Advertisement

Even With A 28% Surge, Cautious Investors Are Not Rewarding Juki Corporation's (TSE:6440) Performance Completely

Juki Corporation (TSE:6440) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 11% in the last twelve months.

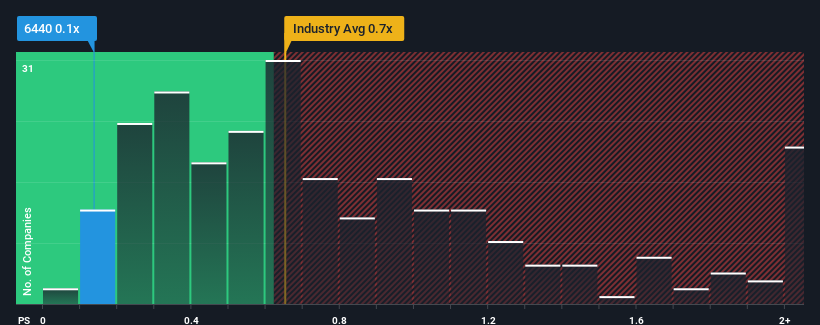

Although its price has surged higher, given about half the companies operating in Japan's Machinery industry have price-to-sales ratios (or "P/S") above 0.7x, you may still consider Juki as an attractive investment with its 0.1x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for Juki

How Juki Has Been Performing

While the industry has experienced revenue growth lately, Juki's revenue has gone into reverse gear, which is not great. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Juki will help you uncover what's on the horizon.Do Revenue Forecasts Match The Low P/S Ratio?

In order to justify its P/S ratio, Juki would need to produce sluggish growth that's trailing the industry.

Retrospectively, the last year delivered a frustrating 3.3% decrease to the company's top line. As a result, revenue from three years ago have also fallen 2.2% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 8.2% over the next year. With the industry only predicted to deliver 4.8%, the company is positioned for a stronger revenue result.

In light of this, it's peculiar that Juki's P/S sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Final Word

Despite Juki's share price climbing recently, its P/S still lags most other companies. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

To us, it seems Juki currently trades on a significantly depressed P/S given its forecasted revenue growth is higher than the rest of its industry. There could be some major risk factors that are placing downward pressure on the P/S ratio. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Juki (1 can't be ignored) you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6440

Juki

Manufactures and sells industrial and household sewing machines, and industrial equipment in Japan, China, rest of Asia, the Americas, Europe, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor