Advertisement

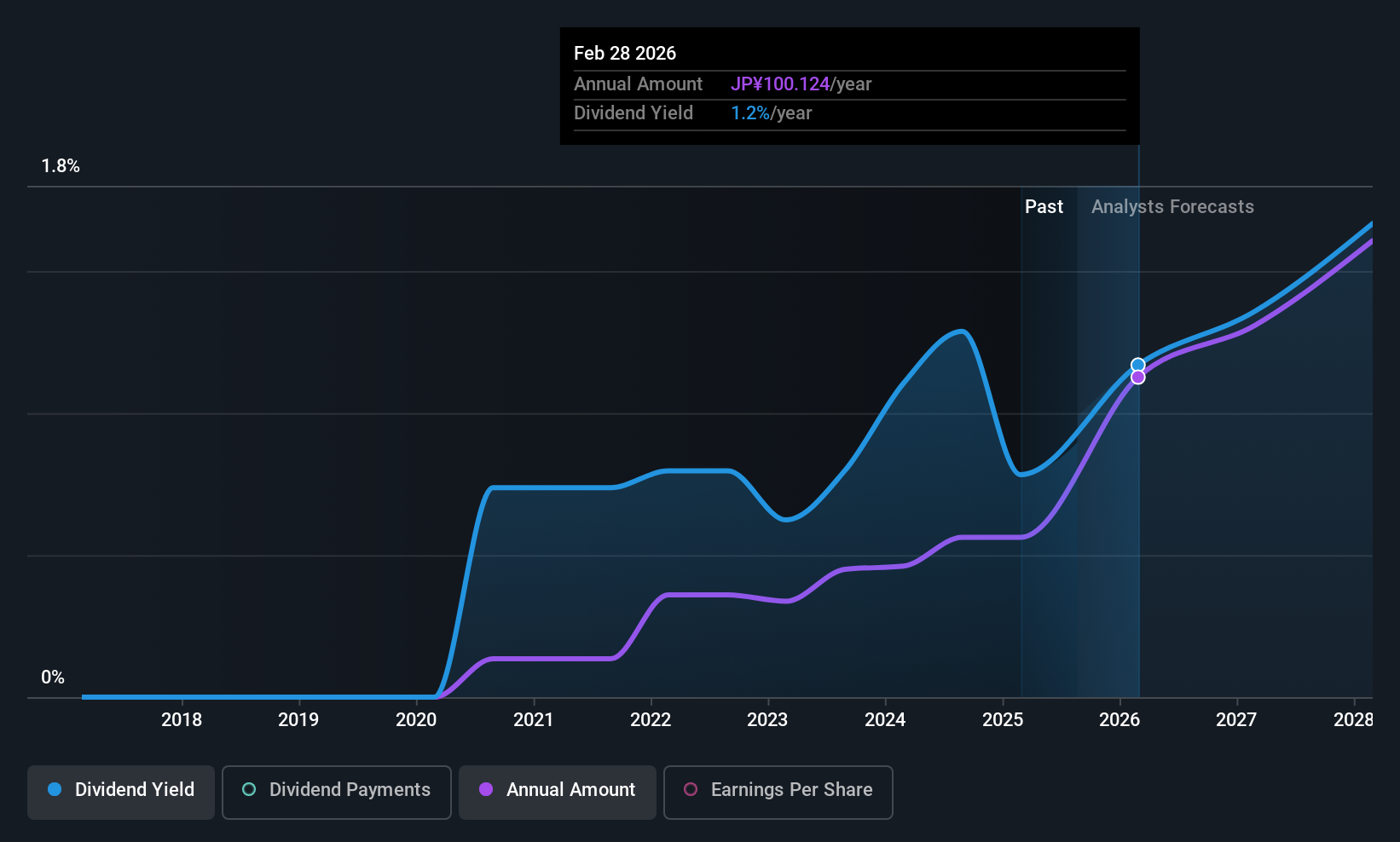

Baycurrent, Inc. (TSE:6532) has announced that it will be increasing its dividend from last year's comparable payment on the 1st of December to ¥50.00. This takes the annual payment to 1.2% of the current stock price, which is about average for the industry.

Baycurrent's Payment Could Potentially Have Solid Earnings Coverage

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. However, prior to this announcement, Baycurrent's dividend was comfortably covered by both cash flow and earnings. This means that most of what the business earns is being used to help it grow.

Looking forward, earnings per share is forecast to rise by 20.6% over the next year. If the dividend continues on this path, the payout ratio could be 40% by next year, which we think can be pretty sustainable going forward.

See our latest analysis for Baycurrent

Baycurrent Is Still Building Its Track Record

The dividend's track record has been pretty solid, but with only 5 years of history we want to see a few more years of history before making any solid conclusions. Since 2020, the dividend has gone from ¥12.00 total annually to ¥100.00. This works out to be a compound annual growth rate (CAGR) of approximately 53% a year over that time. It is always nice to see strong dividend growth, but with such a short payment history we wouldn't be inclined to rely on it until a longer track record can be developed.

We Could See Baycurrent's Dividend Growing

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that Baycurrent has been growing its earnings per share at 9.5% a year over the past three years. Baycurrent definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

In Summary

Overall, this is a reasonable dividend, and it being raised is an added bonus. While the payout ratios are a good sign, we are less enthusiastic about the company's dividend record. Taking all of this into consideration, the dividend looks viable moving forward, but investors should be mindful that the company has pushed the boundaries of sustainability in the past and may do so again.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 7 analysts we track are forecasting for Baycurrent for free with public analyst estimates for the company. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Baycurrent might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6532

Exceptional growth potential with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor