Advertisement

- Japan

- /

- Trade Distributors

- /

- TSE:8031

How Investors May Respond To Mitsui (TSE:8031) Expanding Australian Iron Ore Partnership With Rio Tinto and Nippon Steel

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Rio Tinto Group announced it will partner with Mitsui & Co. and Nippon Steel to invest US$733 million in developing new iron ore mines at the West Angelas hub in Western Australia, targeting first output in 2027 and an annual production capacity of about 35 million tons.

- This collaboration highlights Mitsui’s ongoing commitment to global resource development and may affect its investment outlook and earnings composition going forward.

- Let’s examine how Mitsui’s major Australian iron ore investment with Rio Tinto and Nippon Steel could shape its future business narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Mitsui Investment Narrative Recap

To be a Mitsui shareholder, you need to believe in the company’s ability to grow earnings through large-scale investments in global resource projects, while actively managing risks from fluctuating commodity prices and energy transition trends. This week’s US$733 million West Angelas iron ore partnership showcases Mitsui’s continued push in resource development, but does not appear to materially alter the main short-term catalyst: demand and price trends in core commodities. The biggest risk remains ongoing earnings pressure from lower prices and volumes in core resource segments, which showed up in recent quarterly results.

One of Mitsui’s most relevant recent moves was its investment in the Blue Point low-carbon ammonia project in the U.S., aiming to tap into rising global demand for cleaner energy. This initiative directly relates to the company’s long-term catalyst of transitioning its portfolio toward less volatile and more sustainable energy segments, as commodity-driven earnings remain under pressure.

Yet, behind the headlines, investors should also watch for periods where the absence of significant asset sale gains...

Read the full narrative on Mitsui (it's free!)

Mitsui's projections estimate ¥15,578.0 billion in revenue and ¥878.2 billion in earnings by 2028. This scenario assumes a 3.3% annual revenue growth and a ¥62.3 billion earnings increase from the current ¥815.9 billion.

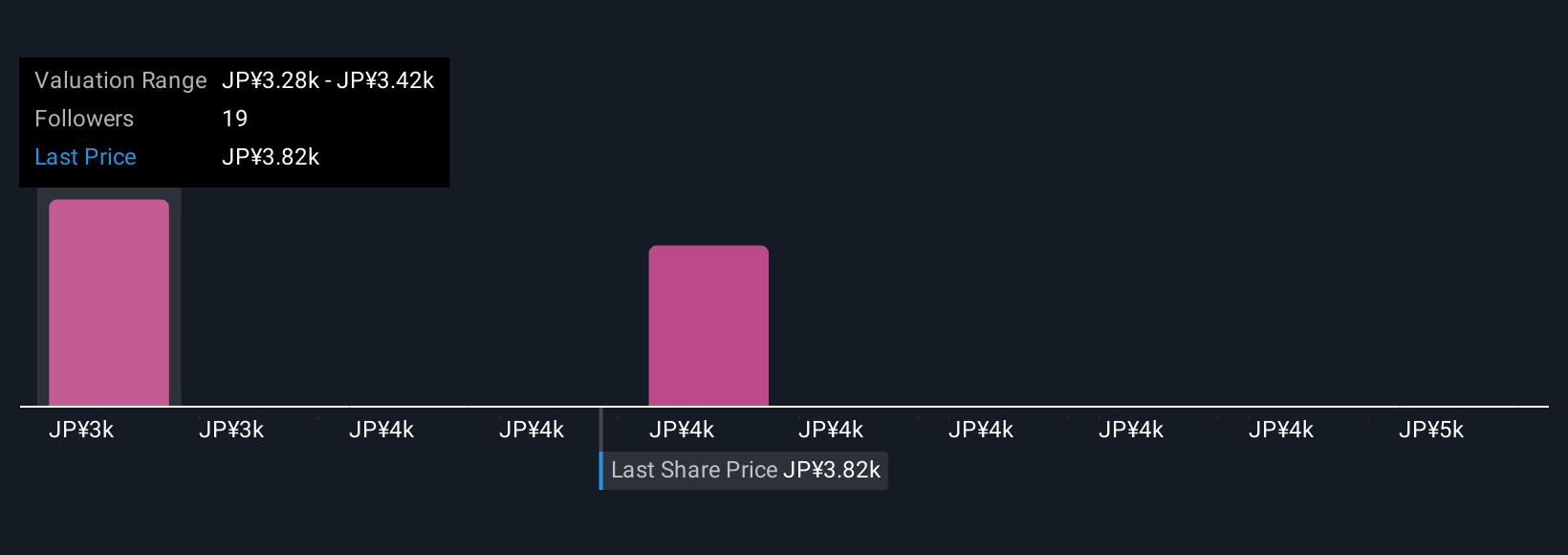

Uncover how Mitsui's forecasts yield a ¥4010 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Four different fair value estimates from the Simply Wall St Community span ¥3,274 to ¥4,700, reflecting a wide range of expectations. While you consider these varied perspectives, remember that Mitsui’s continuing exposure to commodity cycles may weigh on future profit stability.

Explore 4 other fair value estimates on Mitsui - why the stock might be worth 12% less than the current price!

Build Your Own Mitsui Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Mitsui research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Mitsui research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mitsui's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 35 companies in the world exploring or producing it. Find the list for free.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8031

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor