Advertisement

- Japan

- /

- Professional Services

- /

- TSE:6532

BayCurrent (TSE:6532): Exploring Valuation After Recent Share Price Gains

Simply Wall St

Reviewed by Kshitija Bhandaru

Baycurrent (TSE:6532) shares have been showing steady gains over the past month, with the stock returning about 9% during that period and more than 18% in the past three months. Investors might be taking a closer look as these trends emerge.

See our latest analysis for Baycurrent.

Baycurrent’s current momentum is hard to ignore, with notable share price returns this year and a strong 1-year total shareholder return of 70%. After several quarters of solid growth, interest appears to be building as investors look for further upside potential.

If you’re looking for more fast-moving opportunities, this is a great moment to broaden your search and discover fast growing stocks with high insider ownership

With strong recent gains and impressive growth rates, the big question now is whether Baycurrent’s stock remains undervalued, or if the market has already priced in its robust future prospects. Could further upside still be ahead?

Price-to-Earnings of 41.5x: Is it justified?

Baycurrent trades at a price-to-earnings (P/E) ratio of 41.5x, significantly above both its industry peers and the broader market average. At the last close of ¥9,058, this valuation stands out as particularly steep in comparison.

The P/E ratio measures how much investors are willing to pay today for a yen of the company’s current earnings. In growth-driven sectors like Professional Services, a higher P/E can signal strong confidence in future earnings potential, but it also raises questions about whether that optimism is already reflected in the price.

Currently, Baycurrent’s P/E is nearly double the peer group average of 22.2x and much higher than the Japanese Professional Services industry average of 15.8x. Even compared to the estimated fair P/E of 29.2x, the stock looks expensive, suggesting the market expects exceptional growth or is willing to pay a premium for the company’s track record and prospects.

Explore the SWS fair ratio for Baycurrent

Result: Price-to-Earnings of 41.5x (OVERVALUED)

However, faster-than-expected earnings slowdowns or sector-wide valuation corrections remain real risks that could impact Baycurrent’s share price trajectory.

Find out about the key risks to this Baycurrent narrative.

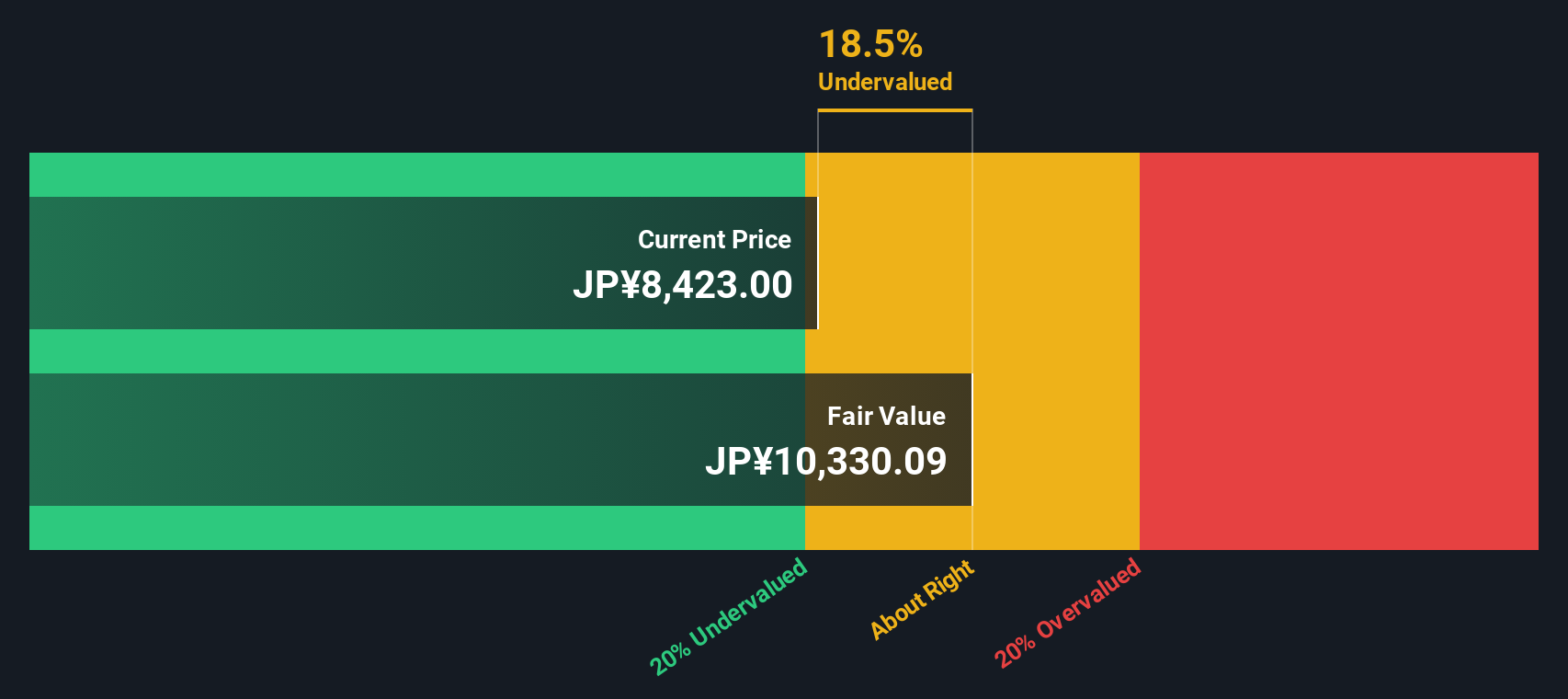

Another View: SWS DCF Model Suggests Undervaluation

While the price-to-earnings ratio paints Baycurrent as expensive, our DCF model offers a different perspective. According to the SWS DCF model, the stock trades about 12% below its estimated fair value. This suggests that despite a rich P/E, there could be untapped upside left.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Baycurrent for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Baycurrent Narrative

If you see the story differently or want to dig into the numbers yourself, you can easily put together your own perspective in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Baycurrent.

Looking for more investment ideas?

Take charge of your investing journey by acting on unique market opportunities before others do. These handpicked screens put the best stocks right at your fingertips.

- Uncover hidden value with these 886 undervalued stocks based on cash flows, which targets established companies trading below their true worth based on cash flows.

- Tap into big yield potential by reviewing these 19 dividend stocks with yields > 3%, featuring reliable picks with impressive dividend payouts greater than 3%.

- Ride the next wave of digital transformation by analyzing these 25 AI penny stocks, featuring forward-thinking firms making breakthroughs in artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baycurrent might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6532

Exceptional growth potential with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.4% undervalued

TR

Community Contributor