- Japan

- /

- Commercial Services

- /

- TSE:7868

KOSAIDO Holdings' (TSE:7868) Earnings Aren't As Good As They Appear

Investors were disappointed with KOSAIDO Holdings Co., Ltd.'s (TSE:7868) recent earnings release. We did some analysis and believe that they might be concerned about some weak underlying factors.

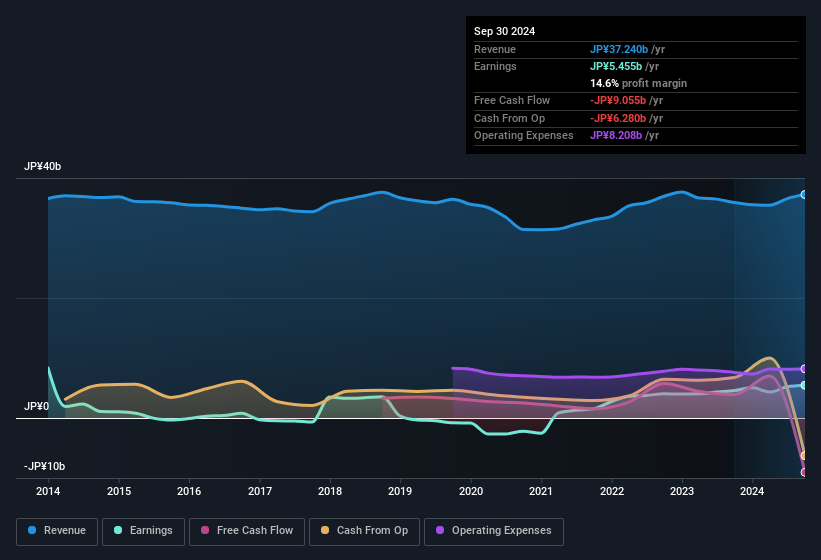

View our latest analysis for KOSAIDO Holdings

Zooming In On KOSAIDO Holdings' Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

KOSAIDO Holdings has an accrual ratio of 0.28 for the year to September 2024. Unfortunately, that means its free cash flow was a lot less than its statutory profit, which makes us doubt the utility of profit as a guide. Over the last year it actually had negative free cash flow of JP¥9.1b, in contrast to the aforementioned profit of JP¥5.46b. We saw that FCF was JP¥3.9b a year ago though, so KOSAIDO Holdings has at least been able to generate positive FCF in the past. Having said that, there is more to consider. We can look at how unusual items in the profit and loss statement impacted its accrual ratio, as well as explore how dilution is impacting shareholders negatively.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, KOSAIDO Holdings increased the number of shares on issue by 6.7% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of KOSAIDO Holdings' EPS by clicking here.

How Is Dilution Impacting KOSAIDO Holdings' Earnings Per Share (EPS)?

As you can see above, KOSAIDO Holdings has been growing its net income over the last few years, with an annualized gain of 252% over three years. But EPS was only up 210% per year, in the exact same period. And over the last 12 months, the company grew its profit by 19%. But in comparison, EPS only increased by 20% over the same period. And so, you can see quite clearly that dilution is influencing shareholder earnings.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So it will certainly be a positive for shareholders if KOSAIDO Holdings can grow EPS persistently. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

How Do Unusual Items Influence Profit?

Given the accrual ratio, it's not overly surprising that KOSAIDO Holdings' profit was boosted by unusual items worth JP¥637m in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Our Take On KOSAIDO Holdings' Profit Performance

KOSAIDO Holdings didn't back up its earnings with free cashflow, but this isn't too surprising given profits were inflated by unusual items. Meanwhile, the new shares issued mean that shareholders now own less of the company, unless they tipped in more cash themselves. Considering all this we'd argue KOSAIDO Holdings' profits probably give an overly generous impression of its sustainable level of profitability. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. Be aware that KOSAIDO Holdings is showing 4 warning signs in our investment analysis and 2 of those are a bit unpleasant...

Our examination of KOSAIDO Holdings has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if KOSAIDO Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7868

Proven track record with adequate balance sheet.