Advertisement

Hitachi, Ltd. (TSE:6501) is about to trade ex-dividend in the next 3 days. The ex-dividend date generally occurs two days before the record date, which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. This means that investors who purchase Hitachi's shares on or after the 28th of March will not receive the dividend, which will be paid on the 4th of June.

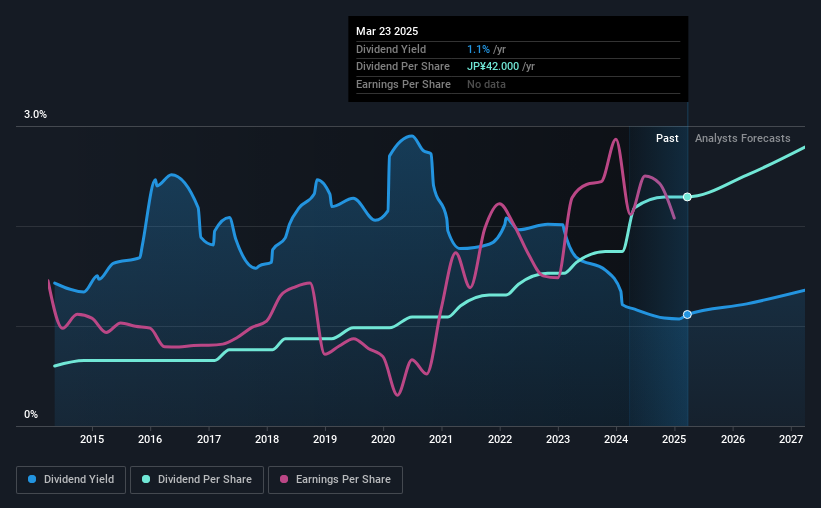

The company's next dividend payment will be JP¥15.00 per share, on the back of last year when the company paid a total of JP¥42.00 to shareholders. Calculating the last year's worth of payments shows that Hitachi has a trailing yield of 1.1% on the current share price of JP¥3767.00. If you buy this business for its dividend, you should have an idea of whether Hitachi's dividend is reliable and sustainable. We need to see whether the dividend is covered by earnings and if it's growing.

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Hitachi paid out a comfortable 33% of its profit last year. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Thankfully its dividend payments took up just 28% of the free cash flow it generated, which is a comfortable payout ratio.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

View our latest analysis for Hitachi

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings fall far enough, the company could be forced to cut its dividend. That's why it's comforting to see Hitachi's earnings have been skyrocketing, up 21% per annum for the past five years. Hitachi is paying out less than half its earnings and cash flow, while simultaneously growing earnings per share at a rapid clip. This is a very favourable combination that can often lead to the dividend multiplying over the long term, if earnings grow and the company pays out a higher percentage of its earnings.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Hitachi has delivered 14% dividend growth per year on average over the past 10 years. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

To Sum It Up

Is Hitachi worth buying for its dividend? Hitachi has been growing earnings at a rapid rate, and has a conservatively low payout ratio, implying that it is reinvesting heavily in its business; a sterling combination. Hitachi looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

While it's tempting to invest in Hitachi for the dividends alone, you should always be mindful of the risks involved. For example - Hitachi has 1 warning sign we think you should be aware of.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Hitachi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6501

Hitachi

Provides digital system and services, green energy and mobility, and connective industry solutions in Japan and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor