Advertisement

- Japan

- /

- Commercial Services

- /

- TSE:1418

Interlife Holdings Co., Ltd.'s (TSE:1418) Stock Is Going Strong: Is the Market Following Fundamentals?

Most readers would already be aware that Interlife Holdings' (TSE:1418) stock increased significantly by 40% over the past three months. Given the company's impressive performance, we decided to study its financial indicators more closely as a company's financial health over the long-term usually dictates market outcomes. Specifically, we decided to study Interlife Holdings' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Interlife Holdings is:

19% = JP¥755m ÷ JP¥4.1b (Based on the trailing twelve months to November 2024).

The 'return' refers to a company's earnings over the last year. That means that for every ¥1 worth of shareholders' equity, the company generated ¥0.19 in profit.

See our latest analysis for Interlife Holdings

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Interlife Holdings' Earnings Growth And 19% ROE

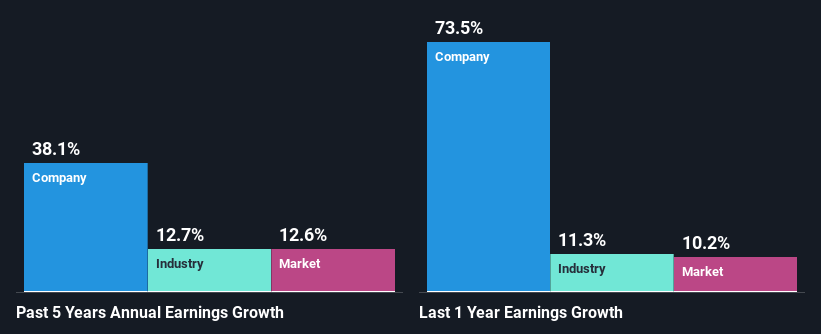

To begin with, Interlife Holdings seems to have a respectable ROE. Further, the company's ROE compares quite favorably to the industry average of 8.9%. Probably as a result of this, Interlife Holdings was able to see an impressive net income growth of 38% over the last five years. However, there could also be other causes behind this growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

Next, on comparing with the industry net income growth, we found that Interlife Holdings' growth is quite high when compared to the industry average growth of 13% in the same period, which is great to see.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Interlife Holdings is trading on a high P/E or a low P/E, relative to its industry.

Is Interlife Holdings Using Its Retained Earnings Effectively?

The three-year median payout ratio for Interlife Holdings is 32%, which is moderately low. The company is retaining the remaining 68%. So it seems that Interlife Holdings is reinvesting efficiently in a way that it sees impressive growth in its earnings (discussed above) and pays a dividend that's well covered.

Additionally, Interlife Holdings has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders.

Conclusion

In total, we are pretty happy with Interlife Holdings' performance. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Not to forget, share price outcomes are also dependent on the potential risks a company may face. So it is important for investors to be aware of the risks involved in the business. To know the 2 risks we have identified for Interlife Holdings visit our risks dashboard for free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:1418

Interlife Holdings

Provides designs, constructs, manages, and maintains commercial facilities and public facilities in Japan.

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|38.7% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|30.8% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.6% undervalued

MA

Community Contributor