Okuma (TSE:6103) shares edged up 0.04% today, continuing a slight upward move over the past week. Investors are watching closely to see if recent momentum can meaningfully impact the company’s performance over the coming months.

Despite mild share price gains today, Okuma’s momentum has been mixed within the broader year. While the stock has posted a steady 1-year total shareholder return of 0.11%, recent months have seen performance plateau. This suggests investors are still weighing its long-term prospects.

Given its modest returns and positive but decelerating growth, the key question is whether Okuma’s current valuation leaves room for upside or if the market is already factoring in the company’s future potential.

Advertisement

Price-to-Earnings of 24.6x: Is it justified?

Okuma’s current price-to-earnings ratio (24.6x, last close ¥3,480) signals a premium compared to peers, with valuation running ahead of industry standards and fair value benchmarks.

The price-to-earnings (P/E) ratio measures how much investors are willing to pay for each yen of Okuma’s earnings. In capital goods manufacturing, this is often used as a proxy for market confidence in a company’s growth, profitability, and risk outlook.

At 24.6x earnings, Okuma is priced significantly higher than both the Japanese Machinery industry average (13.3x) and its peer group average (14.7x). The estimated fair P/E ratio, calculated at 20.5x, also sits well below Okuma’s current level. This suggests the market is pricing in higher earnings growth or quality than is typical for its sector.

However, risks remain, such as profit volatility and a premium valuation, which could be pressured if Okuma’s earnings growth fails to meet market expectations.

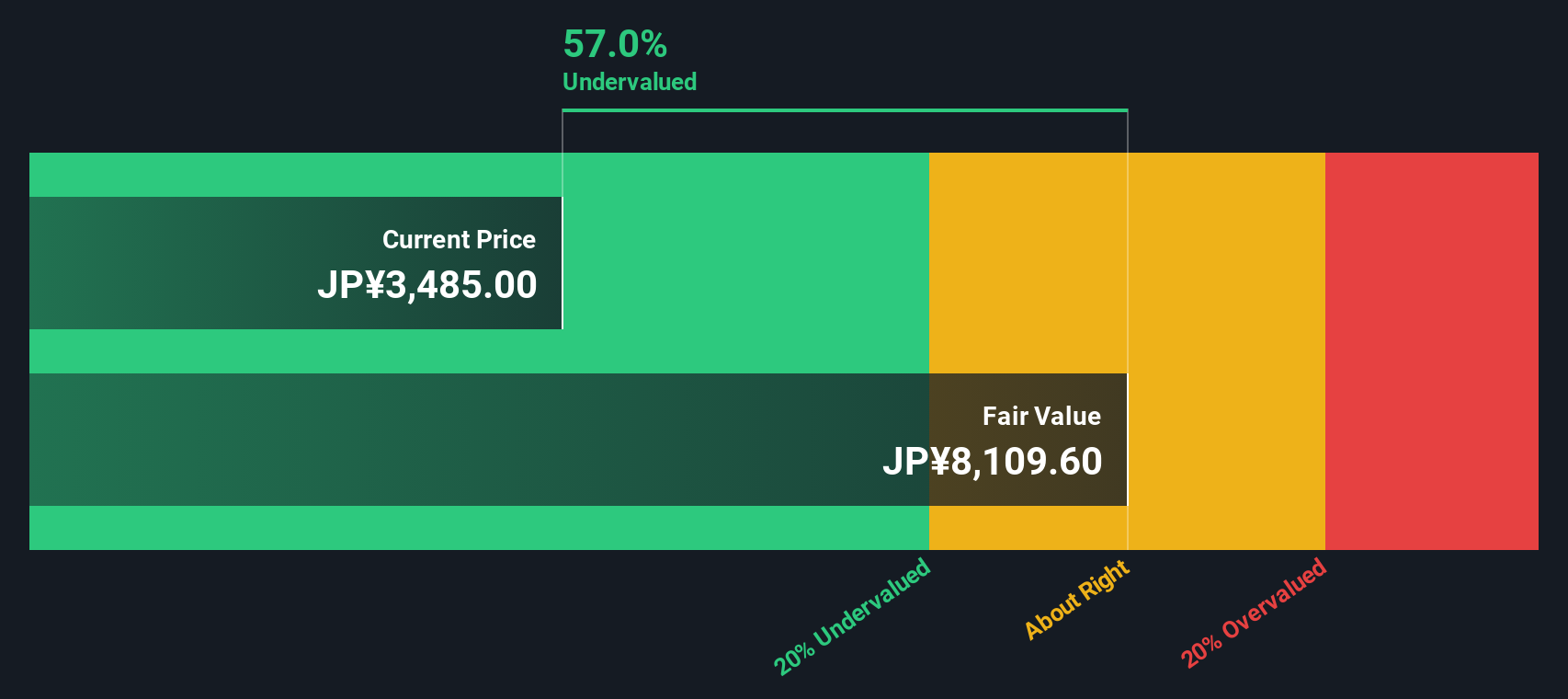

Another View: Discounted Cash Flow Signals Undervaluation

While the high price-to-earnings ratio presents Okuma as expensive, our DCF model offers a different perspective. Based on projected cash flows, Okuma trades more than 57% below our calculated fair value. Could the market be too cautious, or is optimism misplaced? The answer depends on which evaluation method investors trust more.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Okuma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Okuma Narrative

Keep in mind that if you see the story differently or want to dig into the numbers yourself, you can shape your own analysis in just a few minutes with Do it your way.

If you want to get ahead of the pack, now is the time to scout other stocks and investment themes with the Simply Wall Street Screener. Don’t miss out on fresh opportunities that savvy investors are already tracking.

Unlock rapid growth potential by following these 24 AI penny stocks, which are innovating in artificial intelligence and transforming entire industries.

Tap into robust passive income streams by checking out these 19 dividend stocks with yields > 3%, which offer attractive yields to strengthen your portfolio’s income profile.

Catch the next big trend in financial technology by exploring these 78 cryptocurrency and blockchain stocks, which are pioneering new ways to profit from blockchain and digital assets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies