Advertisement

- France

- /

- Basic Materials

- /

- ENXTPA:VCT

3 Reliable Dividend Stocks With Up To 9.1% Yield

Simply Wall St

Reviewed by Simply Wall St

As global markets experience a boost from easing core inflation and robust bank earnings, major U.S. stock indexes have rebounded, with value stocks notably outperforming growth shares. In this context of optimistic economic signals and potential rate adjustments, dividend stocks stand out as attractive options for investors seeking steady income streams.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Peoples Bancorp (NasdaqGS:PEBO) | 5.11% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.32% | ★★★★★★ |

| Guaranty Trust Holding (NGSE:GTCO) | 6.38% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 3.48% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.68% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.49% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.13% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.47% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.93% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.89% | ★★★★★★ |

Click here to see the full list of 1981 stocks from our Top Dividend Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

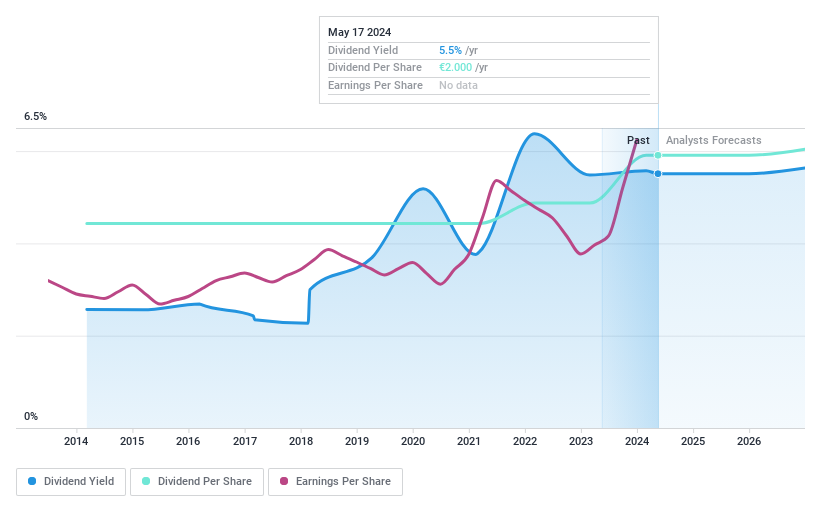

Vicat (ENXTPA:VCT)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Vicat S.A. operates in the construction industry through the production and sale of cement, ready-mixed concrete, and aggregates, with a market cap of approximately €1.68 billion.

Operations: Vicat S.A. generates revenue from its main segments, with €2.52 billion from Cement and €1.55 billion from Concrete & Aggregates.

Dividend Yield: 5.3%

Vicat offers a stable and reliable dividend, with a 5.3% yield, though slightly below the top quartile in France. Its dividends are well-covered by earnings and cash flows, with payout ratios of 33.4% and 45.7%, respectively. Over the past decade, Vicat's dividends have been consistent and growing despite its high debt level. The stock trades at a significant discount to its estimated fair value, suggesting good relative value compared to peers and industry standards.

- Navigate through the intricacies of Vicat with our comprehensive dividend report here.

- Our expertly prepared valuation report Vicat implies its share price may be lower than expected.

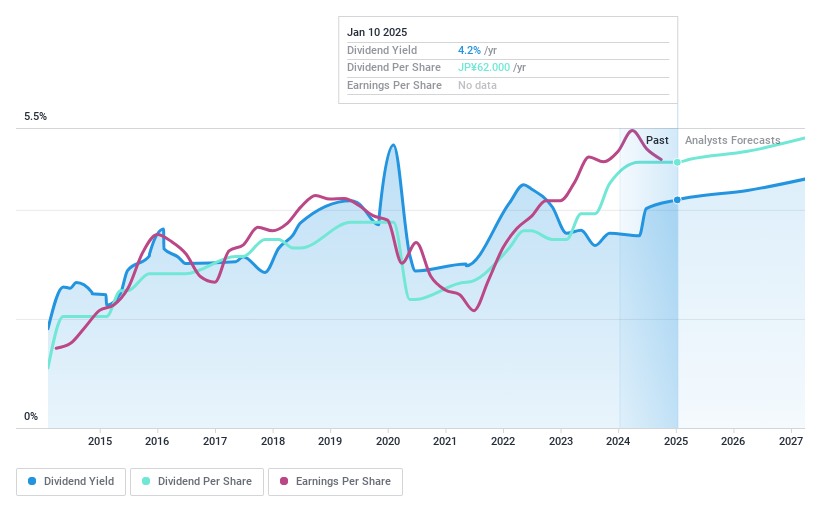

Amada (TSE:6113)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Amada Co., Ltd. is a global company that manufactures, sells, leases, and services metalworking machinery and related software and equipment, with a market cap of ¥538.64 billion.

Operations: Amada Co., Ltd.'s revenue segments include the manufacture, sale, leasing, repair, maintenance, checking, and inspection of metalworking machinery, software, and peripheral equipment across various regions including Japan, North America, Europe, and Asia.

Dividend Yield: 4%

Amada's dividend yield of 3.95% ranks in the top 25% of Japan's market, yet its dividend history has been volatile and unreliable over the past decade. Recent improvements include a dividend increase to ¥31 per share from ¥25 year-over-year. Dividends are covered by earnings and cash flows, with payout ratios of 84.7% and 55.5%, respectively, indicating sustainability despite past instability. The company also completed a significant share buyback program worth ¥15.96 billion, enhancing shareholder value.

- Click here and access our complete dividend analysis report to understand the dynamics of Amada.

- Upon reviewing our latest valuation report, Amada's share price might be too pessimistic.

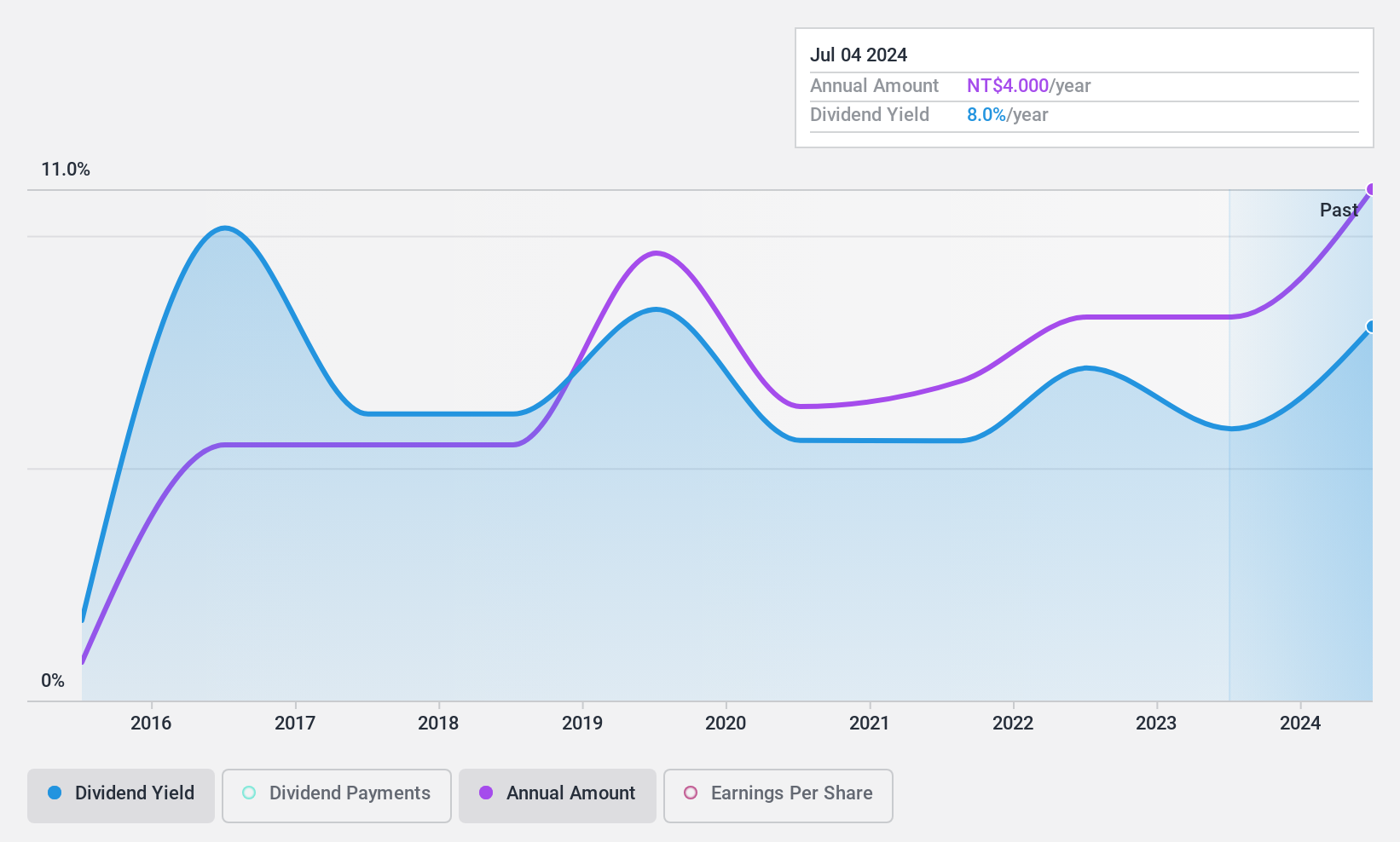

Darfon Electronics (TWSE:8163)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Darfon Electronics Corp. offers eco-friendly technologies in IT peripherals, passive components, and green energy solutions with a market cap of NT$12.22 billion.

Operations: Darfon Electronics Corp.'s revenue is primarily derived from Intelligent Products, contributing NT$12.40 billion, and Green Energy Products, generating NT$9.87 billion.

Dividend Yield: 9.1%

Darfon Electronics offers a high dividend yield of 9.1%, placing it among the top 25% in Taiwan's market. However, its dividends have been volatile and unreliable over the past decade, with a high payout ratio of 156.6%, indicating they are not well covered by earnings despite being supported by cash flows. Recent financial results show declining sales and net income, with Q3 net income at TWD 189.41 million compared to TWD 1,074.43 million last year, raising concerns about future dividend sustainability amidst falling profits and margins.

- Delve into the full analysis dividend report here for a deeper understanding of Darfon Electronics.

- Our valuation report here indicates Darfon Electronics may be undervalued.

Taking Advantage

- Reveal the 1981 hidden gems among our Top Dividend Stocks screener with a single click here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:VCT

Vicat

Engages in the production and sale of cement, ready-mixed concrete, and aggregates for construction industry.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.2% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|27.0% undervalued

KA

Community Contributor