Advertisement

Investors Shouldn't Be Too Comfortable With Komori's (TSE:6349) Earnings

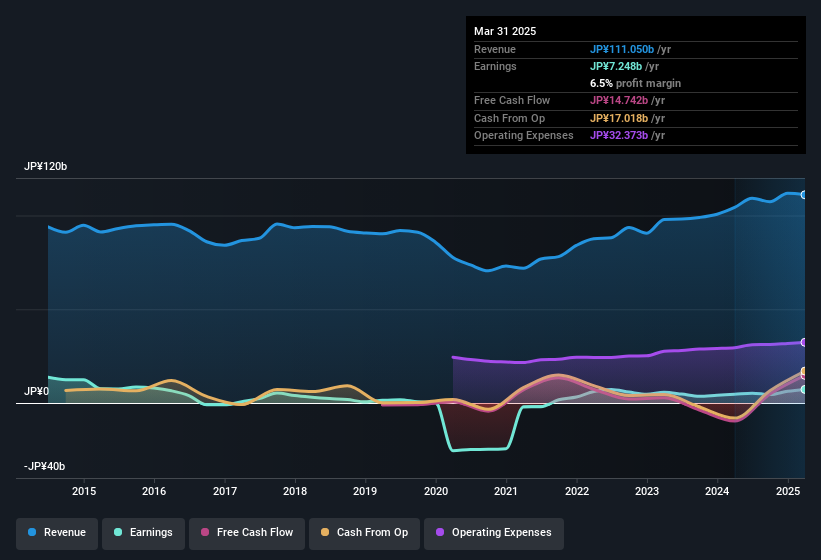

Komori Corporation's (TSE:6349) robust earnings report didn't manage to move the market for its stock. We did some digging, and we found some concerning factors in the details.

We've discovered 2 warning signs about Komori. View them for free.

A Closer Look At Komori's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

Over the twelve months to March 2025, Komori recorded an accrual ratio of -0.11. That indicates that its free cash flow was a fair bit more than its statutory profit. In fact, it had free cash flow of JP¥15b in the last year, which was a lot more than its statutory profit of JP¥7.25b. Given that Komori had negative free cash flow in the prior corresponding period, the trailing twelve month resul of JP¥15b would seem to be a step in the right direction. However, that's not all there is to consider. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part.

See our latest analysis for Komori

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Komori.

The Impact Of Unusual Items On Profit

Surprisingly, given Komori's accrual ratio implied strong cash conversion, its paper profit was actually boosted by JP¥1.5b in unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And, after all, that's exactly what the accounting terminology implies. If Komori doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Komori's Profit Performance

In conclusion, Komori's accrual ratio suggests its statutory earnings are of good quality, but on the other hand the profits were boosted by unusual items. Based on these factors, we think it's very unlikely that Komori's statutory profits make it seem much weaker than it is. If you'd like to know more about Komori as a business, it's important to be aware of any risks it's facing. Every company has risks, and we've spotted 2 warning signs for Komori you should know about.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

Discover if Komori might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6349

Komori

Engages in the manufacture, sale, and repair of printing presses in Japan, North America, Europe, and Greater China.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor