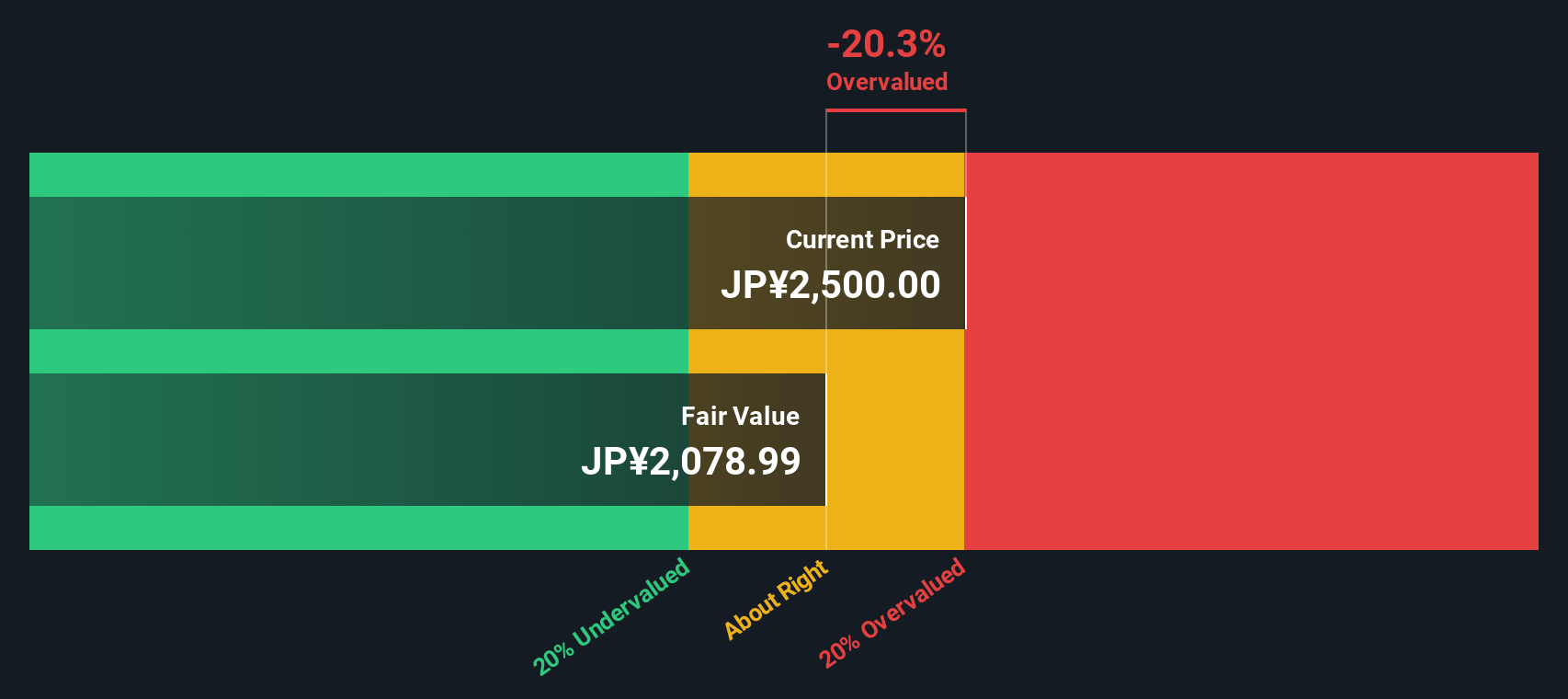

Another Perspective: What Does Our DCF Model Suggest?

While the earlier valuation method signals HASEKO could be trading on the expensive side, the SWS DCF model points in the same direction. This suggests shares may also be overvalued on a cash flow basis. Do both approaches agree for the right reasons, or is there more beneath the surface?

Unlock even more market opportunities by targeting high-potential stocks with smart screeners. Turn your next insight into action before others catch on.

Uncover tomorrow's big gainers by hunting for undervalued opportunities with our undervalued stocks based on cash flows before they appear on everyone else’s radar.

Boost your income strategy by focusing on companies offering robust payouts through dividend stocks with yields > 3% you may have overlooked.

Feed your curiosity for innovation by checking out pioneers reshaping technology with AI penny stocks in the AI space.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HASEKO might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.