Advertisement

- Japan

- /

- Commercial Services

- /

- TSE:9793

DaisekiLtd's (TSE:9793) Shareholders Will Receive A Bigger Dividend Than Last Year

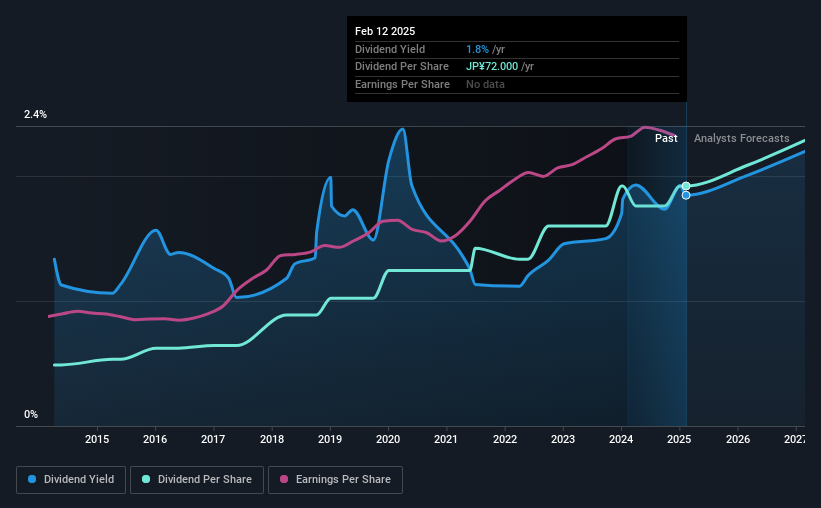

Daiseki Co.,Ltd. (TSE:9793) has announced that it will be increasing its dividend from last year's comparable payment on the 26th of May to ¥39.00. This takes the annual payment to 1.8% of the current stock price, which is about average for the industry.

See our latest analysis for DaisekiLtd

DaisekiLtd's Payment Could Potentially Have Solid Earnings Coverage

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue. However, prior to this announcement, DaisekiLtd's dividend was comfortably covered by both cash flow and earnings. This means that most of what the business earns is being used to help it grow.

Over the next year, EPS is forecast to expand by 9.9%. If the dividend continues on this path, the payout ratio could be 38% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The dividend has gone from an annual total of ¥18.33 in 2015 to the most recent total annual payment of ¥72.00. This works out to be a compound annual growth rate (CAGR) of approximately 15% a year over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

We Could See DaisekiLtd's Dividend Growing

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. We are encouraged to see that DaisekiLtd has grown earnings per share at 7.3% per year over the past five years. DaisekiLtd definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

In Summary

In summary, it's great to see that the company can raise the dividend and keep it in a sustainable range. The payout ratio looks good, but unfortunately the company's dividend track record isn't stellar. The payment isn't stellar, but it could make a decent addition to a dividend portfolio.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 1 warning sign for DaisekiLtd that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9793

DaisekiLtd

Engages industrial waste treatment and resource recycling activities in Japan.

Excellent balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor