Advertisement

A Piece Of The Puzzle Missing From Kawasaki Heavy Industries, Ltd.'s (TSE:7012) 30% Share Price Climb

Despite an already strong run, Kawasaki Heavy Industries, Ltd. (TSE:7012) shares have been powering on, with a gain of 30% in the last thirty days. The last 30 days bring the annual gain to a very sharp 89%.

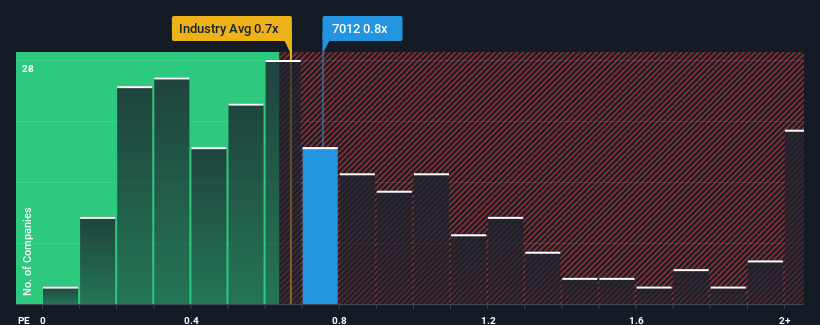

Although its price has surged higher, you could still be forgiven for feeling indifferent about Kawasaki Heavy Industries' P/S ratio of 0.8x, since the median price-to-sales (or "P/S") ratio for the Machinery industry in Japan is also close to 0.7x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Kawasaki Heavy Industries

What Does Kawasaki Heavy Industries' P/S Mean For Shareholders?

Kawasaki Heavy Industries certainly has been doing a good job lately as it's been growing revenue more than most other companies. One possibility is that the P/S ratio is moderate because investors think this strong revenue performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Keen to find out how analysts think Kawasaki Heavy Industries' future stacks up against the industry? In that case, our free report is a great place to start.Is There Some Revenue Growth Forecasted For Kawasaki Heavy Industries?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Kawasaki Heavy Industries' to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 15%. Pleasingly, revenue has also lifted 36% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 8.3% per year as estimated by the twelve analysts watching the company. That's shaping up to be materially higher than the 4.7% per annum growth forecast for the broader industry.

With this information, we find it interesting that Kawasaki Heavy Industries is trading at a fairly similar P/S compared to the industry. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Final Word

Kawasaki Heavy Industries appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Despite enticing revenue growth figures that outpace the industry, Kawasaki Heavy Industries' P/S isn't quite what we'd expect. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Kawasaki Heavy Industries (of which 1 shouldn't be ignored!) you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Kawasaki Heavy Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7012

Kawasaki Heavy Industries

Engages in aerospace systems, energy solution and marine engineering, precision machinery and robot, rolling stock, and motorcycle and engine businesses in Japan and internationally.

Solid track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor