Okano Valve Mfg.Co.Ltd. (TSE:6492) Stock's 26% Dive Might Signal An Opportunity But It Requires Some Scrutiny

Okano Valve Mfg.Co.Ltd. (TSE:6492) shareholders that were waiting for something to happen have been dealt a blow with a 26% share price drop in the last month. Looking at the bigger picture, even after this poor month the stock is up 44% in the last year.

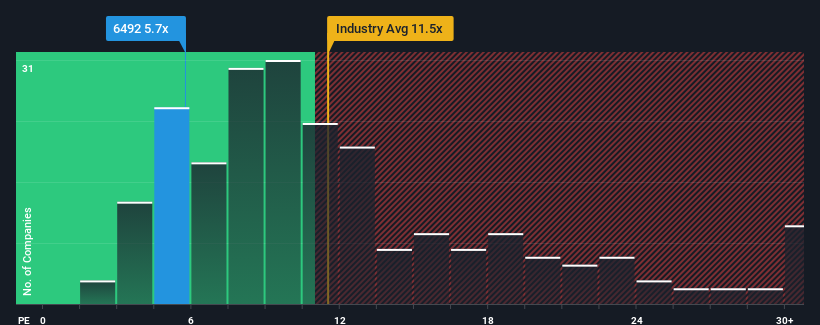

Although its price has dipped substantially, Okano Valve Mfg.Co.Ltd may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 5.7x, since almost half of all companies in Japan have P/E ratios greater than 14x and even P/E's higher than 21x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Recent times have been quite advantageous for Okano Valve Mfg.Co.Ltd as its earnings have been rising very briskly. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Okano Valve Mfg.Co.Ltd

Is There Any Growth For Okano Valve Mfg.Co.Ltd?

In order to justify its P/E ratio, Okano Valve Mfg.Co.Ltd would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered an exceptional 104% gain to the company's bottom line. The latest three year period has also seen an excellent 106% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 9.8% shows it's noticeably more attractive on an annualised basis.

With this information, we find it odd that Okano Valve Mfg.Co.Ltd is trading at a P/E lower than the market. It looks like most investors are not convinced the company can maintain its recent growth rates.

What We Can Learn From Okano Valve Mfg.Co.Ltd's P/E?

Shares in Okano Valve Mfg.Co.Ltd have plummeted and its P/E is now low enough to touch the ground. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Okano Valve Mfg.Co.Ltd currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Okano Valve Mfg.Co.Ltd (of which 1 doesn't sit too well with us!) you should know about.

You might be able to find a better investment than Okano Valve Mfg.Co.Ltd. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6492

Okano Valve Mfg.Co.Ltd

Manufactures and sells industrial valve for high pressure and high temperature services in Japan.

Flawless balance sheet and good value.

Market Insights

Community Narratives