Advertisement

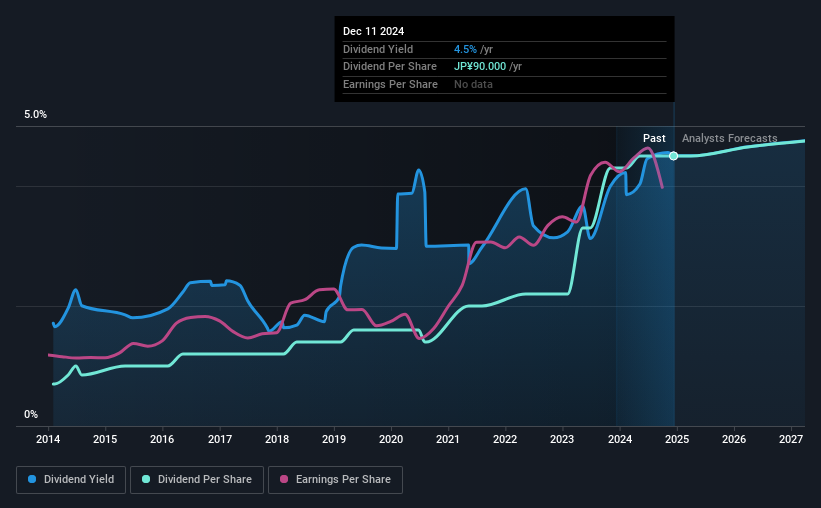

Okamura Corporation (TSE:7994) will pay a dividend of ¥45.00 on the 26th of June. This makes the dividend yield 4.5%, which is above the industry average.

See our latest analysis for Okamura

Okamura's Payment Could Potentially Have Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. Based on the last payment, Okamura's earnings were much higher than the dividend, but it wasn't converting those earnings into cash flow. No cash flows could definitely make returning cash to shareholders difficult, or at least mean the balance sheet will come under pressure.

Over the next year, EPS is forecast to expand by 6.2%. If the dividend continues on this path, the payout ratio could be 51% by next year, which we think can be pretty sustainable going forward.

Okamura Has A Solid Track Record

The company has an extended history of paying stable dividends. The dividend has gone from an annual total of ¥14.00 in 2014 to the most recent total annual payment of ¥90.00. This implies that the company grew its distributions at a yearly rate of about 20% over that duration. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Okamura has seen EPS rising for the last five years, at 19% per annum. The company is paying out a lot of its cash as a dividend, but it looks okay based on the payout ratio.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Okamura will make a great income stock. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. We don't think Okamura is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 1 warning sign for Okamura that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7994

Okamura

Manufactures, sells, distributes, and installs office furniture, store displays, material handling systems, and industrial machinery in Japan.

Very undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor